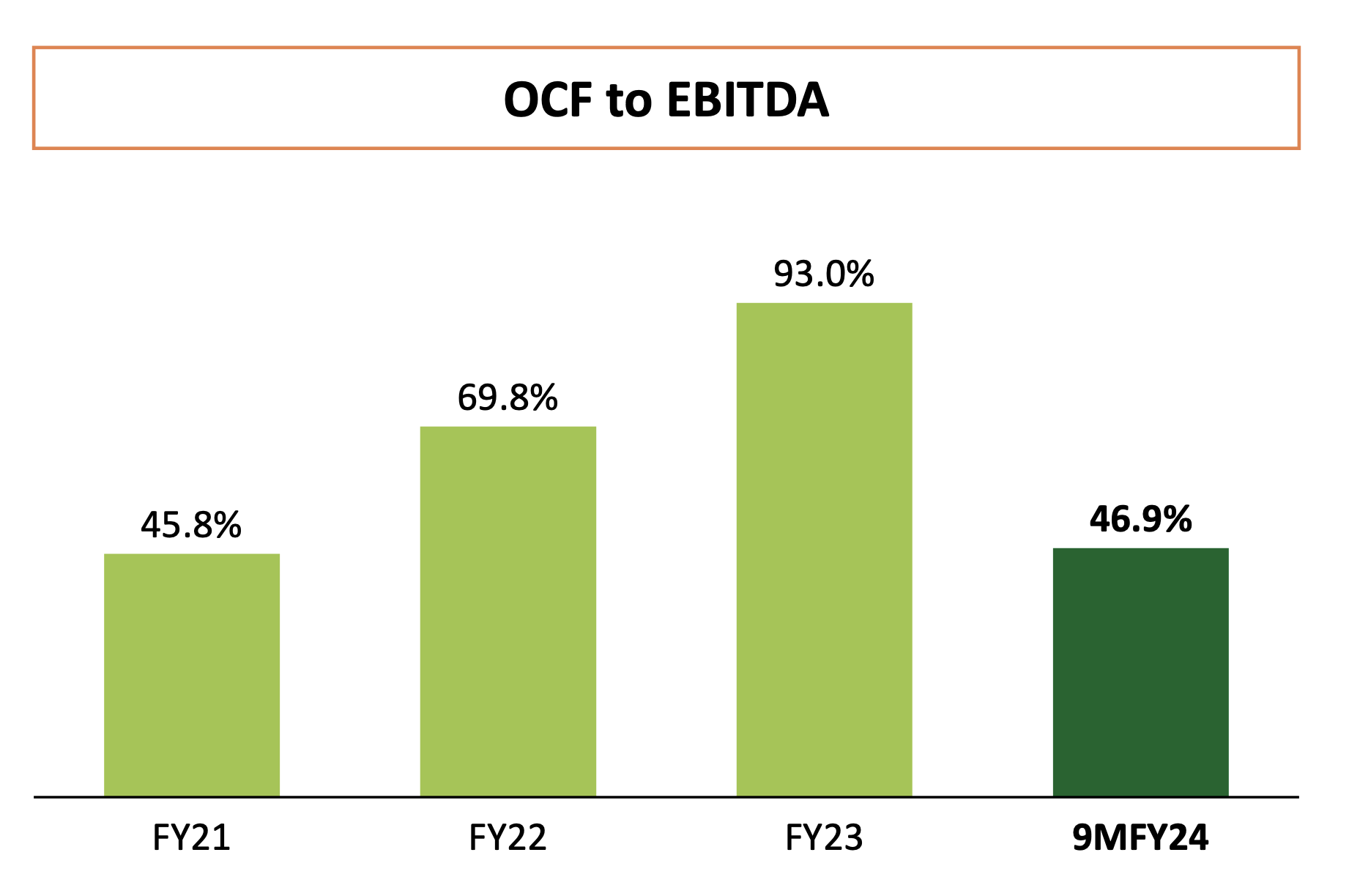

Hi. In the Investor Presentation of Shaily Engineering Plastics (slide 15), I saw the following ratio. Can someone explain as a concept what is this ratio supposed to indicate? Especially for a manufacturing company which has been spending a lot of money to put up new capex.