Thanks Vikas, Mahesh.

The pdf gives a link -which looks like a sharepoint portal. Tried logging in using hotmail, but unable to login to their portal – getting an error.

Will wait and check out whether it gets fixed soon

Thanks

Thanks Vikas, Mahesh.

The pdf gives a link -which looks like a sharepoint portal. Tried logging in using hotmail, but unable to login to their portal – getting an error.

Will wait and check out whether it gets fixed soon

Thanks

The % contribution of various products is linked to the chemical composition of the tyre.

for eg. Carbon black as a proportion of raw materials is about 20-25% in a tyre, which gets recovered.

Its just the nature of the pyrolysis process.

Even the fuel oil is a recovered oil. Which acts as a substitute for crude oil product used as fuel by their customers.

Sodium silicate is more to do with using the immense heat generated from the process as effectively as possible. The company evaluated several options, including setting up a power plant, before deciding that this is what makes most economic sense to them. There is no issue in availabilty of the raw materials (silica and soda ash), the capex for this plant is very small, and the end product has wide usage and is easily saleable.

Regarding revenue – for now they have just one plant. So I am guessing that the volume they are able to produce would be fairly constant, with normal fluctuations. Any change in numbers would then be driven more by realisations till their new plant comes up in a few months.

Dhampur Bio is converting existing ethanol plant to dual feed. To my mind this is the best thing to do at low capex of 50cr (funded 75% by soft loan). So full cane can go for sugar which is at higher margins and utilise the idle ethanol capacity using grains. Give the company another 6 to 9 months and performance will be among the best – EPS will double to Rs. 25 (annualised) and min share price 250 ( 70% upside).

Disclaimer – Please note this is not a recommendation to invest.

Fellow startup founders coming out in support

A possible way forward is for RBI to identify corrective actions (something to similar to what USFDA does) and keep the doors open for reversal of ban rather than decisions which completely kill the business of PayTM, keeping in mind it is a public company with millions of shareholders. Assuming here that there is no fraud angle to the whole thing and it is more of compliance issues of operational nature, Government should also support in whatever way it can.

i had pointed this out in May 2023.[quote=“Aarti, post:69, topic:82007, full:true”]

Valuation seems little on higher side given sales and margins have stagnated. also price has moved up more than 6 times in 3 years.

[/quote]

Came across this article on IRM. Clearly calls out that IRM is professionally managed under an chairmanship of an ex-IAS. Chairman has lot of credibility with government. He also has a commitment from promoter about non-interference.

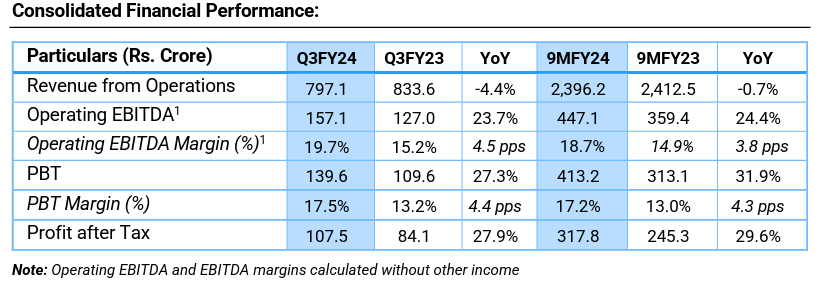

Q3 FY 24 Results. Decent Results.

Value added products save the day for Usha Martin.

Operating EBITDA up 23.7% Y-o-Y to Rs. 157.1 crore

PAT increases 27.9% Y-o-Y to Rs. 107.5 crore

Consolidated Performance Overview – Q3FY24 vs. Q3FY23:

• Revenue from operations decreased by 4.4% Y-o-Y to Rs. 797.1 crore in Q3FY24

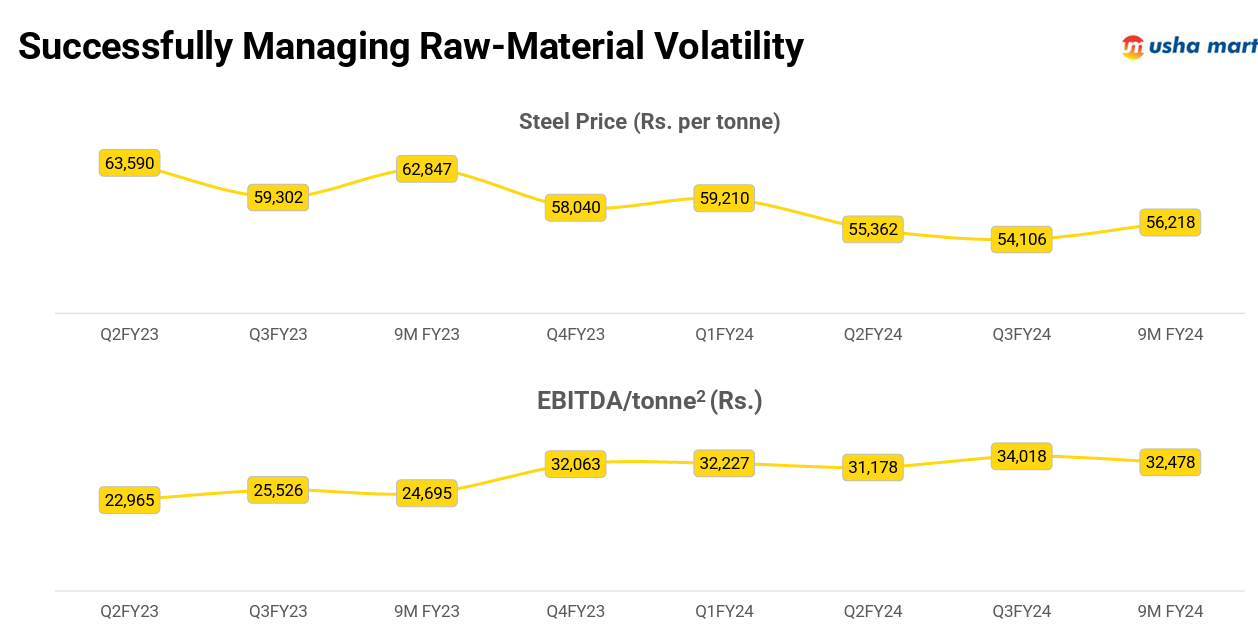

o The core Wire-Rope segment revenues held steady, despite Y-o-Y reductions in sales volumes

and raw material prices, supported by enhanced realizations

o Realizations were supported by continued contribution from international markets and value-added

offerings

• Q3FY24 Operating EBITDA stood at Rs. 157.1 crore as against Rs. 127.0 crore, higher by 23.7% on a Y-o-Y basis .

• In the quarter, the Operating EBITDA margin was recorded at 19.7%, an increase from 15.2% in Q3FY23

o The Company’s sustained strategic emphasis on value-added products, coupled with its

expanding global presence, has been instrumental in enhancing margin performance consistently

o EBITDA margins including other income for Q3FY24 stood at 20.4%, compared to 15.8% in Q3FY23

• In Q3FY24, PBT amounted to Rs. 139.6 crore, registering a 27.3% Y-o-Y increase from Rs. 109.6 crore

• In Q3FY24, PAT amounted to Rs. 107.5 crore, registering a 27.9% Y-o-Y increase from Rs. 84.1 crore

• Basic EPS stood at Rs. 3.53 for the quarter as against Rs. 2.76 Y-o-Y

Commenting on the performance Mr. Tapas Gangopadhyay, Non-Executive Director said, “

Our strategic focus on high value wire ropes has ensured continued strong profitability, with our Operating EBITDA growing at 23.7% YoY during the quarter. However, this quarter had subdued contributions from our Wire & Strand and LRPC segments which impacted topline.

Capex: Our wave 1 Capex program, poised for commissioning, is a testament to our commitment to expanding our product portfolio in high-end value-added products across our business verticals. This strategic investment also reflects our ambition to set a new benchmark for excellence and to solidify our standing as a premier global player in the wire rope sector.

Looking ahead, Usha Martin is well-positioned to leverage its core strengths to drive future growth. Our improved financial and operational standing forms the foundation of this strategy. We are particularly confident in the strength of our in-house manufacturing and R&D capabilities, which, combined with our diverse product range and dedicated after-sales service, position us to effectively meet and adapt to global market challenges.

Our extensive network and established brand reputation further reinforce our capacity to secure sustained growth and value creation for all stakeholders.”

Press release:

c08021b6-4a35-496a-adab-d11fb14728b3.pdf (bseindia.com)

Investor Presentation:

b5b4658c-f563-4265-b79d-3274c99bfb7a.pdf (bseindia.com)

Discl: Invested from lower level.

Link is there now, found it in screener

(post deleted by author)