Posts in category Value Pickr

Fermenta Biotech Limited (Old Name DIL – Duphar-Interfran Ltd) (12-02-2024)

All of their profits are from sale of property, their drug business is still in loss, hasnt turned around yet. Not a surprise to me. Vitamin D3 is a commodity drug.

DELHIVERY – One stop solution for shipping and parcel delivery (12-02-2024)

Key messages [rephrased] from Q3FY24 Conf Call:

- Expect growth rates of 15~20% for eCom and 30% for PTL segments in FY25.

- Factors that will help to grow: Service quality, reach of the network, and cost leadership.

- Focus area: Gain heavy volume. In turn, source PTL loads from across the country. Seeded salesforce in 80 cities. Will back them with enhanced marketing spend.

- Incremental gross margins continue at 50% and shall continue in the coming quarters. In the long run, it might settle at 30% – basis 12 yrs. of own historical data. In the very long run, the stable transportation margin [OPM, I think so] shall be at 16~18% plus some delta due to better network engineering.

- OS1 based DispatchOne [SaaS] offering is expected to be monetized from Q1FY25.

How technology, network engineering, and automation act as a competitive advantage? For any logistics company, 3 core assets: Trucks, Infrastructure and People.

- Trucks: Mesh network enables dynamic routing without compromising on the timelines instead of the traditional Hub and Spoke model. Inturn, trucks are used more efficiently: Reduced deadheading, improved axle loading and optimized use of the container space.

- Infrastructure: Automation of the Hubs ensures better throughput: optimal combination of the trucks & trailers, and faster sorting of the parcels and freights.

- People: Higher productivity due to automation first approach. Reduced parcel and freight handling costs. Inturn, lower loss and damage expenses.

Note: Dynamic routing and truck-trailer automation at the hubs have improved the Line-Haul [Mid-Mile] cost significantly in the last 7 quarters.

As of now, the software driven logistics ecosystem of delhivery provides incremental gross margins at 50%. In future, industry players intend to pass general price increase [from inflation] to their customers whereas Delhivery would maintain the same prices, benefitting from its network efficiency. Competitors can replicate Delhivery cost structure and network efficiency only if they invest in the automation of all the core areas and fine tune their systems after spending similar amounts of time.

Disc: Hold a position.

Investing Basics – Feel free to ask the most basic questions (12-02-2024)

yes you seem to be correct however inventory turnover ratio would be an accurate indicator as to analyze the positive/negative effects to working capital as a significant increase may be in normal course if a huge order is received by a company or if it is expected to make a huge quantum of sales in the near future

Jyothy Labs ~ Post acquisition of Henkel India (12-02-2024)

Jyothy Labs Q3FY24 Concall Summary

A) Financial Highlights

Net sales up by 10.6% (lower than volume growth due to price correction) value growth. Volume growth is 11%

EBITDA margin stands at 17.5%

net profit up by y 34.9% for the quarter

Input prices stabilized, therefore sustained margin

B) Key categories performance

Fabric Care sales have increased by 11.9%, focus is also on growing the fast-growing liquid detergent category, which has also witnessed good results.

In Dish wash, sales have increased by 6.7%

Household Insecticide category, sales increased by 5.4%

Personal Care segment, sales have increased by 22.3%, Margo neem, rose, lemon, jasmine, got good response from consumers

C) Strategy (focusing more on volume growth)

1st – increase direct distribution

2nd – focusing on several digital advertising like out-of-home, van operations, newspaper ads for

each brand to reach out to the end consumer

3rd – New Products launches like liquid detergent in Henko and Ujala, new launches of Margo variant

D) Challenges:

The rural economy not picking up

Input price risk (if stable can this yr can earn 16-17% EBITDA margins)

E) Q&A

-

Targeting in 4 yrs at CAGR of 19% but too rosy expect 5-6 yrs or top 12-15% CAGR.

-

Focusing more on organic growth and less on M&A

-

HPC (Health & Personal Care), open for shampoos or home and personal care

-

Henko & Mr White focusing on geographical expansion & in-state growth.

-

Once Rural economy picks in can expect more volume growth in Dish Wash Segment.

Key raw materials used by Jyothy labs —> LABSA, Soda Ash, Palm Oil, etc -

1.1 million outlets reach on a direct basis, by next FY to add 75 k to 100k more shops.

-

Targeting 8-9% of sales as ads spent

-

Once they add a retail shop it takes 12-24 months to show in the expected results (optimum sales target).

-

To increase distribution they need to hire more which means more employee cost. (in next concall can ask for volume growth guidance for FY25)

-

Ecom is 5-6% of topline, liquids do better in e-com, liquid detergent (online & offline) not a major part of wash portfolio, focusing more on the liquid detergent side.

-

distribution reach still has more legs to grow under for Margo

-

currently 23 plants, no plan for adding new as of now, means no major capex, expected maintenance capex of 40 Cr this yr

-

In the near future can do price cut to tackle competitors thereby short term margin impact.

