(post deleted by author)

Posts in category Value Pickr

Shreeji Translogistics (26-01-2024)

Thanks pls share your opinion on the promoter. Other income is categorized under ” other income normal ” and not under ” other income exceptional”. Thanks

Shreeji Translogistics (26-01-2024)

other income, buy selling trucks it owns what i feel

Genus Power – Smart Metering (26-01-2024)

The new FII entry 15% u see is from GIC…

Companies with 20%+ growth guidance for next few years (26-01-2024)

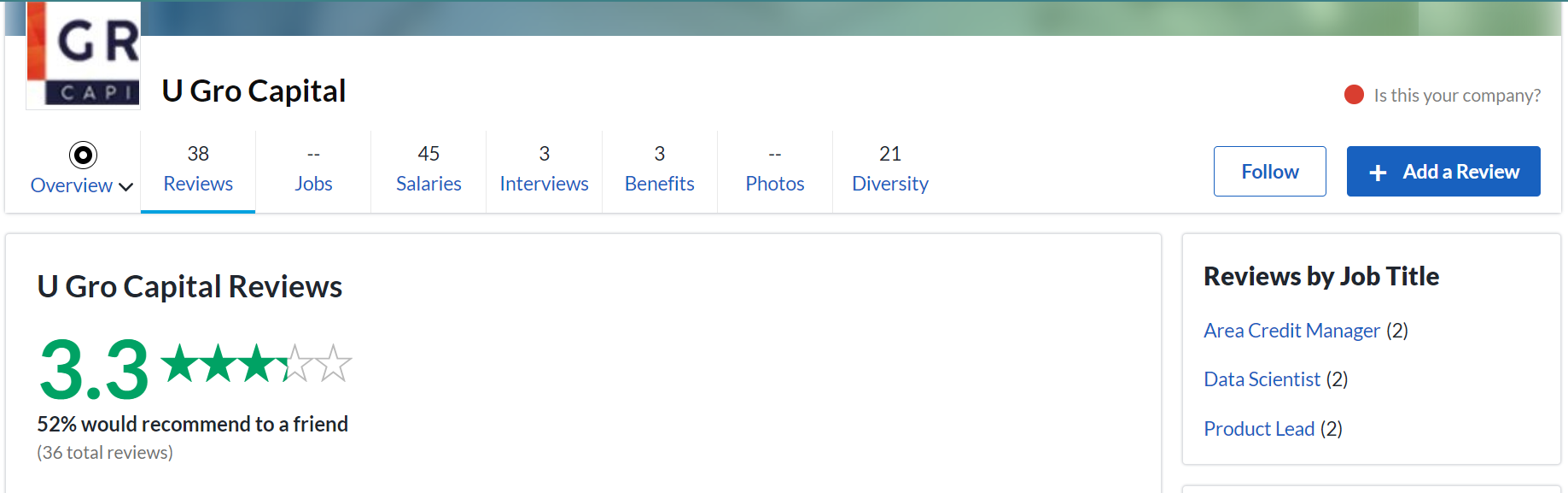

Ugro Capital – Growth projects are good. However ROE Metrics look very weak:

Not very healthy reviews from employees on Glass door either :

Investment strategy review (Long term) (26-01-2024)

Hi, thanks for the reply. I’m still learning so please feel free to let me know if anything I said isn’t correct or there’s a better way. I’ll try to make an explanation to everything on why I’m doing it.

P.S. I have made some investments just for ‘learning’ purposes in the last week. 5.3k of stocks in total to be precise. Mostly the bullish/popular ones like IREDA, IRFC, HDFC. I just invested as by doing so I was actively thinking about it instead of just say learning which in turn motivated me to actually become worried and actually learn more on weekends or stay up to date with the news. That’s the only ‘real’ experience I have at the time of writing this.

The percentage allocation is not something fixed. I will probably make some changes to that when I start investing monthly like I mentioned in the post (probably in a month or so will learn till then). It’s just what I personally came up with.

a. The reason for safe investments, as of now, is to minimise risk. Again, from what I have found out so far the high risk mutual funds I mentioned (like nippon) seems safe in long term (5+ years and I’m aiming 10+) with amazing returns but initially I would like to put my money where there is least fluctuation and returns are consistent. Maybe for the first year of my investment journey. I think it’s mostly because I’m a beginner and will probably change the approach soon as I learn more about how market works.

b. By safe I again mean with the least variation. For ex I mentioned Invesco india arbitrage fund direct growth as an example as you can see the growth for this one is almost linear since 2013 so I consider it a ‘safe’ investment.

For 3k I just added it for reference purpose. Yes, I don’t think it will add any value to say my PF. Again, might be out of context question but by PF you mean something that ‘I’ am investing. Right? I do have an EPF account but my current company doesn’t support and PF scheme. I am assuming you’re referencing the long term (say retirement) investments ‘I am’ making as PF.

