Q3FY24 results – https://www.bseindia.com/xml-data/corpfiling/AttachLive/4a93bd5d-47c7-46ad-8f3f-cc4704d5b74b.pdf

Sales have grown 65% YoY and OPM have expanded to 14%

chart also looks great with consolidation ongoing for the last 6 months.

Q3FY24 results – https://www.bseindia.com/xml-data/corpfiling/AttachLive/4a93bd5d-47c7-46ad-8f3f-cc4704d5b74b.pdf

Sales have grown 65% YoY and OPM have expanded to 14%

chart also looks great with consolidation ongoing for the last 6 months.

It’s just profit booking. Since stock has 5% circuit limit (under ASM), it has been in Red for last few sessions. I believe it’s corrected 25% from the top, in the last 3-4 sessions, which is pretty much the same for all small caps stock that ran too much ahead of their valuations in last 1 year.

I believe it’s more of an industry issue. All the logisitcs companies (VRL, Navkar, Allcargo, Mahindra Logistics etc) have come up with bad numbers, much worse than TCI express. But I can’t figure out what and where the issue is in indian logistics industry. I thought with uptick in economic activity, logistics sector should have a natural tailwind.

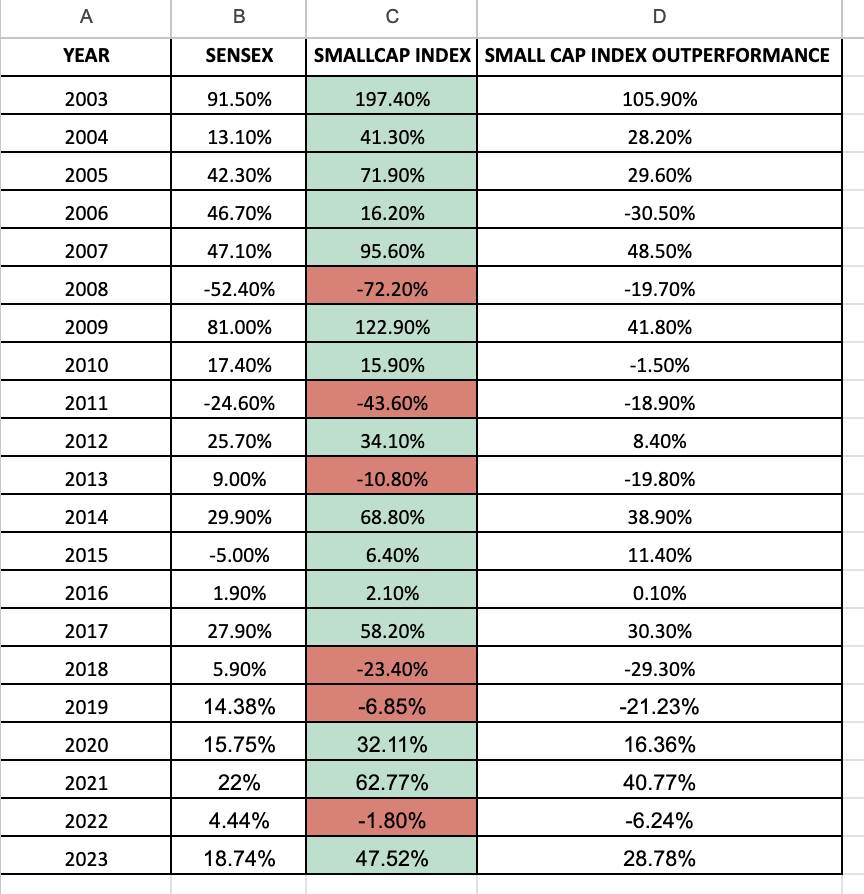

PE of the small-cap index is still comfortable at 31.5, even slightly lower than 32 (at 2023 end)

Let’s also look at the Yearly returns of the small-cap index:

Unless we are in a global boom cycle like 2003-2007, there is a high chance that this year might be a year of consolidation.

Guidance is mentioned in Press Release. 45-50% growth as some talks with customers are in final stages.

However, the things to watch out for are

Disc: Just my thought. No reco to buy or sell

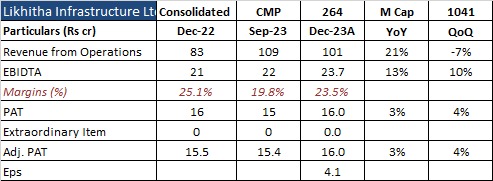

Decent result from Likhitha.

With only 18cr profit in Q4FY23, company will have EPS of around 16.5.

