Why is the stock falling? Anything related to the fundamentals or just a correction?

Posts in category Value Pickr

SmallCap Hunter : Trying to find the dark horses with triggers (05-02-2024)

@puran_tak …i think healthy company valuation as compared to its peers and business prospects is driving force.

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (05-02-2024)

Om…Pls correct me if my understanding is not inline with this thread and ongoing PSU,Power rally.

To me hydrogen enthusiasm has been priced already …since it is simply an end product of wind & solar power generation.

During weekend while travelling, i overheard youngsters discussing NHPC at a very remote village in south-west of gujarat…I was wondering how to look at such situation where renwable investment has became nextdoor enthuasiasm…many people have moved to equity from savings partially if not fully.

if hydrogen(power,energy,hydrogenation) is the new kid in the town for its possible incremental usage in power. why i say possible usage in power ? because i think energy usage like steel, chemicals through hydrogenation is already known.

Hence with hydrogen theme as a ride, only large companies/MSU might have steam left in them for going an extra quarter or two or year at maximum.We may have smaller companies who are into engineering,piping,equipment etc…but they are an engineering companies following an order book investment cycles.

I see multiple smallcase has shown ~76% CAGR past 3 year on renwable/Green theme.

My query is – what can one study/focus inorder to identify sustainable growth in revenue for a company engaged in renwable energy.

Uni Abex Alloy Products (05-02-2024)

hello, I’m not sure. but the following screenshot has got me worried. why trade receivables and inventories cost so much?

Fine Organics – Niche Player in Specialty Chemical (05-02-2024)

Fine Organics — Q3 FY’24

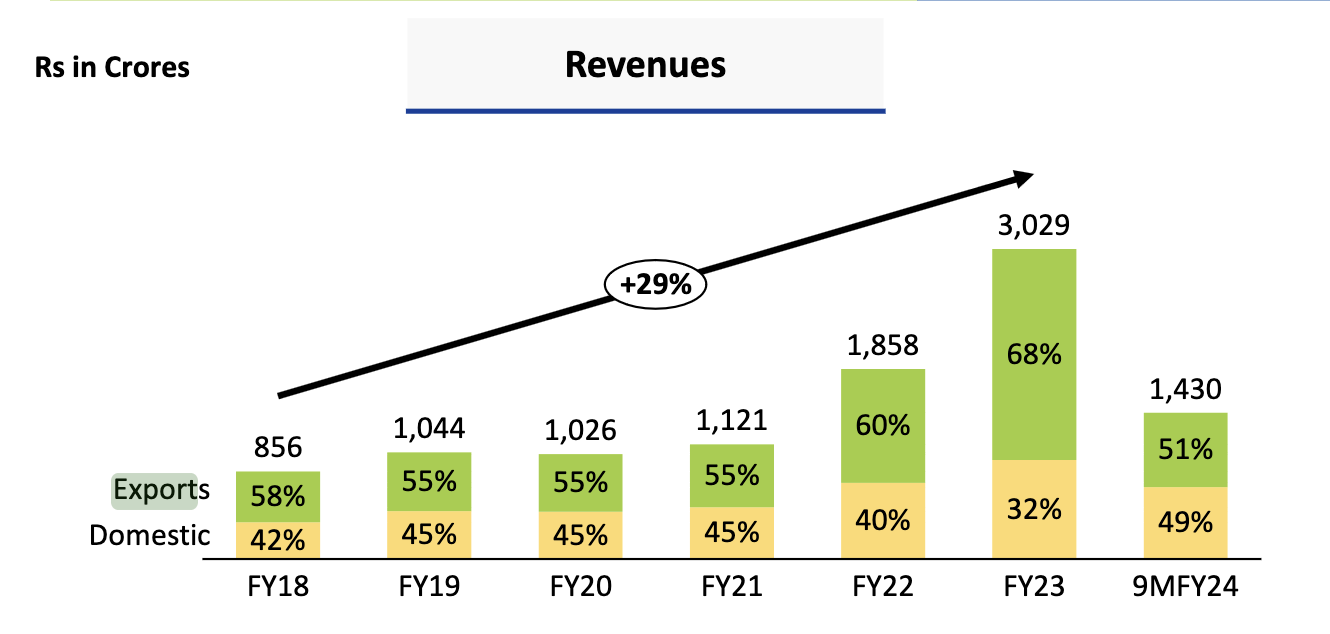

I had already posted revenue forecasts for Mar FY’24, and so far it looks on track with TTM revenue standing at 2173 Cr after Q3 results. In this post, I also want to touch upon a product called Erucamide which is, in my opinion and study, one of the reasons for the fall in demand.

Erucamide is a primary fatty amide that serves as a crucial releasing agent, antistatic agent, and anti-sticking lubricant for polyethylene (PE) and polypropylene (PP). Erucamide is one of the larger contributors to the company’s revenue and they sell them in various formulations for example:

Finawax-e (Erucamide):

FinaFog (PAs, PEs, PPs):

Finalux G 1600

Erucamide, as seen from the examples above, is used in lubricants, plastics, surfactants, automobile interiors and more. The Erucamide market size is expected to develop revenue and exponential market growth at a CAGR of 3.5% during the forecast period from 2023–2030. The growth of the market can be attributed to the increasing demand for Erucamide owning to the Plastics Industry, Ink and Paint Industry, Rubber Industry and other applications across the global level. That being said, in the short term due to the poor economic performance, most international markets are witnessing a massive drop in demand for Erucamide.

Also, China who was a big importer of PP(Polypropylene) has now started meeting its requirement through domestic manufacturing, again hitting FineOrg’s export opportunity.

Remember, Fine organics depends a lot on exports, and in FY’23, FineOrg’s split between domestic and export market was 32% and 68% respectively. That very split has now changed to 50-50% by Q2 FY’24. The exports business is a high margin business, and hence margins are on a declining trend at the moment.

FineOrg’s long term business prospects are still in-tact, and there is no fundamental problem in the business itself. But the short to medium term forecasts don’t look positive. A lot of this is already priced into the stock, and it will not receive the premium valuation it once used to command until the export demand starts to recover. Please note, that it is highly unlikely that this recovery is going to be sharp, instead it will take several more quarters before the prospects start to improve. Another risk to note is the constant FII selling, but the positive takeaway is the promoter holding standing firm at 75%. It might end up being a game of patience.

Anyone looked at Somany Ceramics (05-02-2024)

Thanks for your response @ranvir

Also, do you know why margins of Somany Ceramics have consistently been 4-5% lower than those of Kajaria Ceramics? Both have 90% revenues from tiles and 10% from bathware, both have similar product quality, distribution network etc

Screener.in: The destination for Intelligent Screening & Reporting in India (05-02-2024)

Thanks @kowshick_kk … I will still request to add a filter (if possible) so that I could permanently filter out some companies to appear in my watchlist…

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (05-02-2024)

yes, De nora India is a MNC -a part of De nora group of Italy. They are the leaders in electrode manufacturing & maintenance for fuel cell and Electrolyser.

Recently the parent company has entered in to collaborative agreement with H2U – US based company to manufacture electrolysers