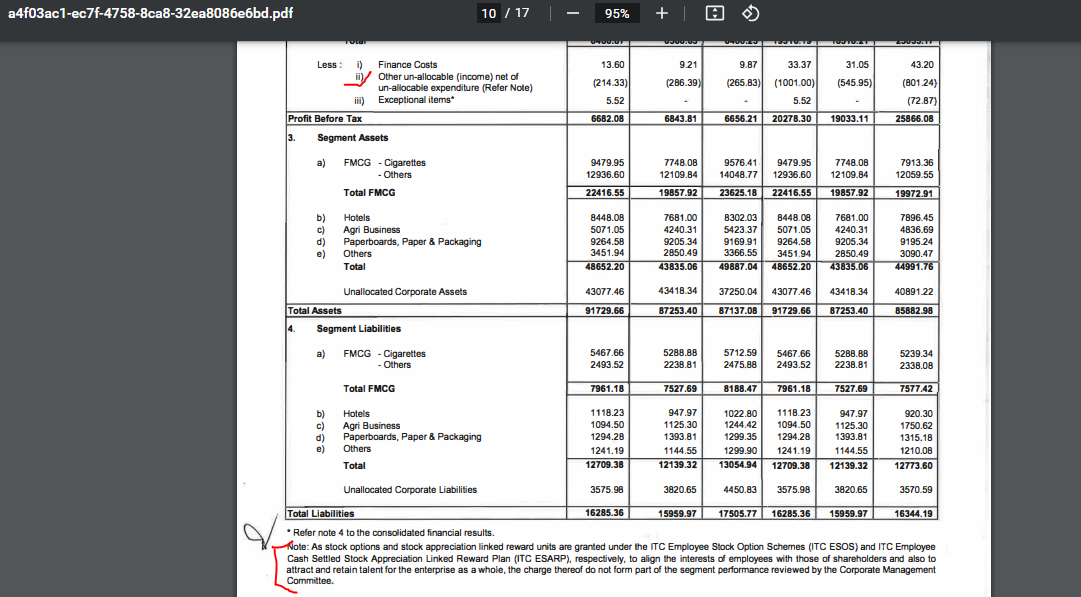

“Other un-allocable (income)- net of un-allocable expenditure” – snap you have posted you will get details about the Un-Allocable profit item in earning release file page number 6 footnote. I have captured the same line item in below snap at consolidated level and check the note , its saying about ITC ESOP charge. But there is more to it . Details you will get at ITC latest annual report page number 201 . Its more sort of Interest company earn for loan and deposits , profit loss on Investment – Finance Cost it pays out – Unallocated Corporate charge. As its segment reporting so corporate level income and expense which can’t put under segment shown in this fashion.