They didn’t mentioned any softness in the demand in their last concall. And the things is other electronics companies are giving good result. This result should be company specific. Let’s see what they say in concall. At least finally they got orders since the IPO.

Posts in category Value Pickr

IREDA: Renewable Energy Powerhouse (09-02-2024)

Well, valuation is the ultimate king in equity market. Market may support insanity in the short term but in the long run valuations always revert to the sector mean for majority of the stocks. The stocks that trade above the sector mean typically have something special about them such as extraordinary growth potential, very high quality management with outstanding and consistent track record of execution and some kind of moat.

IREDA: Renewable Energy Powerhouse (09-02-2024)

Cheer up, stock is down 15% so notionally you are in 2% profit. You can still reenter it if FOMO is too strong ![]()

Tata Investment Corporation: Unusual discount to NAV (09-02-2024)

That’s not how you derive book value of a company. Sorry to state the obvious but in case you don’t know, book value is your asset minus liabilities (or equity capital + reserves).

Tata investment market cap is 27584 crores while its book value is 23000 crores. If you divide them by outstanding shares you get current share price and book value per share respectively.

DCX Systems Ltd (09-02-2024)

Sadly there is no mention of why results are soft in Q3 FY 24…No slide giving qualitative details about the most important quarter i.e. last quarter.

As an investor, we need to check if management hinted at short term softness in last concall or atleast tempered down expectations. If so, I am ok with current quarter. If not, it would be red flag in my books.

Discl – invested recently but need to listen to concall to understand management intent

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (09-02-2024)

Sharing my notes from the Investor meet recently

1.Sales of 121cr in q3 with other income. Pat is 26cr. Comparison with last year Q3 119 percent growth in pat.

-

Growth in rev 57%

-

Phase 1 expansion in full swing and will be operational in april 2024. Check pics in ppt shared

4000MVA to 5500MVA

4.Already working on phase 2 expansion.

Capacity will go to 7000MVA

Turnover of 800-900cr. It will give

Orderbook is 355cr in jan.

Order position is good and good demand in mkt and good precense in renewable sector – solar and wind. Phase 1 will be utilized by this

What drives the margins- a lot of exports of transformers. Not to third world countries but to middle east and us and canada. So standard of quality has to be high. Plant is very efficient. We manufacture transformers in a very efficient manner.

Margins should be sustainable for another one year.

Strength from export perspective – this mkt is difficult to penetrate. Entry barriers are high. Quality has to be highest standard. Customers dont trust from day 1. We have been doing this since 2010 and now customers recognise us and trust us.

Margin in export and domestic- locally margins have improved 15-20% in export it is 30-50% depending on the type of transformer.

Sold 3000MW in 9 months. Turnover this year should be 400-420cr. Next year phase 1 and phase 2 from 7000 MVA will start.

We mfg upto 132KV. Majority is 66KV or less.

More into renewable sector. So oil cooled transformer.

Renewable trf are difficult to manufacture. A lot is required to manufacture it. Realisation varies depending on transformers. Most of sales is to renewable companies. Also transformer is supplied to steel cement oil and gas.

In renewable we compete with small companies . Those whoch have turnover of 100-150cr.

Renewable is 60% of sales. Export is 40%

Split between domestic and export -45% export this quarter and rest local. In export we sell transformer for multiple applications not just oil and gas. Mainly distribution transformers, oil and gas and renewable in exports.

Power class will stay upto 132KV. Portfolio will stay the same but capacity will increase

Margins have increased over last 10 years. What has changed?

-

New plant made 5 years back very efficient

-

Quality standards improved and orders from export customers

3 demand has also increased.

We are anticipating huge demand in renewable sector. Govt is targetting 35-40 GW of renewable each year. Next 5 years demand should continue.

To fully utilise it’ll take 2 years.

30% is North america and balance is midsle east.

Market share in wind and solar will not be more than 15%. Just an estimate.

Prices of transformer – no shortage of raw materials. Some of rm price has come down or become stable. Ceramic insulators are available plentiful.

What is driving transformer demand in north america. – grid as well as renewable and replacement of old transformers installed in 60s.

Any regulatory tailwinds – no subsidy or any support.

Depends on management which area they want to cater to. Voltamp type cos are well placed in normal industrials.

Expansion will cost 30cr. From internal accruals.

Timeline fo completion is 4 months to one year.

Cycle is similar to 2004-2008

Greenfield would cost alot more. We have huge piece pf land. Can go upto 30000mva

More requirements for oil type. Since dry type are expensive. Dey type is used in safety purposes like multiplex basement

No plans for new product lines

Export demand is also high

Disc: Invested and Biased

TAAL Enterprise – cheap valueations (09-02-2024)

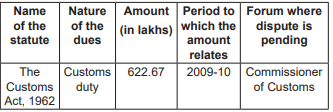

amount is 622 lakh not in crore,

Waaree Renewables – old Sangam Advisors – can it keep on renewing? (09-02-2024)

Part of the Green energy theme i guess!

Max India – Demerger, Will sum of parts be greater than single entity (09-02-2024)

My apologies, but the Title is the old one when Max Healthcare was in the fold.

I did request the moderator in the last line, if this was not noticed. Refer to my older post on Max healthcare, reason why i end up here of that company. Max India – Demerger, Will sum of parts be greater than single entity – #94 by ashwind

Tracxn Technologies (09-02-2024)

very comprehensive, thank you.