Recently visited the Hyderabad airport encalm lounge. Still had waiting of 10 mins around evening times. There is a bigger lounge going to open in the expanded terminal as well. So far do not see any effect of cards reducing lounge visits.

Posts in category Value Pickr

Tips Industries Limited – Ready to RACE ahead! (29-01-2024)

Saw Today’s Volume??? Big Boys are are entering the game ![]()

Endurance Technologies – Quality focussed Auto component manufacturer (29-01-2024)

Endurance – Corporate Governance example

CSL Finance Limited – Transition To NBFC (29-01-2024)

CSL finance has recorded a 42% growth in net profit to reach Rs 16.8Cr in the 3rd quarter. Company has a mcap of close to 1000cr and available at roughly twice the BV. Leverage ratio is quite low at 1.09x. Number of branches was at 29 as of Q2, company is targetting to reach a branch count of 50-60 by end of Fy25. Q3 GNPA at 0.40% and NNPA at 0.24%.

Disc: Invested.

csl.pdf (3.1 MB)

Ntpc (29-01-2024)

If ROEs are still capped, whats causing NTPC to quote at P/B of 2 now?? Is it the new CERC Tariff Regulations for 2025-29 anticipated to be more beneficial to power producers?

NCC: Extremely undervalued (29-01-2024)

Great earning acceleration lie ahead for the next 2-3 yrs

Basis management commentary and guidance on earnings ppt, Expect PAT to double from 650cr currently to ~1300cr in Fy25 and to cross 1650cr in Fy26 which for the CMP (Rs. 212) implies a PE multiple of 10 times on 1 year out earnings and a multiple of 8 times on 2 year out earnings.

For NCC, the PE multiple ascribed at cycle peaks crosses well over 22 times. Therefore, the stock has the potential to double in a couple of years at which point it would still trade at a very reasonable multiple of 16 times.

NCC: Extremely undervalued (29-01-2024)

Well, stock price and P/E are two different things. A stock can give multi-bagger returns at the same P/E if earning keeps growing. So high order book and better offtake will definitely ensure earning growth and hence appreciation in stock price. But if that will lead to P/E re-reating is doubtful.

