FIIs and DIIs started increasing the stake

FIIs and DIIs started increasing the stake

Stylam came with lower sales (-8%) and improved margins leading to good growth in EPS (30%). They are facing headwinds in domestic markets and in Europe, and are very bullish on USA exports. Concall notes below.

FY24Q3

Lost 20 cr. sales due to Israel war. Shipments to Europe affected, not much impact on USA exports

Strong visibility with healthy enquiries for sourcing from global OEM (added many new OEM customers)

Greenlam has global offices and Stylam doesn’t have any global office

Expect US to become larger than Europe. Europe is currently very slow

Domestic laminate business is taking time to scale up fast due to stiff competition. Have been weak in domestic markets

Acrylic:

5.4 cr. in Q3; 20 cr. in 9MFY24 (11 cr. domestic + 9 cr. exports). Utilization level is <10%

Focus has been to sell under own Granex brand vs OEM sales which has delayed scaleup

Expect Government to impose antidumping duty on imports of acrylic surface from China, and this will be a huge boost for them (700-800 cr. annual imports)

Capex

Disclosure: Invested (position size here, no transactions in last-30 days)

May be offsetting due to previous years losses but paid 3% in q3fy24 first time.

Disclosure: Invested

Balrampur Chini’s results were very good. Q4 will be even better taking the annual EPS to 31-32 levels. Hopefully they will come with buyback again next year which can take the stock back to 500 levels!! ( Disclaimer – Please note this is not a recommendation to invest.)

Next year all sugar companies will do better due to restoration of ethanol. FY 25 will see sugar as one of the better performing sectors. Risk-return is quite favourable at current prices.

The following is my assessment of the situation.

In short, a lot depends on the execution skills of paytm. There are reasons to believe the company would come out strongly from this difficulty. I also don’t see anything that would negatively impact paytm for the long run.

Disc: Invested. I always consider myself as a novice investor. No recommendations here. I welcome opposing views, which would help me keep my thinking unbiased.

The WPIL Q3 numbers have disappointed the markets, perhaps due to a decline in profitability. On closer look, this is largely due to lesser other income, something that should be ignored, even when it is high to get a better view of the picture. The other reason for declining profits is the sharp increase in employee remuneration. The mgt mentioned that the environment is pretty robust it is gearing up for bigger volumes for which there has been fresh hiring, not only in India, but also overseas. There is always a lag time before volumes start coming in.

The mgt expects a good Q4, which is always the biggest, volume wise. The current year 23-24 is more of a consolidation year after a 50% growth in Sales last year 22-23. This is only to be expected though there should still be nominal growth. I expect the coming year starting in about a month & a half from now see the Co. graduate to the next level.

The stock has corrected sharply & to my mind is already attractively valued. The pendulum we know swings rather wildly to both extremes of optimism & pessimism n it is up to us investors to benefit from this!!

Any idea what they are doing here?

https://www.bseindia.com/xml-data/corpfiling/AttachLive/132fc1e2-cec1-4c1a-8707-925111027a24.pdf

Q3 results are out.

Good improvement in margin YOY and sustaining on QOQ basis.

Please refer to the RHP of the company. I am attaching it. Go to Page 133.

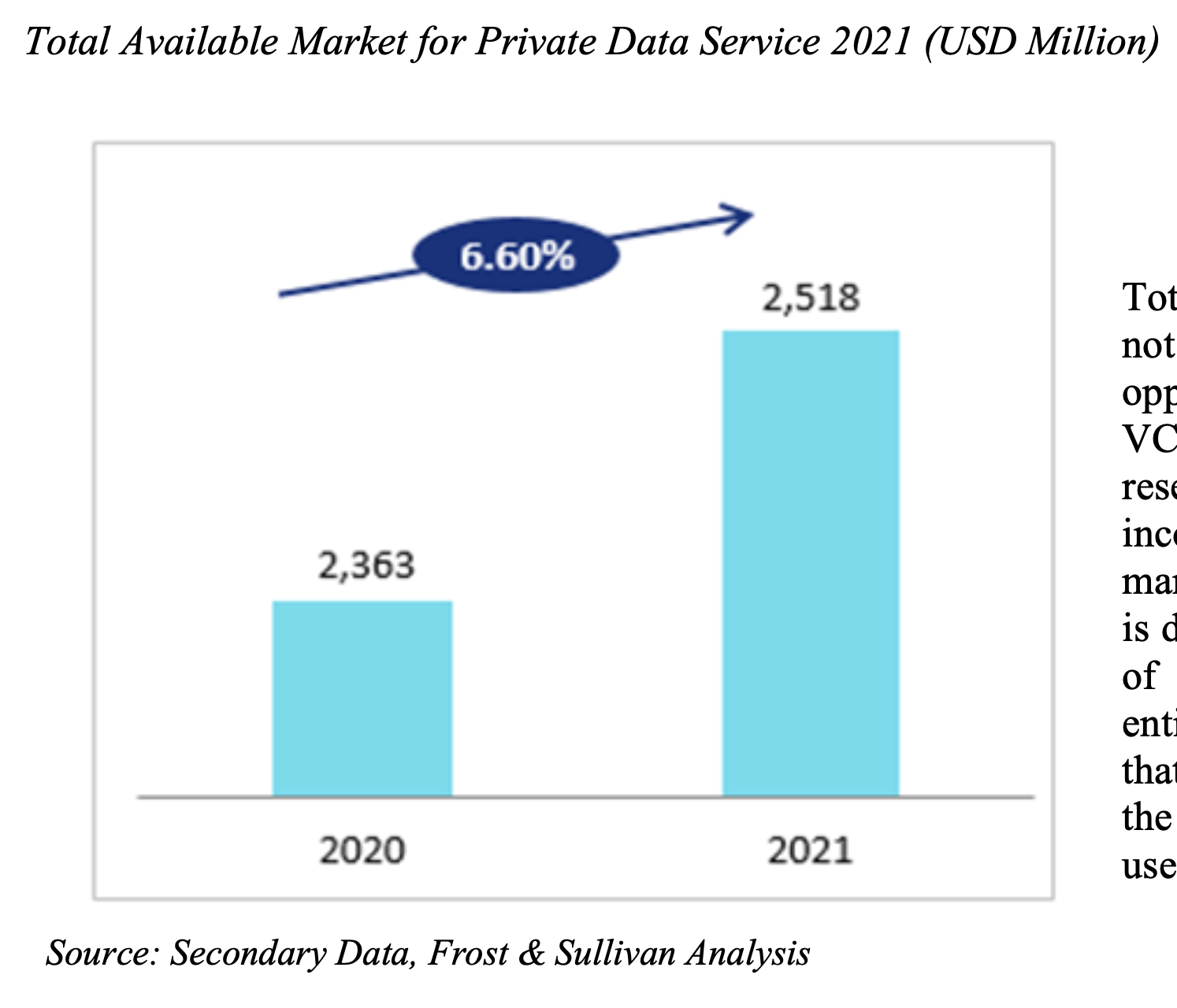

As can be seen from the below image the total revenue that private market data providers can earn annually is in the ballpark of 2.5 Billion USD. Tracxn’s revenue share in the market is less than 1% of the available market.

But I think your question was specifically asking about the number of customers available to capture. Look at the screenshot below. It mentions that as of now the penetration of data service providers in the industry is 50%. This means that Tracxn has 50% of the market available today and these customers are not using any data provider at all.

Please do note that these estimates should be taken with a pinch of salt. I am trying to figure out another data source which can validate the size of this market.

RHP_20221004195631.pdf (6.8 MB)