Not sure on what basis they arrived, but here is the latest from management.

This means more than 2.5 GW for next two financial years.

Not sure on what basis they arrived, but here is the latest from management.

This means more than 2.5 GW for next two financial years.

Apollo pipes is planning to invest 125 cr in Kisan mouldings will be big boost for having strong foot hold in UP and other parts of india.

7bbcdfb6-9dd6-439f-9a33-96014b3ff033.pdf (272.8 KB)

0786ddfe-81e9-4a41-bb0b-26a39fe962c7.pdf (783.6 KB)

Thank you Amol 2021.

Will summarise the con call in some time but my sincere advice to all those who are invested and want to remain invested or as a new investor or even if you want to exit , would be to go through the call at least twice as lot of insights are available. I have already gone through it twice and found lots of nuggets.

Disclosure: Invested … biased and adding in SIP

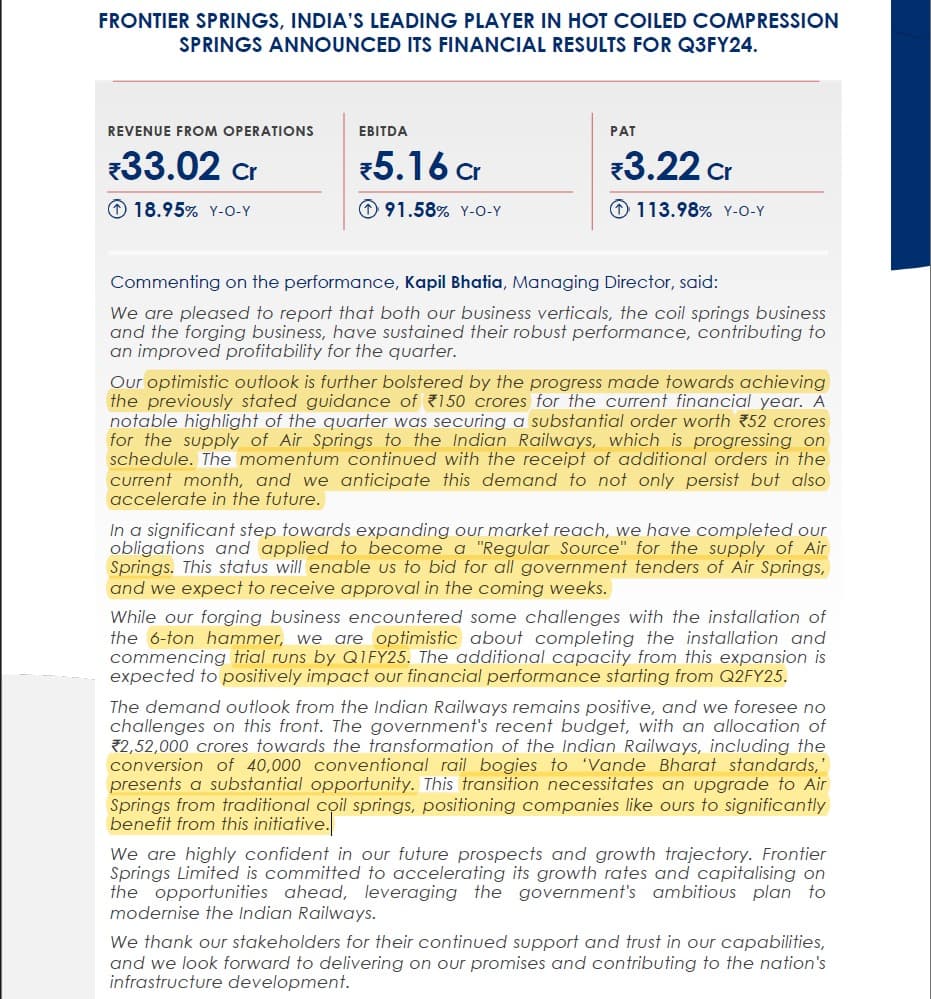

Decent set of nos. with even greater update. Mgmt. is still optimistic about achieving it’s FY24 target of 150 cr. revenue.

Recent budget had declared conversion of 40k conventional rail bogies to ‘Vande Bharat’ standards. This produces a substantial opportunity for Frontier.

6k ton hammer in forging division will start contributing financially Q225 onwards.

Disc: Invested. No transaction last month.

It appears that the situation should be considered alongside the July Rights issue, which was valued at Rs. 141 Crores at Rs. 275 per share. Additionally, it’s worth noting that promoters are consistently purchasing shares from the open market.

From this perspective, it seems like promoters are aiming to accumulate as many shares as possible at a lower price, using various means, including potentially questionable tactics.

While this news might not be favorable for existing shareholders, it does suggest that promoters have a high level of confidence in the future growth of the business.

Looking at historical precedents, similar occurrences in other companies have been overshadowed by sustained business performance. However, it’s essential to acknowledge that while this may impact the stock price in the short term, market outcomes are never guaranteed.

Ultimately, how one interprets this situation depends on individual perspectives and risk tolerance.

Disclosure: Invested

Concall Summary:

Prediction: Next year revenue growth should be 30% (20% from existing parks + 10% from bhubaneswar).

Disclaimer: Invested and biased

Hlo all

I am writing this thread to discuss the sectors which will become multi baggers in long run.

Please share your views

Interestingly, comparing it to Vedant fashion (sorry, may not be apple to apple), the lifystyle apparel business of Raymond(I have extrapolated from avalaible last 2-3 qrtr) does a 3.7cr per store compared to Vedant fashion. However the profitibility looks way different. for any investor , its important that the business is disciplined , efficient, and and generates returns and has simple balance sheet structure.

| Apparel_revenue_Cr | Apparel_EBITDA | No_of_stores | Per_store_AR_cr | Per_store_OP_cr | |

|---|---|---|---|---|---|

| Raymond | 5500 | 850 | 1500 | 3.7 | 0.6 |

| Vedant | 1350 | 655 | 670 | 2.0 | 1.0 |

Also, there was a question in last concall about the ebitda of real eastate business. The management answer was, around 25%, considering it builds on its own land and at an avg rs 20k a sqrft, its too low , compared to something like Brigade enterprises, which does similar %EBITDA including land cost and at an avg 6k a sqrft.

Even though it looks undervalued, but in my opinion economics and efficiency of the company is subpar …I hope restructuring and reorganaising playout, however, from the call it didnt sound like the company is emerging stronger very soon.

Interestingly, comparing it to Vedant fashion (sorry, may not be apple to apple), the lifystyle apparel business of Raymond(I have extrapolated from avalaible last 2-3 qrtr) does a 3.7cr per store compared to Vedant fashion. However the profitibility looks way different. for any investor , its important that the business is disciplined , efficient, and and generates returns and has simple balance sheet structure.

| Apparel_revenue_Cr | Apparel_EBITDA | No_of_stores | Per_store_AR_cr | Per_store_OP_cr | |

|---|---|---|---|---|---|

| Raymond | 5500 | 850 | 1500 | 3.7 | 0.6 |

| Vedant | 1350 | 655 | 670 | 2.0 | 1.0 |

Also, there was a question in last concall about the ebitda of real eastate business. The management answer was, around 25%, considering it builds on its own land and at an avg rs 20k a sqrft, its too low , compared to something like Brigade enterprises, which does similar %EBITDA including land cost and at an avg 6k a sqrft.

Even though it looks undervalued, but in my opinion economics and efficiency of the company is subpar …I hope restructuring and reorganaising playout, however, from the call it didnt sound like the company is emerging stronger very soon.