Finding Multi-Bagger Stocks: What, How and When | The Wealth Formula

MUST WATCH. I FIND LOT OF COMMONALITIES WITH MY INVESTING STYLE TOO. LOT OF ESSENTIAL TICK BOXES FOR A GOOD CHECKLIST IN ABOVE INTERVIEW

Finding Multi-Bagger Stocks: What, How and When | The Wealth Formula

MUST WATCH. I FIND LOT OF COMMONALITIES WITH MY INVESTING STYLE TOO. LOT OF ESSENTIAL TICK BOXES FOR A GOOD CHECKLIST IN ABOVE INTERVIEW

Wow…very nice…how did u get the autographed copy…??

You make a valid point @Kaustav_Gupta

Perhaps I did not put my point across properly. The price differential between the landed cost of captive iron ore & its market price amounts to the extraordinary profits that mining Co.’s like Godawari are assured of. Over the last several years starting 2018, which include the Covid years, the average operating profits of Godawari has been around 24%. Unless there is a drastic/ unprecedented fall, by & large mining Co.’s have enough margins to absorb the shock. Further, if there is indeed such a fall, then iron & steel prices too are likely to fall drastically, thereby wiping out profits for the steel companies. My limited point is that captive mining Co.’s in India with long mining leases still to go are better equipped to handle volatility.

Godrej Properties have delivered another stellar quarter with bookings of 4.34 million sqft having value of 5720 Crores.

I have updated my valuation calculations as per the current quarter results. It seems to be trading at slight premium to fair value.

Please note this is NOT a buy or sell advice. I am NOT a SEBI registered adviser.

Moldtech is into Infra Eng services business. Most of their clientele is from USA and Eu. Currently due to high interest rates, the business is going through headwinds. However I consider this a good opportunity to buy. Few things that may work in favor of the business

These are the few qualitative thesis points, I have in mind. For management guidance on growth of Revenue and Profit, you can refer to the recent concalls

Disc: No reco to buy or sell

Praveen

Couple of observations:

Board of Directors of HBL Tonbo Private Limited (HTPL) have resolved to make an application for striking off the name of the company undersection 24B(2) of the Companies Act, 2013. There are no operations in the company.

Also in the Outcome of Board Meeting Held on 7th Feb 2024 there is a mention of investment in Tonbo Imaging:

Board noted that an amount of Rs. 86.67 crores was invested in 2023. Although, the plan was to

invest Rs 150 crs, a higher valuation was expected by Tonbo for the balance, which was not

accepted by HBL. No further investment in Tonbo is proposed.

So it looks like the relationship with Tonbo has soured and any plans for joint development of missile seekers/other opto electronic equipment have been scrapped.

A sum of Rs 175 crores was approved by the Board for capital expenditure during FY 25.

The largest single item is for Rs 60 crores, for the Lithium lon cell production plant.

There will be no borrowings needed to finance the total capex.

60 Cr for Lithium Ion cells. Not assembly of battery packs but manufacturing of individual cells. The company has been into industrial batteries (VRLA or lead acid) and military batteries (thermal batteries), which are an entirely different chemistry/tech as compared to Lithium Ion. If I am not wrong this is the first time that the company is venturing into Lithium Ion batteries. Not sure if they will tie up with someone or develop the expertise inhouse.

Hey Vineet, when do you update your PF here? If it after 30 days from your initial investment? Or quarterly?

Q3FY24 Concall Notes :

Just beginning of the massive growth journey.

In India total current capacity : 45GW and plan is to add another 100GW over the next decade.

Current orderbook 2600MW.

About 350MW is for 2MW and rest is for 3.3MW.

Will be net debt free by H1 next year.

Interest bearing debt is 450-500cr.

Interest cost will be 30-35cr from Q4 excluding one off charges.

Even these 30crs will become zero in 3 quarters.

Signed agreement for 4MW wind turbines in India, will be commercially available in 2-3 years.

Company is gearing up for 1000MW annual execution.

Numbers will be significantly larger in FY25 and FY26 than the guidance.

Capacity is 2.5GW no need to expand unless we get closer to that number.

Focus is on profitability, historically have been 14-15% EBIT business barring FY17-23 and aiming to get there from FY25.

Expecting to get approval from NCLT in next 2-3 quarters for IWEL merger.

Please ignore any typos and points which I might have missed. Thanks.

