it will become MRF of Pharma sector

Posts in category Value Pickr

PayTM (One 97 Communications Ltd) (27-01-2024)

Often, what a company doesn’t do tells a lot about it than what it says it does. So here are a few such things from the PayTM concall:

- We do not offer loans for merchants who have not been on our platform using devices consistently at least for a period of six months.

- We don’t intend to have a balance sheet. We are a technology company… we would love to work with the lenders and the wisdom that they have of doing credit over so many years…if they feel comfortable doing more, we would do more. If they feel comfortable to do less, we will do less.

- Why not rope in a different set of partners for postpaid who are willing to take higher risk? Answer: I don’t think as a strategy, we want to arbitrage and move to a partner who could technically say, “Hey, I’m happy to take this risk and let’s do business with – you can do business with me.” Our belief here is that we would love to build a business which on an overall basis is aligned to the way the regulatory thinking and the lenders are thinking. So, if there is a concern either regulatory or otherwise, we would like to play with that and make sure that unless and until the overall macro environment and regulatory environment is positive, we are not necessarily going ahead and building this business at a scale that we were building earlier.

- Don’t want to give PAT guidance though we expect to be PAT positive in near future.

- Will have only a moderate expansion of the sales force going ahead… we don’t necessarily need to add more people to grow.

- We can move a customer from one lending partner to another. There is no contractual restriction, but we do not do that unless the other lender is okay. We do not necessarily play on contracts; it is in the spirit of partnership.

I must say I agree with all of the above as a sensible business strategy.

Finally, a key point that is often missed (or underrated), which I have written above earlier also: Why anyone will take loan through Paytm app when they already have pre-approved lines of credit from their banks?

People are not necessarily aware or that much used to using their bank’s platform or lending partner platform that actively versus how they’re used to using Paytm platform. The accessibility of the app makes all the difference, our product efficiency is completely digital and very instant. What we are changing is availability. 10 crore people are able to see the icon to get credit.

(Disc.: Holding)

Amara Raja Energy & Mobility Limited: Powering Ahead (27-01-2024)

Gautam Ji, What conclusion we should draw from this. (Please accept my sincere apology, if my question is too silly)

Laurus Labs – Can Business Transform to Next Level? (27-01-2024)

Laurus signs pact to set up a joint venture with Slovenia’s Krka pharmaceutical.