Domestic was 97.4%

Exports were 2.6%, which I guess is gradually increasing.

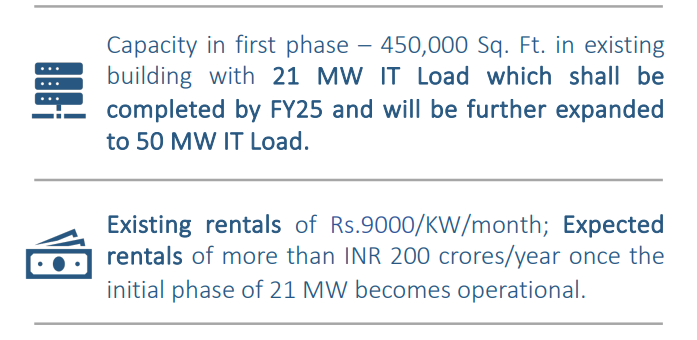

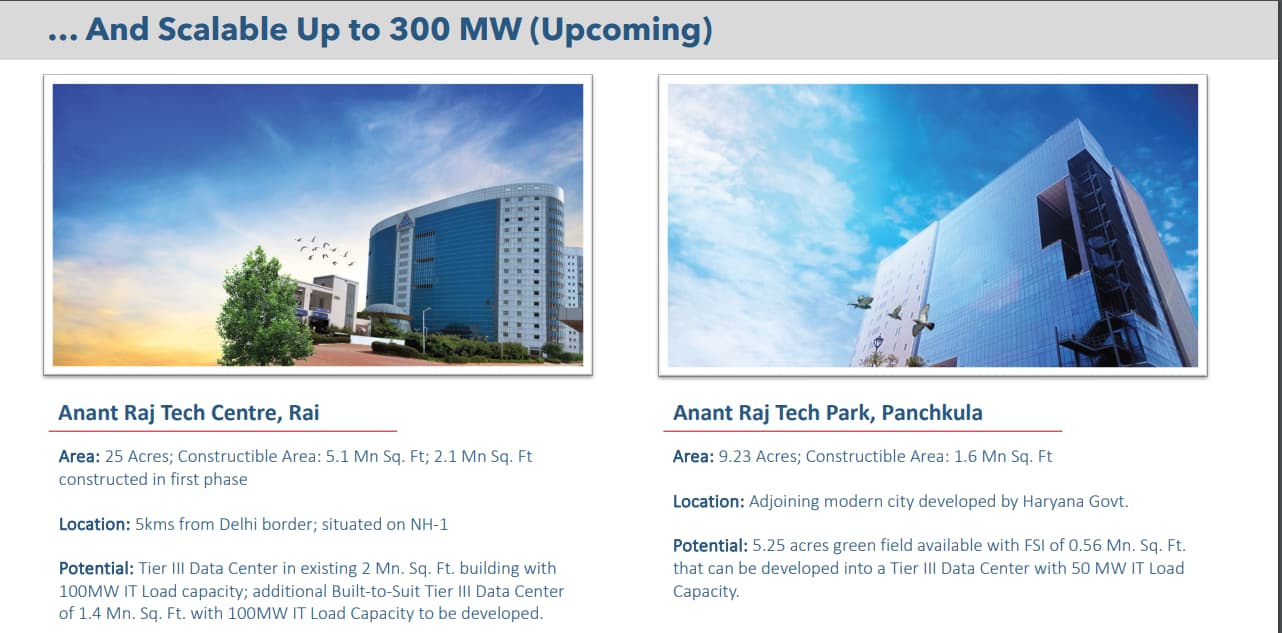

For Anant Raj, these two screen shots reveals its potential.

It is similar to Saregam where people chase that stock for Carvaan ( Including me ![]() ), but their business had potential in music licensing. For Anant Raj, people may chase it for real estate, if plans for data centers get executed as management described, we will be rewarded handsomely. Of course it require patience, which is in short supply, specially now a days.

), but their business had potential in music licensing. For Anant Raj, people may chase it for real estate, if plans for data centers get executed as management described, we will be rewarded handsomely. Of course it require patience, which is in short supply, specially now a days.

Disclosure: Invested

Super results

Going by Management guidelines of 8.25- 8.5 Lac tonne DI pipe production target , we are expecting top line of 8200-8300 Cr for FY 24-25

PAT margin of 13-14% translates to PAT of 1050 -1100 Cr current MCap is 9800 Cr

Hence available at PE of 9.8 -11 FY 25 earnings.

For FY 26 production will be 9.-9.5 Lakh tinned

Very much undervalued