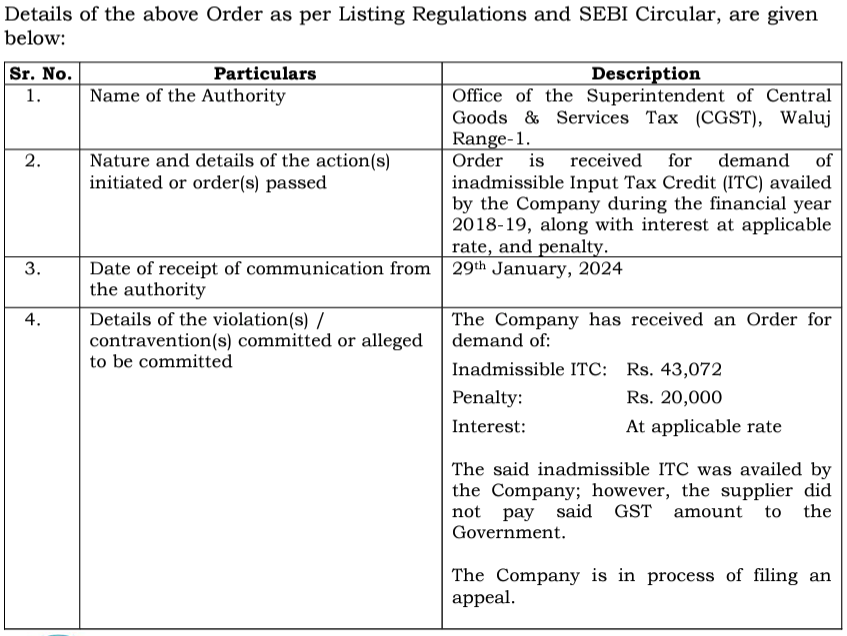

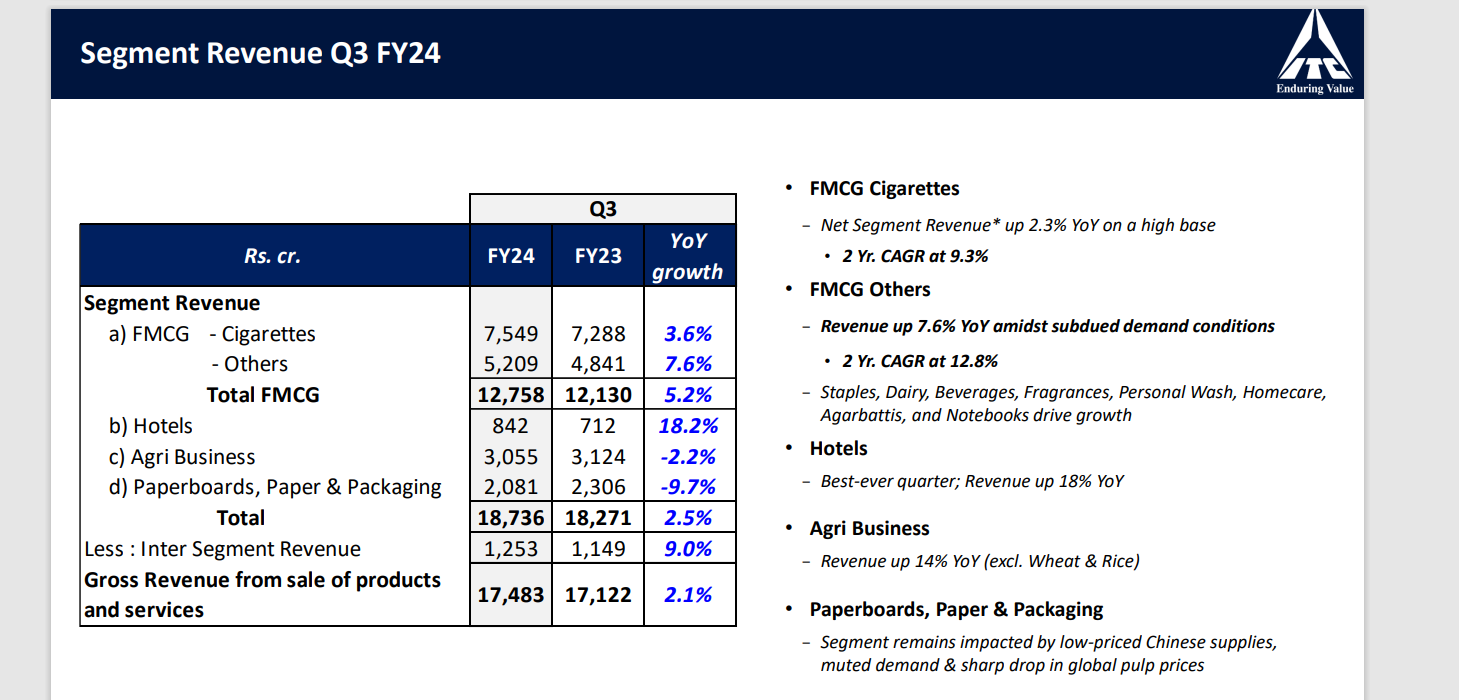

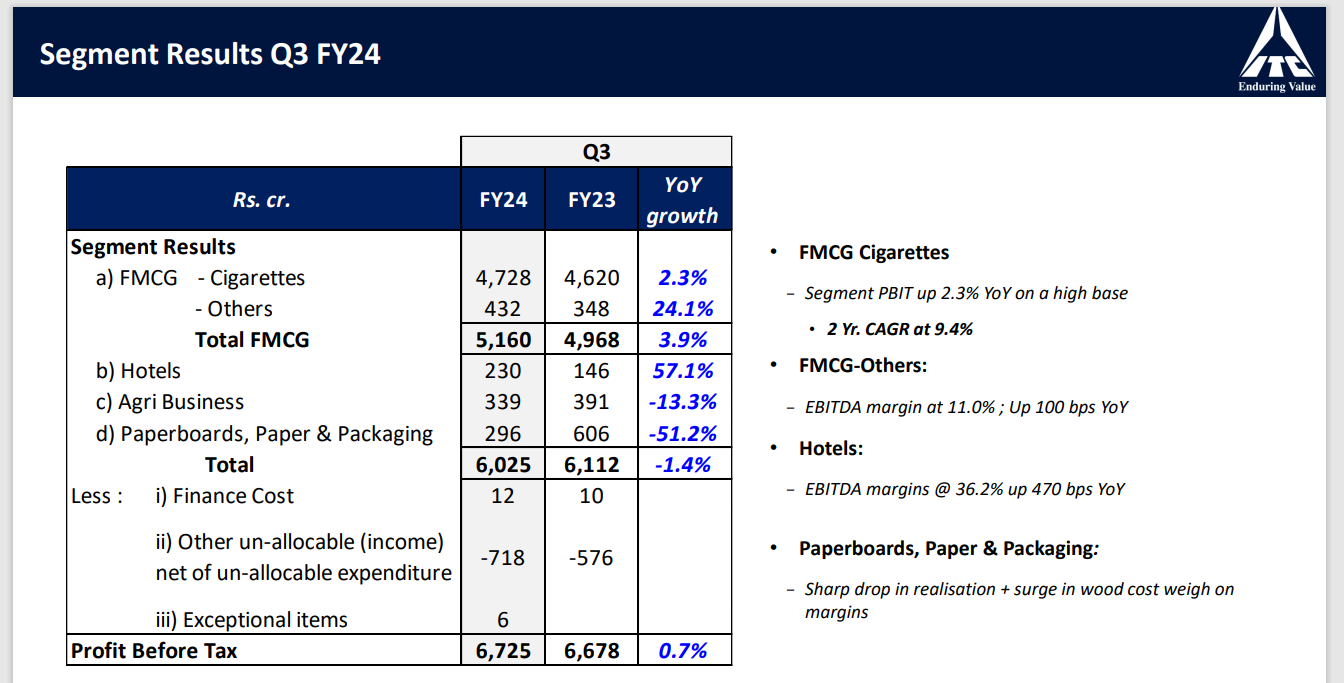

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (29-01-2024)

Hi,

Q3 results are out. Dividend 6.25 per share.

Results are exceptional for hotel business.

Results are good for FMCG others.

Results are ok for Cigarettes business.

Results are not good for Agri and Paper/Boards/Packaging business. However, this was expected considering the current environment.

Revenue Part:

Profits part:

Anyone, please explain what is this “Other un-allocable (income)- net of un-allocable expenditure” figure which is 718 core? Last year Q3 it was 576 crore.

Link for Presentation and results:

ca06d49c-f2bb-448d-a291-1e352bf932f3.pdf (bseindia.com)

Disclaimer: Views may be biased as I am invested in ITC.

Thanks,

Deb

Companies with 20%+ growth guidance for next few years (29-01-2024)

Zen tech has posted great results this quarter and yoy basis, further they have given 50% CAGR for next 4 yrs. Here’s concall link Sign in to your account

Elecon Engineering Limited (29-01-2024)

Thanks.

Elecon is a gem ![]()