Yes, also when they buy 75% from Glenmark Pharma, any excess shares they receive has to be sold off within 3 years as part of minimum shareholding norms

Posts in category Value Pickr

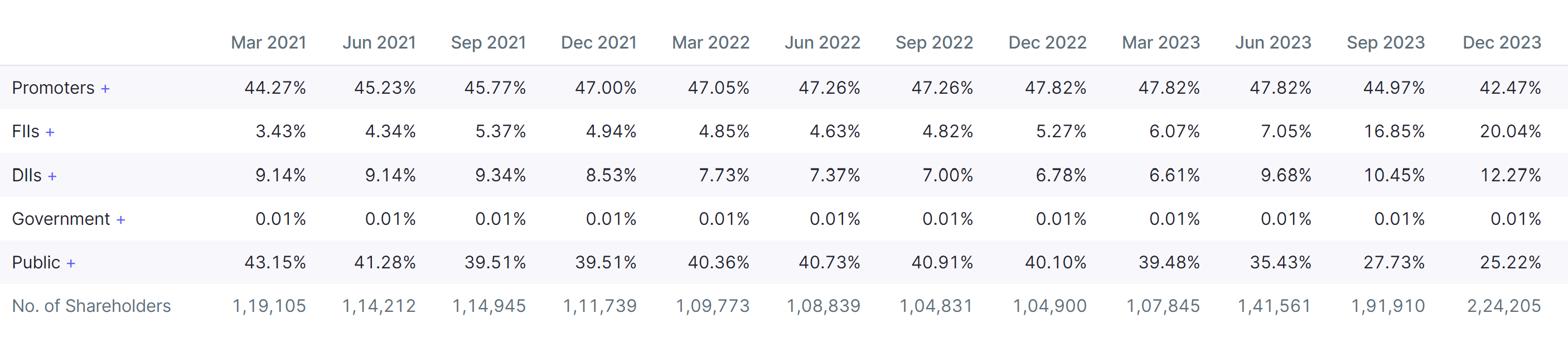

Great Eastern Shipping (GE Shipping) – Possible Sleeper? (07-02-2024)

I think Pe is not the right metric to value shipping business with balatic dry index at an all time high ,revenues would be elevated and shipping is a cyclical buisness.Price to book value would be the right metric to judge this company according to me and it is at an all time high currently.

Carysil (earlier Acrysil) – Kitchen sinks (07-02-2024)

Carysil Limited Q3 and 9 Months FY24 Earnings Conference Call February 01, 2024

-

Our focus on increasing capacity utilization in the quartz sinks category has been steady, with progress reaching 70% by the end of 9 months FY24 and expected to increase further on a quarter-on-quarter basis

-

We expanded our capacity by adding 90,000 units in the last quarter, bringing the total to 1,80,000 units. The demand in this segment remains strong, with capacity utilization of 67% of the quarter ended 31st December 2023

-

Our performance in the US and the UK market continues to be strong. The destocking process concluded and inventory is returning to its normal levels

-

We expect better operating margins in the coming quarters due to various actions taken by improvement in, material sourcing, and business expansion

-

Howdens is the Number 1 trade kitchen supplier in the UK. It has 750 depots. It has 27 granite

models. They sell 10,000 kitchen sinks per week. That’s 500,000 kitchens per annum. Their gross revenue is 3.3 billion pounds with approximately 20% EBITDA margins. That has been a great feather on the cap for our UK team. And we also have received the first order from them -

It’s exciting to inform you that we have initiated the sale of appliances from our new manufacturing setup. By March 2024, our state-of-the-art facility, capable of producing 1 lakh units annually will be fully operational

PayTM (One 97 Communications Ltd) (07-02-2024)

Dear Mr.Aggarwal,

Thank you for sharing the link but I’m afraid I could not go through the content owing to a paywall. Would you mind sending a soft copy to: jai.dlf@gmail.com

Await your kind help and thank you in anticipation of the same.

Best regards

Jai ganesh

Manappuram Finance (07-02-2024)

The performance is unsatisfactory, as gold isn’t contributing to growth in AUM or revenue, possibly due to intense competition from banking entities.

PayTM (One 97 Communications Ltd) (07-02-2024)

I think Paytm Payment Bank had a competetive advantage over other Payment Banks because of Paytm and not the other way. Had they been separate, PPB would also have been a faliure like other PBs.

Small cap frenzy (07-02-2024)

The current market scenario does rhyme so much with your post ![]() . What makes it scarier? Promoters reducing their stakes in these so-called inevitable companies…so basically outsiders see a much brighter future for the company than the promoters who are in the business 24/7 so promoters said okay you may have it then XD.

. What makes it scarier? Promoters reducing their stakes in these so-called inevitable companies…so basically outsiders see a much brighter future for the company than the promoters who are in the business 24/7 so promoters said okay you may have it then XD.

Titagarh

Suzlon

This too explains the scenario well –

Credits – @Worldlywiseinvestors

RACL Geartech Limited (07-02-2024)

Is there any Capex plan as per latest concall ?

