Anyone know how the “Company is expected to give good quarter” is derived at?

More importantly is it reliable ? ![]()

Anyone know how the “Company is expected to give good quarter” is derived at?

More importantly is it reliable ? ![]()

I think March they will kick start their production plant from telegana unit one. Hope topline and bottom will grow 2 to 4x in the next 3 to 5 years… Invested around 170 range with no action till 2027.

Source: Con-call decoder

GMM Pfaudler LtD

Current Operational Performance:

The order intake in Q3 displayed a substantial 20% growth compared to the previous quarter, boosted by a significant systems order worth $11.4 million from the U.S. market.

The international business experienced a noteworthy increase in order intake, placing a strong emphasis on establishing a robust backlog for the upcoming year.

A dedicated effort to diversify away from GlassLine was visible in the international business, particularly through advancements in non-GlassLine technologies, specifically the mixing platform.

Verifiable efforts to enhance profitability and cost efficiency were observed in the international business, focusing on consolidating footprint and improving profitability in the GlassLine business.

Future Outlook:

Management expresses confidence in the future outlook, with a clear focus on enhancing profitability and cost efficiency.

The priority is to build a robust backlog for the upcoming year, with a strong emphasis on enhancing order intake and sales performance.

The international business is anticipated to continue its growth trajectory, with a targeted approach to diversify away from GlassLine and improve profitability in non-GlassLine technologies, particularly in the mixing platform.

Management is optimistic about the growth potential in the service business, emphasizing response time and spare parts availability.

Concerns:

Other Points:

It doesn’t tick all the boxes especially when it comes to MOAT and pricing power but the way the new promoters are steering the company and industry tailwinds does tickle my interest, Do you have any thoughts on this?

About the company –

Indo Tech Transformers Ltd was, established in 1976 is one of the leading transformer manufacturing Companies situated in Southern India having manufacturing facilities at Kancheepuram in Tamil Nadu. Over 56000 Transformers of different ratings up to 245 KV are in service in various Substations and Industries across India and around the world.

The Company’s facilities are established keeping in mind the best available infrastructure and with state of the art equipment’s for manufacturing and testing. The Extra High Voltage (EHV) transformers facility is totally dust free to enable manufacture transformers under very sterile conditions. The testing lab accredited by NABL equipped to carry out all routine and special tests as required by various national and international standards.

Indo Tech Transformers Limited is engaged in the business of manufacturing Power, Distribution, Invertor, Convertor special application transformers, catering to various industries like Transmission, Generation, Hydro, Wind, Solar, Steel, Cement, Textiles, Utilities, DESCOMS etc.

Among our clients are some of the renowned companies like TNEB, NTPC, ADANI, L & T, ABB, SIEMENS NLC, VESTAS, DVC, GAMESA, BGR, SUZLON, TATA PROJECTS, KEC INTERNATIONAL, REGEN POWER TECH, RELIANCE, WALCHAND, TKIS, DOOSAN, GE etc. and leading Hotels, Hospitals, Steel and Cement Plants etc. Our transformers are in service at many Ferrous and Non-Ferrous metal industries throughout the country. Some of our main customers include companies like JSW steel, Jindal Steel and Power, BALCO, Jayaswal Neco Industries etc. Additionally, we have served industrial clients through various leading electrical consultants like M.N. Dastur & Co, EIL, Mecon, Fichtner, PGCIL, Avant Garde, TCE etc. We are also approved by leading Inspecting Agencies like RITES, LLOYDS, CPRI, BUREAU VERITAS, TUV, SGS etc. (1)

