Why is Anandrathi enjoying premium valuation to Nuvama?? is it just because they do not have debts unlike Nuvama which has capital market business also???

Posts in category Value Pickr

Carysil (earlier Acrysil) – Kitchen sinks (13-02-2024)

The management has not clarified on the sharing of the cost for acquisitions done recently along with the plan to synergies the backend operations with these acquisition.

The manpower cost has gone up significantly in absolute as well percentage to sales ?

TCI Express – Logistics Sector niche player (13-02-2024)

Comparison given by @Pchandrapal is the right comparison (apple to apple) among the logistic players.

MTAR Technologies – A wager on innovation meeting economies of scale (13-02-2024)

To summarize a very long first message on this thread, I invested in MTAR for the following reasons:

• Management had a recent track record of exceeding guidance numbers

• Robust revenue growth from FY20 to FY23 (~₹214 – 574 cr), with EBITDA margins in the mid to high 20s

• Precision engineering company – lots of expertise and IP

• Active in critical growth sectors – clean energy, space, defence, nuclear energy

• The most upside (in my opinion) was in clean energy (fuel cells, H2 boxes, and electrolyzers), not to mention the highest potential for economies of scale to kick in (batch manufacturing to mass manufacturing of electrolyzers, etc.)

To say that Q3 results came as a shocker today would be an understatement.

Commenting on the results, Mr. Parvat Srinivas Reddy, Managing Director & Promoter, MTAR Technologies, said, “Revenues in FY24 shall be marginally higher as compared to FY23 due to deferment of export shipments in Clean Energy sector to the next fiscal year. However, the growth outlook for FY25 remains intact with 45% – 50% YoY likely increase in revenues. The company is in final stages of discussion with reputed global MNCs as well as made good progress in Small Satellite Launch Vehicle project.”

Rewinding the clock and going back to Q2 results, while this has been covered in detail in previous messages, I just wish to reiterate a few points from that con call:

• While order deferment from Bloom Energy was cited as the reason, I was not a fan of the drastic cut in revenue guidance for FY24 down to ₹670 – 700 cr from ₹830 – 860 cr. In addition the EBITDA margin guidance was reduced to 26% (+/- 100bps)

• Still expecting to see a closing order book of ₹1400 to 1500 cr

• Delivered approximately 400 and 200 units of Yuma and Santa Cruz Block 1, respectively

• Expecting to deliver 528 units of Santa Cruz Block 2 in Q3

• Expecting to deliver 44 electrolyzers in Q3 and 66 in Q4

• In talks with Fluence Energy around energy storage systems, which could be a ₹120 – 130 cr business in FY25, with plans to deliver 1000 units. Fluence wants MTAR to build the capacity to deliver 3000 plus units

• Over the long term, proactively planning to get EBITDA margins to 28%

• Expecting H2 domestic sales to be 3x what they were in H1, indicating a jump from ₹50 cr to ₹150 cr

So when I look at the Q3 numbers, I have a lot of questions, which I hope will be answered in tomorrow’s con call:

• With the total revenue from Q1 to Q3 adding up to around ₹445 cr, what actual number are we targeting for FY24 revenue? If it is significantly lower than the lower end of the Q2 revised guidance of ₹670 cr, I will have trouble taking guidance figures at face value going forward

• Is there a revenue recognition issue that caused this massive drop in Q3 revenue? For example, products that should have been shipped on Dec 29 did not leave the factory till January 3, and therefore revenue will have to be recognized in Q4?

• How many Santa Cruz boxes were shipped in Q3? The target was around 530 from the previous call

• How are the conversations with Fluence Energy progressing? Is the ₹120 – 130 cr revenue projection for FY25 (~1000 units) still accurate?

• How many electrolyzers were actually shipped in Q3? What are we expecting for Q4, and when are we going to make the transition from batch manufacturing to high volume mass manufacturing here? Over the next 3-5 years, can the revenue contribution from electrolyzers increase massively, and even exceed the contribution from fuel cells/hot boxes/hydrogen boxes?