Indian Energy Exchange (IEX) (07-02-2024)

The main point regarding Market coupling in the Circular

- The Commission received an overwhelming response on the Staff Paper, with

a total of 127 stakeholders submitting their comments and suggestions. The list of

stakeholders is available on the Commission’s website.- The Commission has examined the comments and suggestions received on

the staff paper. The Commission notes that stakeholders have provided a mixed

view on most of the issues raised in the staff paper. Those in favour of market

coupling have advocated its benefits mainly in terms of improved competition,

increased volumes, lower transaction costs, ease of operation, better services, check

on monopoly, better transmission corridor allocation, integration of cross-border

power markets, and that it will pave the way for reforms, like MBED, SCUC, and the

introduction of financial derivatives. On the other hand, the stakeholders arguing

against market coupling pointed out the disruption that may be caused by market

coupling, the role of power exchanges getting diminished as a bid collecting agency,

the dampening effect on innovation & technology investments, the adverse effect on

Order in 1/SM/2024 Page 4

competition, no improvement in transmission infrastructure utilization, the addition of

another layer in the form of Market Coupling Operator (MCO) and the resultant

increase in transaction costs, adverse impact on smaller traders’ businesses,

violation of power exchange licence conditions, etc. Besides, some of the

stakeholders, like PXIL and the World Bank, shared the results of the simulations

done to support the need for market coupling under the prevailing market conditions.- After carefully examining the suggestions received from the stakeholders, the

Commission felt the need for more evidence-based results to decide on the potential

benefits that coupling may accrue to the market participants and the power system

as a whole. Accordingly, the staff of the Commission carried out several simulations

using bid data from power exchanges to study the impact of market coupling on

volume, prices, and economic surplus, as stipulated in PMR 2021. For the purpose

of the analysis, bid data from IEX and PXIL for the Real-Time Market (RTM) for 40

days in 2022-23 was considered where bids, including cleared and uncleared bids,

were available on both trading platforms. The analysis for the Day-Ahead Market

(DAM) pertains to the months of January, February, and March 2023. A brief

summary of the results is as under:

i. The coupling of power exchanges enables the clearing of some uncleared buy

and sell offers. For example, in RTM, there were times when supply and/or

demand bids were received on one exchange but could not be cleared. When

the bids of the two exchanges were coupled, the cheaper sell offers on the

said exchange were cleared and replaced the high-price sell offers of the

other exchange. Additionally, some high value buy offers were also cleared

after coupling. This led to an increase in the economic surplus.

ii. In the instances where coupled MCP was below the uncoupled MCP on the

dominant power exchange, the overall consumer surplus increased. The

maximum increase in volume in RTM was approximately 250 MW. In most

instances, the economic surplus increased by less than 1% in RTM.

iii. In DAM, the coupling of power exchanges led to an increase in economic

surplus by less than 0.013%. However, in certain time blocks, an increase of

up to 3% was also observed. The maximum increase in volume was

approximately 230 MW (3% of that time block), and the maximum decrease in

Order in 1/SM/2024 Page 5

volume was 100 MW (2% of that time block). The total increase in volume for

the months of January, February, and March 2023 was ~9 MUs (0.08%

increase). The average MCP also increased by 0.3 paisa/kWh (0.06%), and

volatility was reduced by 0.050 paisa/kWh (0.02%). The number of times the

MCP touched the price cap was observed to remain the same over the

analysis horizon.- Based on the results of simulations for coupling in DAM and RTM, it emerges

that there is a possibility of uncleared bids (buy and sell) getting cleared in a coupled

scenario. However, the overall gains in terms of increase in volume and economic

surplus may not be significant. The peak time blocks witnessed an increase in

economic surplus in a coupled scenario, but over a longer time horizon, the gains

remained insignificant. Further, the impact on MCP and volatility varies across

different time durations depending on the elasticity of demand and supply curves.

The Commission finds these results broadly in conformity with the largely accepted

view that under the prevailing market structure, where one dominant power

exchange holds about 99% market share in DAM and RTM, merely coupling bids of

all the power exchanges will not yield substantial improvement in market outcome.- Notwithstanding the results of the simulations, the exercise undertaken, and

the comments of the stakeholders revealed some insights that the Commission felt

were worth taking forward. The insights were in the form of – the need to increase the

depth of the market, the scope for further optimization of system cost, and the need

to enhance power system reliability and flexibility through appropriate market design.

The Commission feels it imperative to bring in more participation in the market,

which would not only improve supply availability and encourage competition amongst

suppliers but also facilitate a platform for optimizing the resources. While the

coupling of bids in the present market structure marginally contributes towards this,

other alternatives need to be explored in pursuit of increasing market depth, system

and cost optimization and grid reliability.- The current power market is visibly a demand-driven market, as we have

witnessed in the recent past. Thus, to increase the depth, commensurate supply has

to be necessarily brought in to fully utilize the efficiency gains of the market platform.

Order in 1/SM/2024 Page 6

Resource adequacy framework is being evolved to ensure the adequacy of supply to

meet demand in all time horizons reliably and at the least cost. But this will take time,

and as such, the Commission feels it is expedient to explore all options to optimally

utilize the existing capacity. Currently, most of the generation is tied up in long-term

purchase agreements. While the efforts to bring these contracts to the market are

underway through various policy and regulatory measures – for instance, by

requiring the generators to bid their un-requisitioned surplus (URS) into the market,

defining transmission allocation principles accordingly – there still remains last mile

scope for optimization after all trading options for a specific time block/duration have

been exhausted

Ujjivan Financial – Small Finance Bank (07-02-2024)

With same management of both the entities what are the reasons for your concern