Promoter Change

In Sept 2020, Shirdi Sai Electricals Ltd (SSEL) acquired 69.3% stake in the Co from Prolec GE Internacional, the erstwhile promoter. Consequent to the change in controlling stake from Prolec GE to SSEL, the Co has entered into a Transitional Trademark License Agreement for using the brand name “PROLEC” and shall pay 2.5% of the turnover as royalty for the brand usage to Prolec GE Internacional. [2]

| Narration | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Trailing | Best Case | Worst Case |

| Sales | 93.86 | 156.91 | 189.87 | 148.81 | 220.17 | 213.39 | 205.33 | 206.00 | 280.07 | 370.90 | 417.32 | 491.19 | 412.79 |

| Expenses | 108.83 | 166.39 | 190.80 | 151.74 | 221.37 | 215.47 | 203.43 | 194.72 | 257.96 | 334.57 | 373.19 | 439.25 | 398.61 |

| Operating Profit | -14.97 | -9.48 | -0.93 | -2.93 | -1.20 | -2.08 | 1.90 | 11.28 | 22.11 | 36.33 | 44.13 | 51.94 | 14.18 |

| Other Income | 10.89 | 16.69 | 12.76 | 1.79 | 4.55 | 1.24 | 5.42 | 2.92 | 1.69 | 2.66 | 4.27 | – | – |

| Depreciation | 2.99 | 5.18 | 5.35 | 4.82 | 4.74 | 5.19 | 4.79 | 4.82 | 4.52 | 4.82 | 5.31 | 5.31 | 5.31 |

| Interest | 11.73 | 5.77 | 2.45 | 3.11 | 2.30 | 2.36 | 2.43 | 3.02 | 6.80 | 8.47 | 3.79 | 3.79 | 3.79 |

| Profit before tax | -18.80 | -3.74 | 4.03 | -9.07 | -3.69 | -8.39 | 0.10 | 6.36 | 12.48 | 25.70 | 39.30 | 42.84 | 5.08 |

| Tax | – | – | – | 2.21 | – | – | -1.82 | 0.07 | 0.29 | – | 5.55 | 14% | 14% |

| Net profit | -18.80 | -3.74 | 4.02 | -11.27 | -3.69 | -8.39 | 1.92 | 6.29 | 12.19 | 25.70 | 33.75 | 36.79 | 4.36 |

| EPS | -17.74 | -3.53 | 3.79 | -10.63 | -3.48 | -7.92 | 1.81 | 5.93 | 11.50 | 24.25 | 31.78 | 34.64 | 4.11 |

| Price to earning | -3.38 | -49.44 | 49.62 | -19.50 | -48.45 | -13.19 | 40.30 | 14.55 | 18.84 | 7.09 | 29.87 | 29.87 | 17.59 |

| Price | 59.90 | 174.45 | 188.20 | 207.35 | 168.65 | 104.40 | 73.00 | 86.35 | 216.70 | 171.95 | 949.30 | 1,034.84 | 72.22 |

| RATIOS: | |||||||||||||

| Dividend Payout | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||

| OPM | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.93% | 5.48% | 7.89% | 9.80% | 10.57% | ||

| TRENDS: | 10 YEARS | 7 YEARS | 5 YEARS | 3 YEARS | RECENT | BEST | WORST | ||||||

| Sales Growth | 16.50% | 10.04% | 10.99% | 21.79% | 32.43% | 32.43% | 10.04% | ||||||