Disclosure : Invested

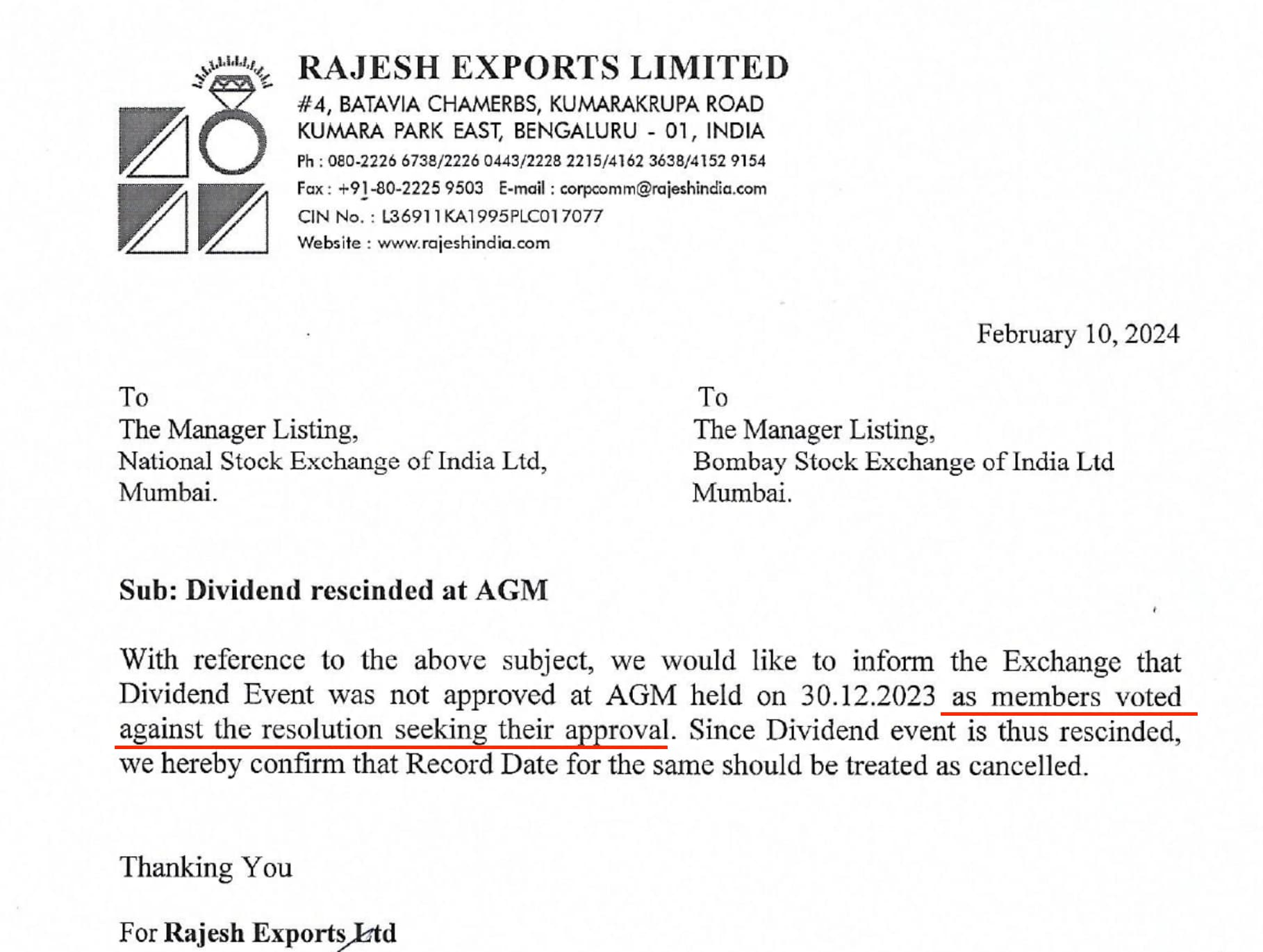

Dividend Cancelled

Was it a stunt ?

Product Profile – This company is involved in the trade of chemicals, plastic, and rubber products such as soda ash, acids, bases, bleaching powder, heat reaction chemicals, polypropylene bags, plastic sheets, and plastic containers. Additionally, the company generates income from loans.

Noteworthy Points:

It would be helpful if someone could examine the company’s profile to determine if there is any suspicious activity taking place.