Got it @hitesh2710 bhai, thank you for the guidance!

Posts in category Value Pickr

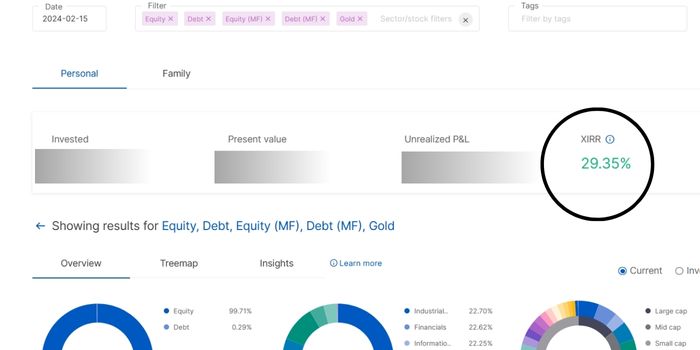

How much is your XIRR? (15-02-2024)

It may be due to high churning. It will show if most holdings will be more than one year.

How much is your XIRR? (15-02-2024)

Zerodha doesn’t calculate it for me because of churn.

Brokerages should really get IRR and TWRR in.

How much is your XIRR? (15-02-2024)

Doesn’t show anything for my 2 accounts. Also checked with a friend.

How much is your XIRR? (15-02-2024)

Hello friends,

I have recently checked at Zerodha and my portfolio XIRR is showing around 29. How reliable is it and what’s yours (if you guys want to share)?

Time technoplast (15-02-2024)

Does anyone know company’s order-dispatch cycle?

In Q3 FY24 presentation, it has been mentioned company has an order book of ~400 Crs which at current run rate is less than one month of orders.

How does one evaluate if pending order book is good enough?

Simple Investing (15-02-2024)

@Likhitp – I consider HUL as a very good, competent company ideal for holding & long-term investing. Reason for not adding so far (I did have a small position sometime back which I had exited) is probably because with limited capital & already high allocation to FMCG, I wanted to focus & chose companies which I felt had a gap to fill (after of course the company passing the corporate governance & management ethics part). I see HUL as already a highly efficient company present in most of the areas they can target. Also, its the largest FMCG company so among large caps and already efficient companies, I think I chose a Nestle over HUL considering better gaps for Nestle to fill at product level in India. I may agree with you that consolidation times are probably the best times to accumulate highly efficient and fully valued companies and so are the times of dips & market crashes…

Disc: Not a buy/sell recommendation. Views for academic purposes and I can be wrong in all my assessments. Not eligible for any advice

Hitesh portfolio (15-02-2024)

I dont track the fundamentals of either Pennar Inds or Capacite infra. Charts of both companies look interesting. They are not in my watchlist.

RIIL has given a multi year breakout above 1100-1200. Stock price is at almost a 15 year high. But I have never managed to understand on what basis the stock keeps going up and down. Fundamentals wise a quick glance at the 10 year results on screener does not provide a very encouraging picture.

In the final phases of a bull markets stocks often go up, and go up a lot purely based on stories and narratives.

Our job as investors is to make sure we know what we are buying and why we are buying. This view has got nothing to do with RIIL in particular. Who knows it might go up a lot from here. But if I dont have any fundamental conviction, then it would be difficult for me to hold on to it if it starts correcting.

The biggest mistakes are committed in roaring bull markets and they often turn out to be the most expensive. Hence while investing particularly during frothy bull markets we have to be very sure about what we are buying.

Yatharth Hospital & Trauma Care Services Limited (15-02-2024)

Con Call Highlights

-

Q3 occupancy lower due to many festivals etc in between which delays a lot of elective surgeries. Jan utilisation levels are higher and Q4 is likely to be materially higher than Q3

-

EBITDA breakeven for Asian Fidelis in 2 years. Likely ARPOB around Noida Hospital (currently at 25-30k range).

-

Jhansi Orcha is currently running at 6% EBITDA levels, to reach optimum utlisation capacity by next year (indicating big bump in next few quarters… since Q3 utilisation is around 22%)

-

Receivables has inched up mainly due to government side… but they are likely to be in control and release in the coming months

-

Robotic surgeries started in Greater Noida & Noida Extension and ARPOB is likely to inch up further in Q4. Radition oncology will also help that.

-

No EWS obligation on the hospital. Lands bought at market rates.

-

International patient ARPOB is higher. To get a boost once Noida airport starts (slated for end 2024 with 1 runway)

-

Tax was kept higher due to some conservative calculations, would normalise in subsequent few quarters

-

Brownfield expansions (Greater Noida & Noida Extension) to come up in next 1-2 years since the hospitals would reach the utilisation by then.

-

Confident of maintaining EBITDA % as in FY24 in the next year despite losses from Asian Fidelis (higher ARPOB is coming!)

Hoping for a bumper Q4 given higher ARPOBs and utilisation.

D – Invested