| OPM | 3.43% | 4.35% | 5.61% | 8.14% | 10.57% | 10.57% | 3.43% | ||||||

| Price to Earning | 26.71 | 22.13 | 22.13 | 17.59 | 29.87 | 29.87 | 17.59 |

Risks

High client concertation risk

Stiff industry competition

Volatility in raw material prices

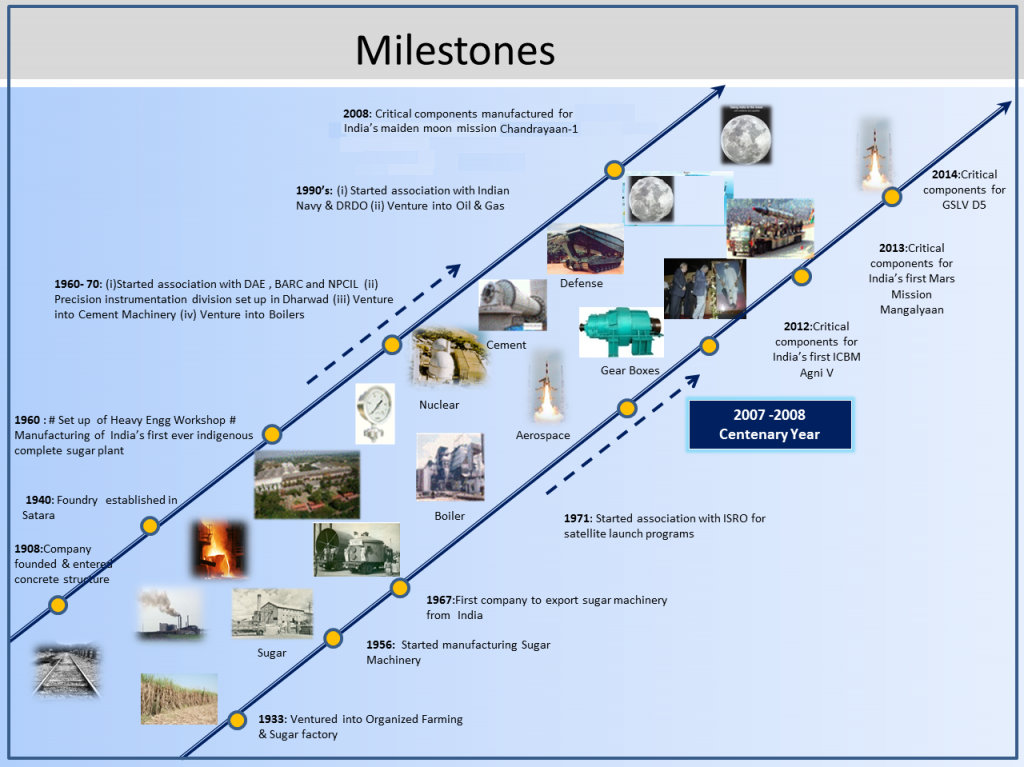

Walchandnagar Industries Ltd.(WIL) , established in 1908 is a Heavy Engineering Company with a presence in Strategic Sectors like Defence, Nuclear & Aerospace and Industrial Products like Gears, Centrifugals, Castings and Gauges. Certified for ISO 9001:2015, WIL also has a presence in Oil & Gas, Railways and in EPC sectors through its offerings for Sugar Plants, Co – Generation Boilers and Cement Plants.

Walchandnagar Industries Limited (WIL) is an ISO 9001: 2015 certified Indian company with global presence and diversified business portfolio in Projects, Products and High-tech Manufacturing. Carrying a legacy of more than 100 years of Engineering Excellence, WIL has established its name as one of the best in its operational areas. WIL is known for pioneering achievements in Indian engineering industry and for its contribution to nation building activities. WIL is a listed company on the BSE and NSE stock exchanges in India.

WIL has a strong engineering, project management and manufacturing infrastructure to undertake projects and supply of machinery and equipments, in the fields of Nuclear Power, Aerospace, Missile, Defence, Oil & Gas, Steam generation plants, Independent power projects, Turnkey Cement and Sugar plants. WIL has a large proven reference list of satisfied customers across the world.

First to Manufacture

* *Critical components for Nuclear Reactor*

* *Main propulsion gear boxes for Indian built Navy Frigates*

* *Components for Satellite launch vehicle for ISRO*

* *Critical components for 235 MW & 500 MW Nuclear Power project*

* *One of the largest Optical Telescope in Asia*

* *Critical components for India’s first Moon mission **“CHANDRAYAAN-I”***

* *Major critical components for India’s Intercontinental ballistic missile (ICBM) program **“Agni V”.***