• Are second half domestic sales going to be anywhere close to the projected ₹150 cr?

• What does management project for the FY24 closing order book number?

Just so I don’t misquote something, I will wait for the transcript of tomorrow’s call before drafting my next message.

Disclosure of holding: I started buying MTAR Technologies in August 2022, at a price of ₹1422. My cost basis has moved up to ₹1555. I have a fairly concentrated portfolio, and do not hold more than 10 companies at any given time.

Orchid Pharma Ltd (13-02-2024)

Anyone who is tracking this stock for long does know why it rose almost 12000% in 2020-2021 rally? Back then it looked like a operators stock!!

Experiment with Low Volatility (13-02-2024)

I stopped that portfolio and is now fully invested in momentum

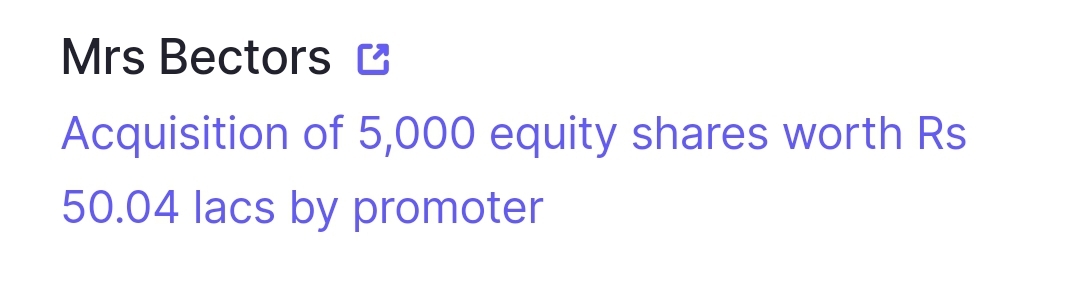

Mrs Bectors Food Specialities: Can it beat the industry? (13-02-2024)

Promotor knows his company better

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (13-02-2024)

BCL Ind Quarterly Investor call notes:

- Recent increase in price by Govt for Ethanol produced from maize to add to the margins from this (Q4) quarter

- Svaksha Distillery capacity expansion to 300 KLPD likely to be over this quarter

- Expect the approvals for 150 KLPD expansion in Bhatinda distillery to come in next few months. It will take around 12 months for the plant to be ready from the approval date. This will take total Distillery capacity (Bhatinda + Svaksha) to 850 KLPD

- Applied for permission to set-up 100 KLPD Biodiesel plant in Bhatinda. Expect the approvals to come in around 3 months time (approx). It will take around 12 months for the plant to be ready from the approval date.

- Around 40% of the raw-material required to produce Biodiesel is already available in-house.

- Biodiesel price is around Rs 82/litre. It is more margin accretive than Ethanol, specially because of the inhouse availability of around 40% of raw material.

- They will be shutting down the Edible oil factory which is within Bhatinda city limits by year (calendar) end. Management waiting to see Govt policy on Edible oil before they decide what part of Edible oil business to retain. They will move the related machinery to the existing distillery plant. This will save overhead costs as existing utilities will be shared.

- Strong demand for their Country Liquor. Awaiting Punjab govt excise policy to decide on <forgot, will update once they publish the transcript>

- Company has competitive advantage over other Ethanol producers because it is already maize ready while many others are struggling since govt stopped selling FCI rice for ethanol.

- Even after considering the planned capacity expansion by other players, Management thinks that it will be a tall task to produce enough Ethanol to meet Govts 20% blending target within the deadline. Hence they see no danger with regards to lack of demand for Ethanol. This is specially considering that Govt is encouraging Ethanol produced by maize over Rice and Sugarcane.

Todays call was short one as the Management had to cut short the call due to disturbances at their end.

