I’ll say what I said to Manish ji Sorry Manish ji, I got carried away. I already apologised on the forum. Let me apologise again. Sorry.

But I stand by what I said. This company is run by loons and it deserves the PE it has atm.

I’ll say what I said to Manish ji Sorry Manish ji, I got carried away. I already apologised on the forum. Let me apologise again. Sorry.

But I stand by what I said. This company is run by loons and it deserves the PE it has atm.

Just signup with email address and fill out the demat number.

Add fund through UPI and buy whichever you want.

This platform has smaller lot size compared to other unlisted platforms I have seen.

Once you buy in weekdays, your shares get reflected in demat account next day. You can just login to CDSL and check if it has been credited there.

Done.

Expect Reasonable Growth In Q4FY24, NIM Will Be Maintained At Current Levels: Manappuram Finance

Asirvad IPO may come in Mid-March to early April

This a civilised forum & has no tolerance to uncivilised language & behaviour. Make sure you restrain your expressions.

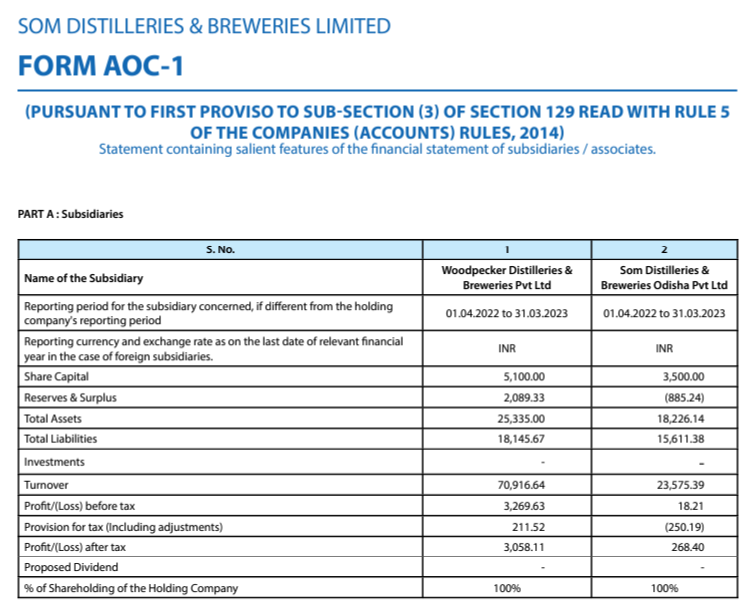

I did some further digging and found below information in the FY23 Annual report of the company. Company had posted 60 crores of profit in FY23, 50% of it came from the subsidiary ‘Woodpecker Distilleries & Breweries Pvt Ltd’ (shown below). 21% of this subsidiary has now been taken by the promoter for meagre 30 crores. It means they have valued the subsidiary at PE of less than 5.

If this is not day light stealing then I don’t know what is. As per them, the whole company should be valued at 280 crores and not 2000 crores (current market cap). I still believe that the promoters should get some discount while raising such capital, but this is not looking good. The shareholders have suddenly lost 10% of annual earnings (20% of profit generated by the subsidiary) in return of 1.5% equity value (30 crores for a market cap of 2000 crores).

Even I am interested in buying Waaree energies. Can you pls share with me how easy it is to buy shares on this Platform? And how is the entire buying process like?

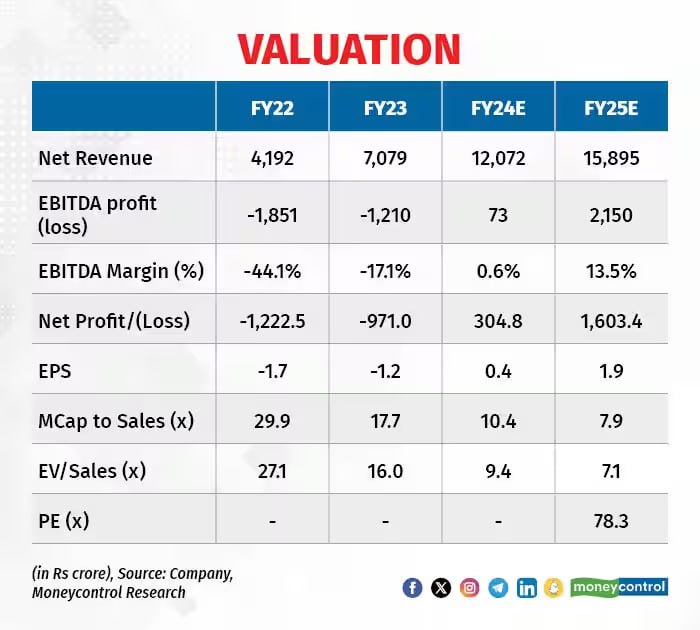

Money Control also concurs the same: Profits – ₹1603cr FY2025

Disc: Holding

Results are very mediocre…Forget the other segments , Saregama continues to disappoint even in the music segment where there is a degrowth…contrast this to tips which had both strong revenue and profit growth…

Today, the company has come out with the notification that Woodpecker Distilleries has become subsididary instead of Wholly owned subsidiary. While the Promoters have infused equity in the subsidiary which is a welcome step as the business needs funds to grow at 50-60% rates, I am a bit surprised by the valuations.

The subsidiary did 262 crores of revenue in FY23 (32.50%) and promoters have taken 21% equity in the subsidiary for 30 crores. It means the whole subsidiary is valued at 142 crores i.e. Subsidiary is valued at roughly 0.5x sales.

While I haven’t seen the subsidiaries’ financials separately, I don’t think it is fairly valued at 0.5x sales. The promoters do bring a lot of knowledge in the company and may deserve some discount but it looks like a very steep discount given that currently, the company is valued at 2x sales in the open market.

Also, doesn’t the company need to get this proposal approved from the shareholders? Can someone please throw some more light on this?