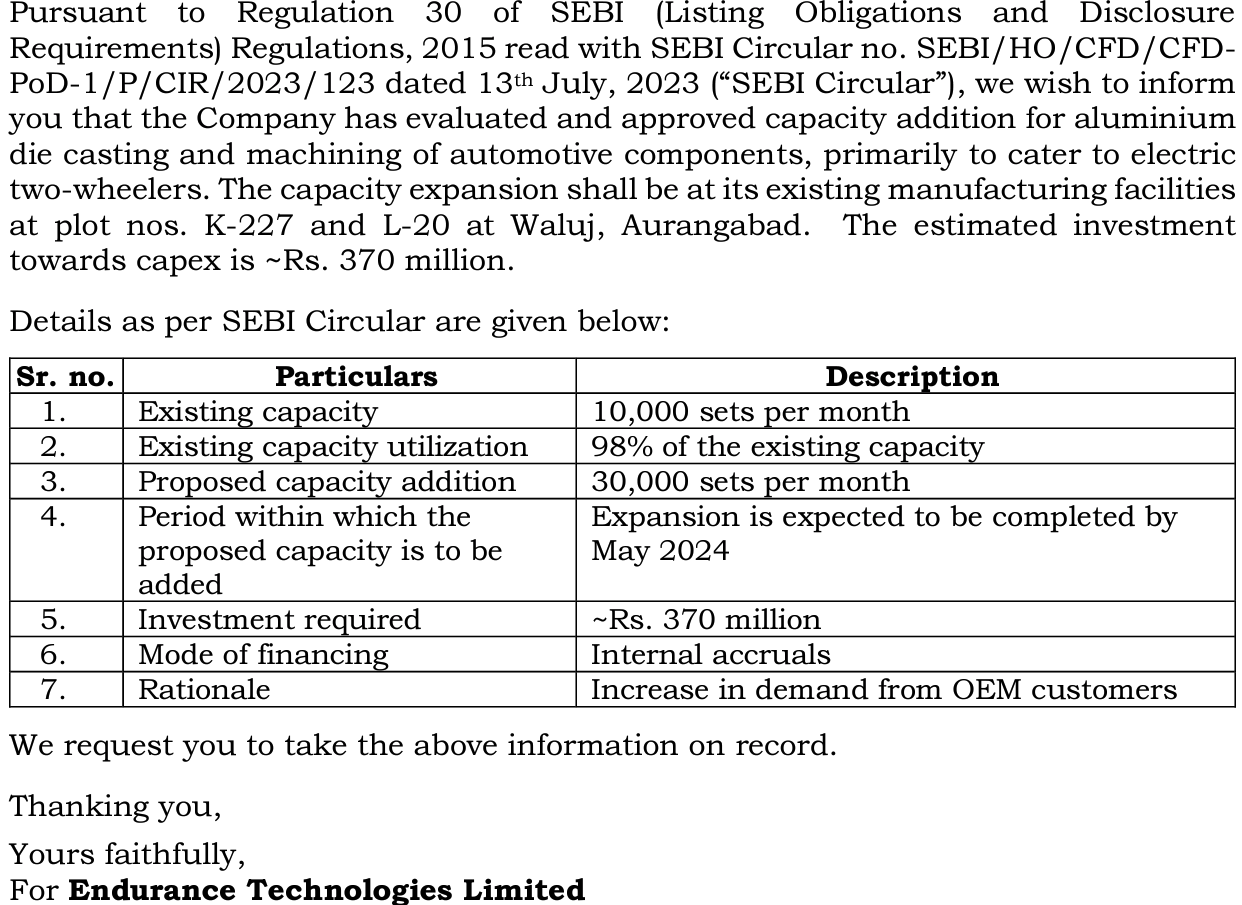

Endurance Technologies – Quality focussed Auto component manufacturer (27-01-2024)

Capex to cater 2W EVs

Est Capex : 370million

Almost 100% capacity utilisation of existing capacity

Internal Accruals

Zomato – Should you order? (27-01-2024)

Hi @siddybee . Thanks for the write up on the blog. I am trying to understand the impact of the payment aggregator license that Zomato has now.

I guess it will help zomato to optimize the costs, there by increasing the profit to an extent. It may also be able to onboard new customers who will use its payment aggregation interface.

But any idea on the magnitude of impact we may be able to see?

(Disc. Not invested)

Migrating out of Zerodha (27-01-2024)

Ya because this is integrity issue and if it is the case then I or we who have a zerodha account needs to rethink on continuing

Migrating out of Zerodha (27-01-2024)

@Rejulal Please Elaborate this & mentioned in detail when you have faced such issue

Investment strategy review (Long term) (27-01-2024)

Hi Tushar, Welcome to the Forum!!

First of all, I would like to mention do not run to invest in everything/every investment product eventually you will end up creating a mess & it will become very difficult to track so many things with very less allocation. According to me start from 1 thing keep minimal so that so that you have proper knowledge of that one product, and you will also have the real taste of that product also with good allocation which will keep you motivated to read and study about that 1 product regularly, give that 1 selection some time (Don’t be in a hurry which can be seen like you want to invest asap , You are thinking money is getting inflated in Saving bank.)

Secondly you are trying to take best of everywhere i.e. best return with safe products which is not practically possible. You will have to choose 1 return or Safety. (Not a recommendation because I don’t know about your background and financial position but at such a young age one should choose Calculated risk)

Every product has a characteristic & nature which should be kept in mind before deciding it is suitable for you and if that aligns with your requirements, Expectation You should jump into the product only when you have knowledge i personally know a lot of people who started with a lot of enthusiasm but have lost money in market.

Lastly on this amount expectation you should calculate the return on total portfolio not like the highest %. According to what you have mentioned 55% in safe instrument & 45% in MF +Equity you will be making about 9-10%

Disclaimer: I am not SEBI registered & have a limited knowledge about your background & income. All the above mentioned is based on my personal understanding, please think twice before taking any financial decision at the end your hard-earned money is at stake. My views may change with time.

Can anyone answer my question about bulk deals (27-01-2024)

In many instances they will be representing different end clients on a synthetic product (ie: equity swaps) – in this case we won’t see the end investors’ name.

For example a broker / banker may be squaring off a swap for an institutional investor in the US , but at the same time may be offering a swap for an investor in the UK.