I like that

- BCL is diversifying in a related area (biodiesel) which is futuristic (green economy) where their decades of experience in raw material sourcing and contacts will come in handy as much of the raw material is common between biodiesel and their existing products. Also their products Ethanol and Biodiesel have the tailwinds interms of regulatory support, which will be in-place for years to come because of Indias pledge at COP26 to reduce carbon emission

- BCL has the next generation of Management in place. Mr. Kushal Mittal seems well spoken and he knows the business well. Also, he refrains from tall claims and clearly articulates the uncertainities in the business on investor calls.

- Over the years their Investor communications have become very professional. Look at the latest quarterly presentation, it will help you understand their business and future plans very well.

Disc: Invested.

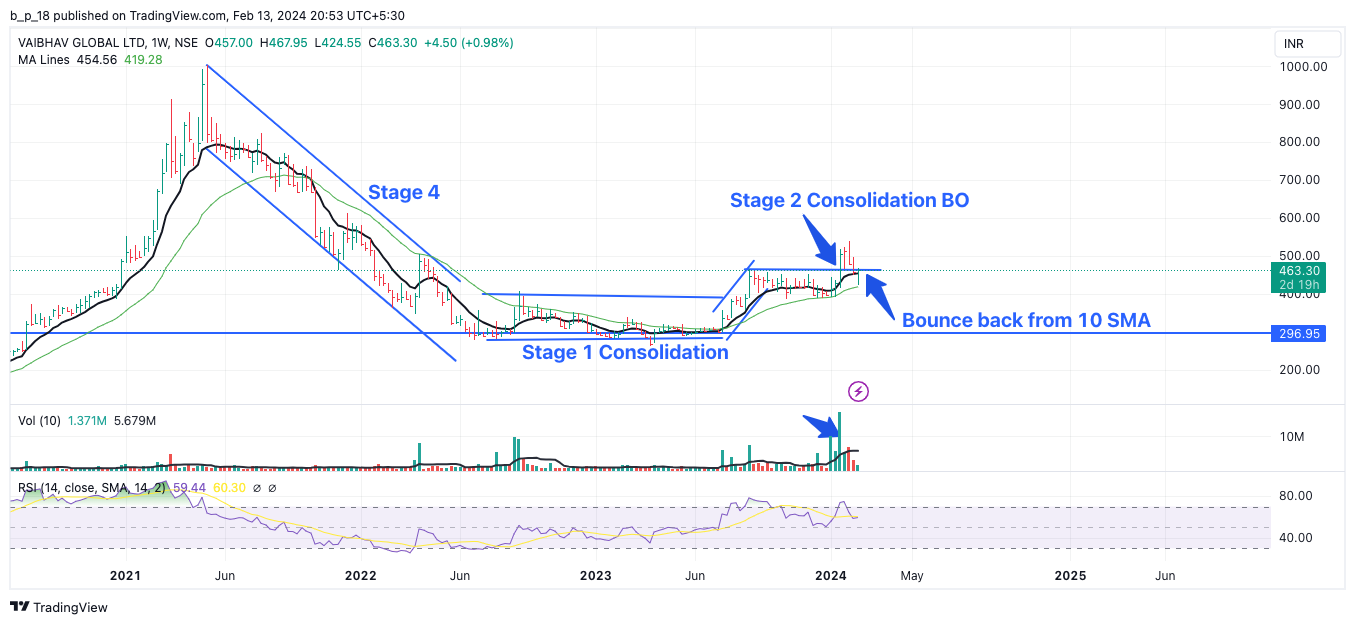

Bull therapy 101-thread for technical analysis with the fundamentals (13-02-2024)

Adding my chart analysis for Vaibhav Global. Smaller red candles on pull back from stage 2 BO would have been more encouraging. But the setup along with good results look good for a stage 2 rally.

Experts please feel free to correct.

Discl. – Not invested. For study purposes

Mrs Bectors Food Specialities: Can it beat the industry? (13-02-2024)

Promoter buying at technical support is always a good sign