Systematix research report post results…

Systematix_Aditya_Vision_Ltd_Q3_FY24_Results_Review.pdf (526.3 KB)

Posts in category Value Pickr

See the bright Sun: Aditya Vision (09-02-2024)

Dreamfolks services limited( DFS) (09-02-2024)

Management still is on cautious mode due to change in lounge access eligibility criteria.

Q4 will reflect the actual impact of the issue, even Q3 has some impact but there is no drop in pax QoQ. if Q4 pax cross 3 M then i am sure this has minimal impact on DFS

| FY23 | FY23 | FY24 | ||||||

|---|---|---|---|---|---|---|---|---|

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | ||

| **1.81 | 2.15 | 2.34 | 2.6 | 2.7 | 2.9 |

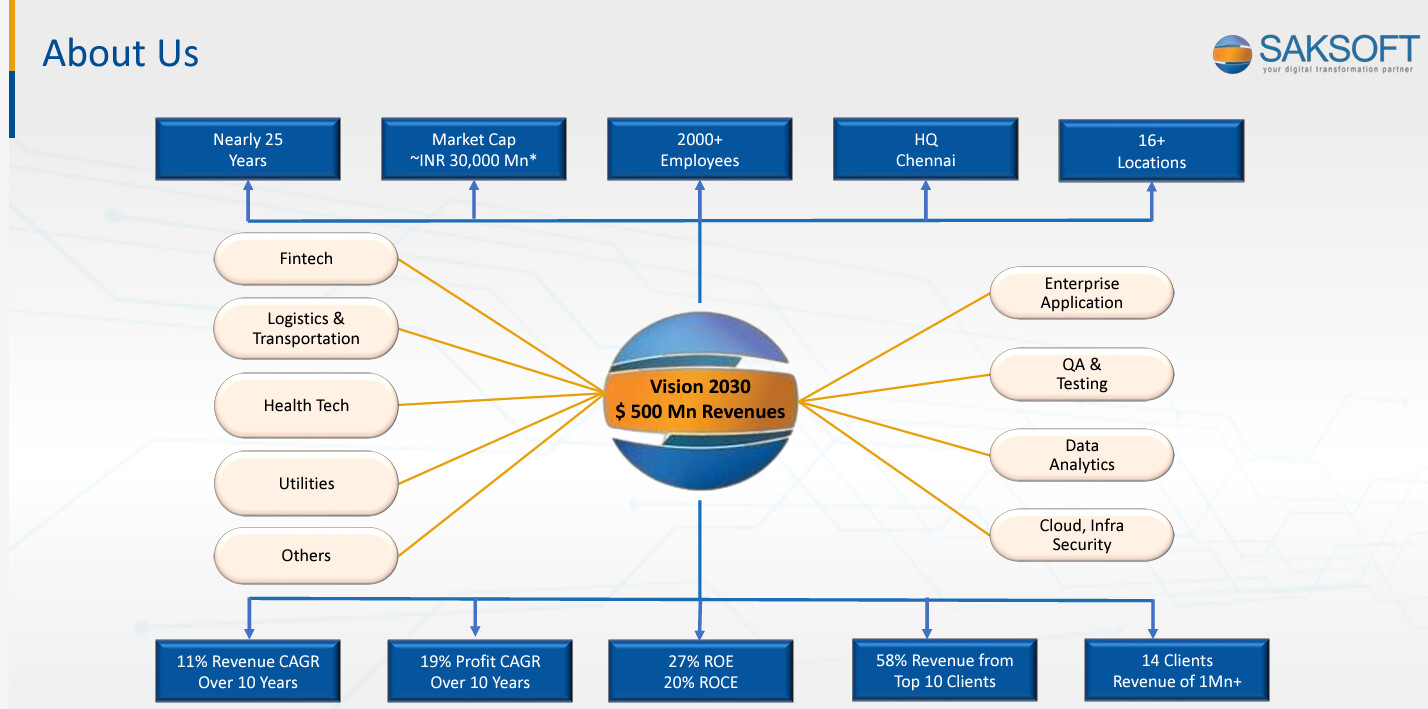

Saksoft Ltd – Value buy in an exploding mobile and tablet market (09-02-2024)

Q3 Concall Highlights:

EBITDA margin reduced due to choose to invest in sales engine to achieve $500mn revenue vision by 2030.

Q3 was tough due to US market head wind, recruitment cost of new employees to achieve $500mn. Q4 will be good, but head winds are there. It is reality check, as wake up call to make company stronger.

All acquired company were profitable when acquired and are profitable now.

Anticipated interest cut in US helps to spur demand.

Q4 EBIDTA margin at 18% is aspirational.

In short, company aspire to grow 22 to 25% to achieve $500mn revenue by 2030.

Disclosure: Invested

HDFC Bank- we understand your world (09-02-2024)

Exactly! Just because HDFC has given no returns in past 3 years, it doesn’t make it deep value. I see HDFC not beating even Nifty or barely beating it, in the next 5 years.

INOX Wind (09-02-2024)

With the recent order win, are there any updated projections for FY25? 1500 MW over next 3-4 years would mean 375 MW per year additional.

HDFC Bank- we understand your world (09-02-2024)

I am also not in favor of investing all money in single stock. My point here is public sentiment/crowd behavior and chasing momentum stocks.

Note: I have highest holding in PP Flexicap fund in my MF investment portfolio ( and PP Flexicap has highest holding in HDFC bank🤣)

Som Distilleries and Breweries (09-02-2024)

This seems a major red flag. Can we have views on this from other fellow members ?

FAZE THREE LTD. –A Textile co. Rising From ASHES to GLORY (09-02-2024)

Similar commentary given by PDS wherein they are expecting some growth to resume from Q4 onwards. But what is interesting to note is that PDS has onboarded Target as one of its client and it is expecting massive ramp up in revenue coming from Target. Target is one of the top 3 clients for Faze three in terms of revenue. Not sure if this development of Target with PDS is going to have any impact on Faze three’s business.

Buy Unlisted Shares (09-02-2024)

Read the DRHP from SEBI website. Specially the industry overview and company’s financial performance. Please don’t get carried away by the growth story.

It’s not that hard to buy shares in unlisted space but getting seller is difficult I guess. I don’t have experience yet though.

In case of Polymatech – the company is raising 750cr entirely as fresh issue. That’s a plus sign. Debt is negligible. The sector is good. Considering Fy23 the PE looks reasonable.

Check YouTube videos of the past management interviews.

You would find a lot of other unlisted share over there but don’t buy them just looking at the valuation. The might not have any plan for IPO anytime soon.

I prefer buying companies who have filed their DRHP already.