Street expectation is always been over their guidence… Compony has been under promising and over achieving. But this time commentry hinting towards real slowness. Whats yous opinion

Posts in category Value Pickr

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (25-10-2024)

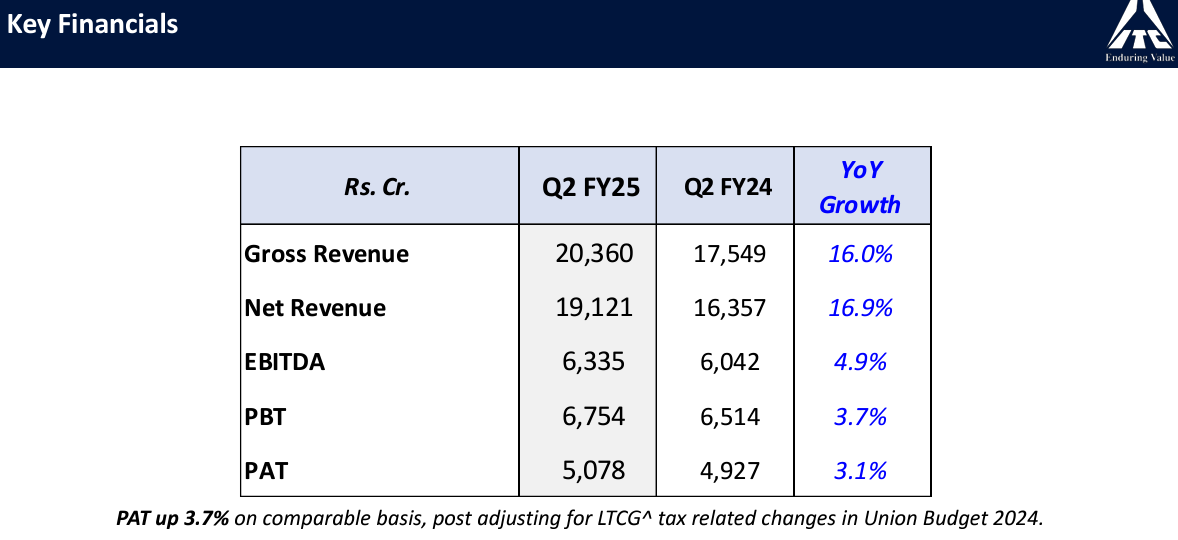

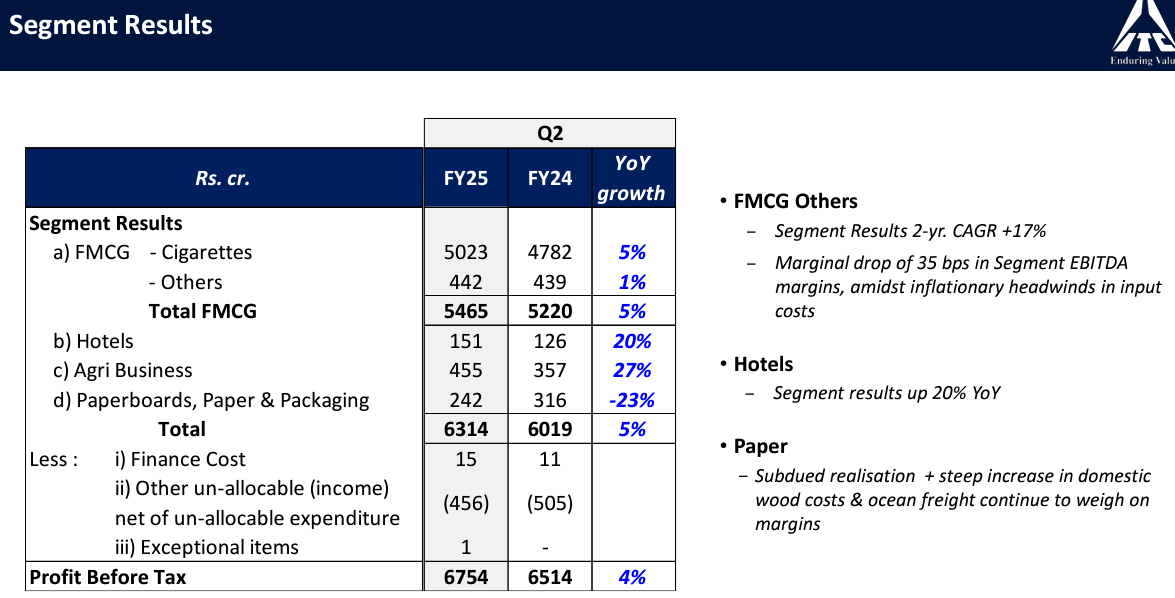

ITC Q2 FY25 Results: Top-line, Bottom-line, and Key Insights

Few insights from ITC’s Q2 results and investor presentation:

-

ITC delivered robust top-line growth in Q2 FY25, with Segment Revenue reaching ₹23,025 crores, a 9.3% YoY increase. This growth was propelled by notable contributions from various segments:

- FMCG: Both cigarettes and other FMCG products witnessed healthy growth, recording 6.1% and 6.3% YoY increases respectively.