* *Critical components for India’s first Mars mission **”MANGALYAAN”.***

First ever

Certifications

Compliance to Various Codes

BUSINESS AREAS

–

WTG

Walchand Technology Group (WTG) is Technology & Engineering Solutions Group of Walchandnagar Industries Limited (WIL) powered by a dynamic and dedicated team of qualified and trained engineering professionals, with a judicious mix of domain and discipline experts. WTG has harnessed in-house knowledge and ability garnered from over 100 years of engineering achievements and experience, to provide a complete range of consulting engineering services in the following sectors

A. Energy – Nuclear, Thermal Plants

B. Oil and Gas – Eg. Distillation Column for Oil India

C. Defence – Submarines & Ships

D. Design Engineering and Execution of Complex Projects – Eg. Sodium Coolant System for 500 MW FBR at Kalpakkam Bhavini

E. Special Purpose machine and R & D Projects

Availability of Software and hardware tools at WTG and access to expert panels of agencies and consultants with specific domain expertise in nuclear, electrical engineering, as well as controls and instrumentation give a distinct advantage.

Prominent Clients list include Nuclear Power Corporation of India limited (NPCIL), BHAVINI, BARC, IGCAR.

Stock Price History

Walchandnagar has been a premium company in critical area manufacturing for aerospace & nuclear sectors. The company has gone through a very tough time but is now looking at a full swing turnaround, backed my massive sectoral tailwinds.

What do I like?

Company founded by a freedom fighter. Has tremendous strength the aerospace, defence, missile, and nuclear sectors.

These are very high-tech areas were only specialised players with the manufacturing capabilities, technical know-how, and historical quality delivery strength, can survive.

It is not easy for a new company to setup & establish itself as a credible supplier of these components, that too for the government, ISRO, NPCIL, etc.

Our Government is pushing on every business area that Walchandnagar Ind is involved in. There is and will continue to be growing demand for products that they manufacture.

Company is undergoing debt restructuring. In the process, they have raised preferential from a few astute & marquee investors – 233CR

Funds to be used for

Q3FY24 Results – poor, and expected. There was a strike which caused some loss, and they are still in the turnaround process.

Management is bullish, confident, and hungry to turnaround the entire business.

“This is truly an opportunity for Walchandnagar to rebuild its brand & legacy, to what it was two decades ago. Next ten years will define Walchandnagar, the engineering & aerospace, defence business, as we stand for it. I think we are very ambitions, very hungry, as a management team. This inflow of capital, and faith, that people have put in us, needs to be repaid in the next 5-10 years. We are very bullish about all that we do, and we are very hungry, that’s they key.” ~ Chirag Doshi, MD

Yesterday’s Press Release

My View

The worst is behind them.

I see honesty, patriotism, and hunger, in Chirag Doshi. These 3 values, when mixed with nation building initiatives by the government, and when the business has an edge due to the highly specialised & technical nature of the product mix (barrier to entry), the resulting recipe is one for imminent success.

Invested, position built slowly across the last several months.

*Disclaimer: I invest on management depth, market leadership, sector growth & demand. My holding periods are long, and I’m alright with drawdowns, as long as corporate & business hygiene is intact. NOT an expert, just a dreamer

My 2 cents –

Every time a Ruchir sharma equivalent tells you something , pls take a step back and ask whether he has an incentive to tell you what he is telling you . And then look at data yourself before coming to judgement.

How on earth China’s share of global GDP decline compared to US when former is growing at least 200 basis points higher , including in 2023??!!

And we all know that in last 12 months, US growth is funded with extreme fiscal expansion that even led rating agencies to react. Do we think that US has infinite fiscal room to keep pumping money ??

Rookie investor here. What I don’t understand is in the quarter of September company had PAT for insurance business. But there are multiple places in the earnings call(September) and ppt where we discuss insurance business to break even by 2027. What am I missing. Isn’t it already profitable ?

I exited this stock after finding that the no competence contract is no longer valid and also that greenply is doing capex and is also selling at 2-3% discount to gain market share, I feel there is no MOAT and I am bullish on the housing and MDF sector but then I think it could be a commodity with no real pricing power.