Fermenta Biotech Limited (Old Name DIL – Duphar-Interfran Ltd) (12-02-2024)

Is there anyone still tracking Fermenta?

Looks like there is some turnaround in the business

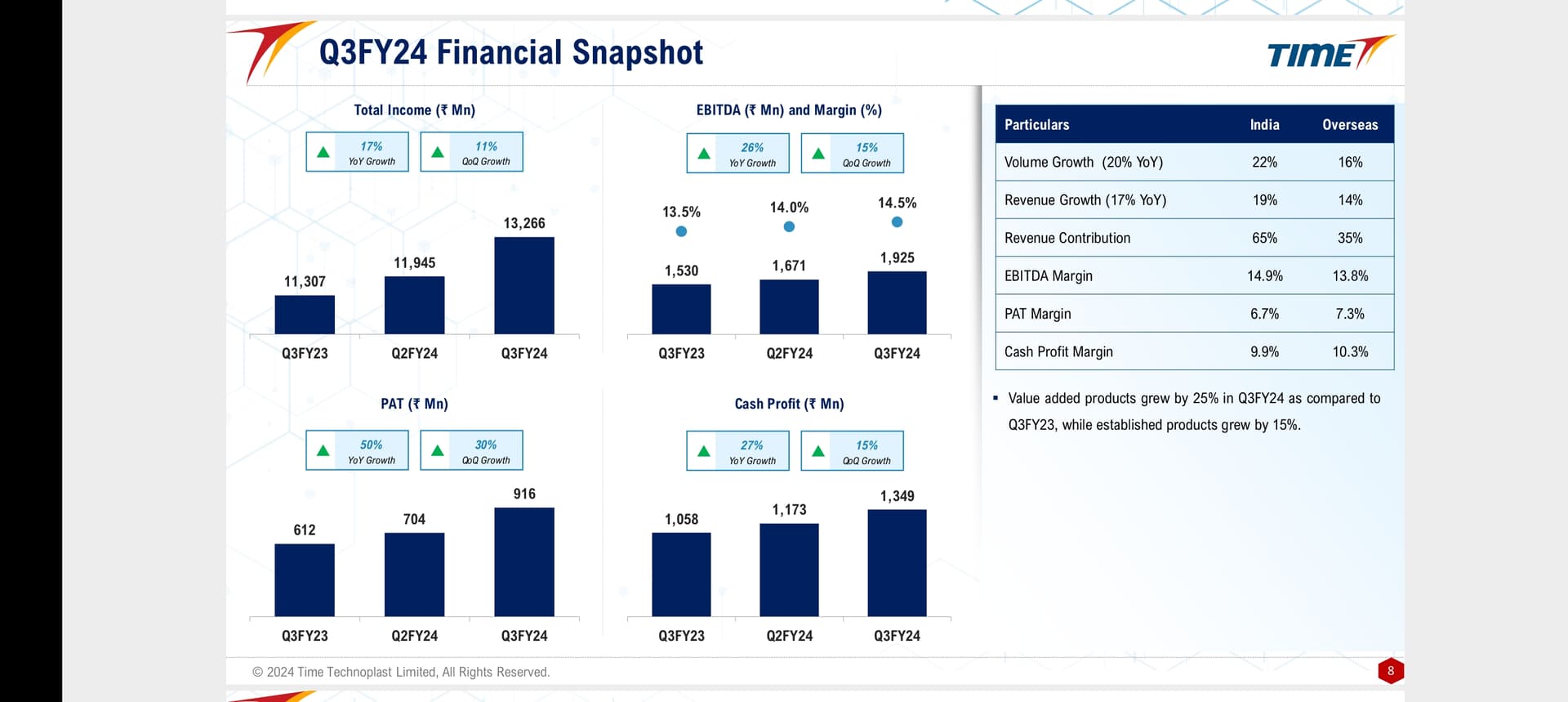

Time technoplast (12-02-2024)

Good Q3 FY 24 Results.

*Revenue up by 17% yoy is at 1326 Cr.

*EBITDA up by 26 % yoy is at 192.6 Cr.

*EBITDA margin is 14. 5 % against 13.5% last year.

*PAT up by 50% yoy is at 91.6 cr.

Priti International Ltd (12-02-2024)

Comparing to the quarter ended on Dec’23, Priti has delivered some good lots within india on Q1 2024 sofar as below (Reference taken from Priti’s Twitter page);

Hyderabad Airport – First lot delivered on Jan 30

Class room furnitures supplied to Bharat dynamics ltd on Feb 01

Modern office Furnitures in Bangalore on Feb 02

Furniture supplied to National Institute of Science, Bhubaneswar on Feb 07

Referring to Q3 result, page 2 – Expenses IV.C – Inventories of finished good /work in progress mentioned as 4.5 Crores (almost 20% of sales revenue) → Probably, this should be part of the above order delivered.

Therefore, we can Waite for the year end annual report to see status of the sales growth and future guidance, and order book.