Well then it has huge competition from Adani Lounges.

Posts in category Value Pickr

Dreamfolks services limited( DFS) (15-02-2024)

I believe that this company has the potential to establish exclusive lounges in premium locations, which would set them apart from simply being an aggregator. This strategic move could solidify their position in the market, making it difficult for new entrants to replace them.

IREDA: Renewable Energy Powerhouse (15-02-2024)

Yes I know that ![]() . My point is that ignore the funds which are buying due to it being part of an Index, or part of the PSU sector (PSU theme funds). People are doing SIP/lumpsum in those funds in heavy number, and the fund manager has no other option but to buy. They have already crossed allocation in TREPS, free cash etc and they will need to continue buying the company.

. My point is that ignore the funds which are buying due to it being part of an Index, or part of the PSU sector (PSU theme funds). People are doing SIP/lumpsum in those funds in heavy number, and the fund manager has no other option but to buy. They have already crossed allocation in TREPS, free cash etc and they will need to continue buying the company.

Look at HNI’s, Ace investors, FII in smallcaps.

MTAR Technologies – A wager on innovation meeting economies of scale (15-02-2024)

Need some overall market correction, and stock to consolidate along 1200-1500 before building any new position.

I am not invested as long as promoter is on a selling spree.

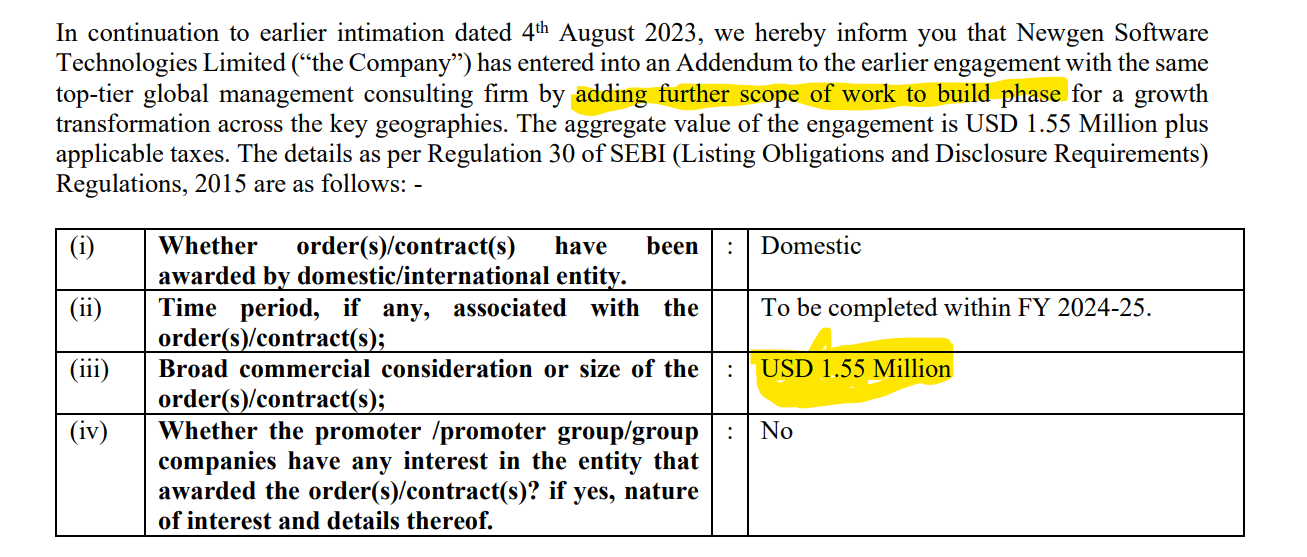

Newgen Software (15-02-2024)

Mining existing client.

D: Invested

Newgen Software (15-02-2024)

Mining existing client.

D: Invested

Infollion Research Services Ltd – Moated Microcap with Differentiated business? (15-02-2024)

Challenges to name a few:

-

Company intends to grow in US market (which is the main reason for going to SME IPO), However not easy to crack US market

- Timezone difference makes it challenging for active engagement

- Any possible extenstion of it like in-person engagement would be extremely impossible (assuming the cost involved, turn around time for F2F etc), So it must be restricted to engagements which they are sure of 100% remote consultation with experts.

- Very mature market with very well established players and space is very crowded. Difficult to standout in the crowd.

-

Extremely tied with economic activity (meaning cyclical), now the going is good – so enjoying. But during economic stagnation and/or recession, this business has to sit out for better days.

-

No exclusivity either with experts or the client. Hence there is really no moat – except the data (skill set of expert and requirement for client) acquisition and mapping between expert and clients.

-

Not sure, how they would be able to manage the inflation – i.e cost to experts and internal escalation of the cost – as it is very competitive market with no moat. So we should expect all the returns to normalize to around 15~20% in longer run – from current 40% (ROE and ROCE)

-

Though the company has tried to expand to multiple pillars of growth for now – only Expert Calls seems to be contributing majorly for both the topline and bottomline.

-

Any long duration engagement may mean that client can circumvent the company and have direct relation with the expert. Hence this would mean company focusing on short term duration project – which may also mean – not longer term visibility into revenue stream.

-

Top few clients gobble up major portion of revenue stream for the company – which may indicate inability of a deeper and wider penetration by the company.

Infollion Research Services Ltd – Moated Microcap with Differentiated business? (15-02-2024)

Challenges to name a few:

-

Company intends to grow in US market (which is the main reason for going to SME IPO), However not easy to crack US market

- Timezone difference makes it challenging for active engagement

- Any possible extenstion of it like in-person engagement would be extremely impossible (assuming the cost involved, turn around time for F2F etc), So it must be restricted to engagements which they are sure of 100% remote consultation with experts.

- Very mature market with very well established players and space is very crowded. Difficult to standout in the crowd.

-

Extremely tied with economic activity (meaning cyclical), now the going is good – so enjoying. But during economic stagnation and/or recession, this business has to sit out for better days.

-

No exclusivity either with experts or the client. Hence there is really no moat – except the data (skill set of expert and requirement for client) acquisition and mapping between expert and clients.

-

Not sure, how they would be able to manage the inflation – i.e cost to experts and internal escalation of the cost – as it is very competitive market with no moat. So we should expect all the returns to normalize to around 15~20% in longer run – from current 40% (ROE and ROCE)

-

Though the company has tried to expand to multiple pillars of growth for now – only Expert Calls seems to be contributing majorly for both the topline and bottomline.

-

Any long duration engagement may mean that client can circumvent the company and have direct relation with the expert. Hence this would mean company focusing on short term duration project – which may also mean – not longer term visibility into revenue stream.

-

Top few clients gobble up major portion of revenue stream for the company – which may indicate inability of a deeper and wider penetration by the company.

Hitesh portfolio (15-02-2024)

Biggest issue with Lux still continues to be corporate governance. Any company where you find instances of insider trading, IT raids, family feuds is always a risky proposition regardless of whether those issues are behind them or valuations are low.

Hitesh portfolio (15-02-2024)

Biggest issue with Lux still continues to be corporate governance. Any company where you find instances of insider trading, IT raids, family feuds is always a risky proposition regardless of whether those issues are behind them or valuations are low.