- Hotels: The segment demonstrated a strong rebound with a 10.9% YoY growth in revenue.

- Agri Business: A significant 22.2% YoY surge in revenue was observed in this segment.

-

Despite this overall growth, the Paperboards, Paper & Packaging segment experienced a decline, with revenue decreasing by 6.8% YoY. The presentation attributes this performance to the impact of low-priced Chinese supplies, subdued domestic demand, and subdued realizations.

-

ITC effectively managed inflationary pressures on input costs, resulting in resilient EBITDA margins for Q2 FY25. Key strategies employed included premiumization, supply chain optimization, calibrated pricing actions, digital initiatives, and strategic cost management.

-

The Hotels segment, in particular, showcased strong profitability, achieving a 20.2% YoY growth in segment results, reaching ₹151 crores. This impressive performance was fueled by a two-year CAGR of 34.2%.

-

Demerger update: Scheme sanctioned by NCLT on 4th October 2024 (certified copy of the Order awaited)

-

Overall, the Q2 FY25 results demonstrate ITC’s ability to navigate a challenging market environment while capitalizing on growth opportunities in its diversified portfolio.

Disclaimer: Invested and Biased. Less than 5% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions

Does GMR Infrastructure have a Potential to be a multi-bagger (25-10-2024)

This could be really helpful, please share your thoughts

Glenmark Life Sciences (25-10-2024)

I attended the concall. While the company is guiding for a strong H2, the overall guidance has been revised down to high single digit growth from the earlier mid teen guidance. This implies around 20% growth for H2 to meet the high single digit growth. Few things i am unable to understand are.

1 – Company maintained the earlier guidance during Q1 call even after knowing the impact of Ankleshwar closure.

2 – Ankleshwar closure was played down as a minor issue during Q1 call even after repeated queries on its impact. Now they are saying that it impacted in order fulfillment in both API and CDMO.

3 – Revision of guidance downwards is also attributed partially to softness in LATAM markets specially in Argentina.

While business is always dynamic, my worry is company is not able to foresee events unfolding even beyond a quarter or they are not sharing it with the investors. Last FY as well they guided for mid teen growth, maintained it after first 2 Qs but eventually ended up in mid single digits.

Disc – Invested from lower levels.

Avantel (25-10-2024)

amount they intend to riase is peanuts, they could have raised it as debt from banks easily, my sense is there is something else happening in the background, time will tell.

Red Tape Ltd. – The next fashion giant? (25-10-2024)

Every other brand is using a Discounted strategy nowadays. It’s a FOMO for marketing. As far as the brand image is concerned they fit into middle low and super brands. That’s a good strategy for long term though

V2 Retail – Second innings playing out well (25-10-2024)

Good results. It seems like H2 is going strong.

Indiamart Intermesh – Indian Alibaba? (25-10-2024)

Can someone explain how exactly do we determine the ROI Indiamart is getting through its investments in various companies as except Busy all are loss making? So if i had to see the ROI on their investments basically how do we do think of this?

@Yogesh_Bhandari @Chandragupta @smanek or anyone else?

Indiamart Intermesh – Indian Alibaba? (25-10-2024)

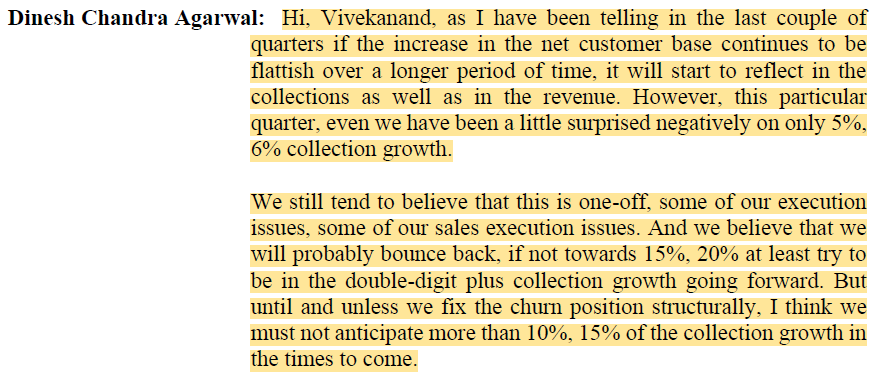

Basically management guidance was to maintain collections growth ~20-30% which started dipping below 20% since Q3’FY24 and they said they were still confident but it just kept getting lower every quarter. The reason for drop was lower net addittion of subscriber due to higher churn rates which the management themselves did not know how to solve. And Q2’FY25 results seem good but collection growth was 6%.

Unless collections growth/net adittion of subscribers don’t improve there is no way stock will go upward. Net adittion of subscribers since last 4 quarters have just been 2K QoQ, it needs to be atleast 5-8K QoQ for performance to improve.

The margins itself were higher just because less customer added so lesser customer acquistion costs, so margins will go down (even mgmt said so) once net adittion improves.

P.S: If you’re wondering why collection growth is important, it is basically a leading indicator for future revenues.

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (25-10-2024)

None that I know but that’s something you will have to decide for yourself if management can fulfill or if they will slash guidance as the situation develops.