For allocation strategy I think I’m a mix of both. I do have a number in mind. Say rough 1-2cr in investment before turning 30 (8-9 years for me) and push it to 5+cr before 35. Again, these numbers I’m estimating with only some sip calculation I did in the last 2 weeks. It seems pretty much doable as I will increase the SIPs a lot in future as I don’t like spending a lot of money. Probably 60-70% will stay in my savings account anyways so will be better to invest it. But the investment should do at least 12% CAGR for 10 or so years as I’ll keep on increasing the SIP as I increase my source of income.

Some are suggesting me to start small. Say, invest 10k pm in total in mutual funds (divide in 4 types of fund 2 small cap, 1 index, 1 mid/large cap) and say 2k (separate from the 10k) in stocks for learning the market.

The main thing that is motivating me for investing in general is compounding. The early I start the better it is. Hence why even the 10k that I mentioned in the last paragraph will be a great investment in long term. Even a year will make a lot of difference in long term because of compounding. Hence, my main focus is to start as early as possible with the highest returns as possible.

Again, I’m still pretty new so some of this might be incorrect so feel free to point that out.

Thanks!

Infinium Pharmachem Ltd – new growth story in pharma space? (26-01-2024)

Incorporated in 2003, Infinium Pharmachem Limited manufactures & supplies Iodine Derivatives, APIs, and Iodination reaction-based bulk drugs.

KEY POINTS

Business Area: Infinium is an integrated Pharma and Healthcare segment company with niche products. Co. manufactures and supplies various pharma-related chemicals, bulk drugs, pharma intermediates, etc.

Wide range of Product [1] Company currently provides the widest range of Iodine derivatives in the market, with 250+ intermediates and 15+ APIs

Manufacturing Facilities [3] The Company has its manufacturing plant at GIDC Sojitra, Dist. Anand – 387240, Gujarat, spread across 6204.53 sq. Mtrs. of land.

IPO Details Company intends to raise 25.3 Crs through the IPO which will be utilized for:

- To meet Marketing and Other Expenses

- Expansion of the Existing facility

- Repayment of Borrowings

- To meet its working capital requirement.

Micro-cap company with reasonable PE (34.96) than peers. It has recently IPO’d and untested. Looking to enter at right price.

Zomato – Should you order? (26-01-2024)

Zomato is trading a P/E of 142 times with a market capitalization of INR 1.18 LAKH CRORE. Margins are hard to grow in this line of business with intense competition and pricing pressure, and the upside at this price point looks very limited.

I wrote a DETAILED article covering Zomato’s B-model + whether the stock offers a good investment opportunity – Zomato : a long term bet? – by Siddharth Bothra

Here’s my take on the Q2FY24 results:

Pros

- Zomato started charging platform fees (around INR 3-4 per order) in line with competition. Management expects platform fees to stay for the foreseeable future. Almost 100% of orders have platform fees now.

- Ad revenue increased on the back of increase in ad placed on Zomato. Ad revenue + platform fees helped contribution margin by 20 bps in Q2FY24

- Blinkit became contribution margin positive in Q2FY24. Could achieve EBITDA breakeven by Q1FY25. Blinkit GOV could be > than Food delivery business in the future. 480 dark stores expected by the end of FY24. Started selling iPhones and other electronics which could drive GOV up. (iPhones are excluded from GoV however)

- Expecting 25-30% growth in Food delivery GOV for Q3

- Key metrics: 18.4Mn MTUs, 3.8Mn Gold members, Average monthly ordering frequency up 3%, GOV up 47% [for Q2FY24]

- Sitting on a cash balance of INR 11,761 CRORE at the end of Q2

Cons

- Pace of Gold membership increase could slow down in future. Gold orders are lower contribution margin than non-Gold orders. Gold subscription only covers a part of the incremental costs incurred for privilege service provided to Gold members. Will continue to be a drag on margins.

- ESOP costs increased, might end with 450 crore of ESOP Expense for FY24 [I don’t believe in the concept of Adjusted EBITDA

]

] - HyperPure didn’t see any positive movement in EBITDA. No commentary from the management on this line of business in general.

- Marketing costs were up 13-14% QoQ. Salary costs were up 20% QoQ due to salary increments generally carried out in Q2.

Zomato is doing a lot of things right, looks like a good business. But – margin expansion is difficult, without which the stock would continue to look expensive.

Disclosure: Not invested. Waiting for atleast a 30% correction from current levels to enter the stock.

IPO Review – Discussion until listing (26-01-2024)

@Yogesh_s what are your thoughts on Capacite infra now? Do you see value?

CMS Info Systems Ltd (26-01-2024)

See there may be two possible reasons for this : 1) Promoter PE Firm has been selling its stake time and again as they will be completely exiting due to fulfillment of their investment objective. This has affected investor sentiment and increased supply time & again. 2) Due to digital push of the government, many investors are not keen.

Having said that, I think this is a very good company which will become a major banking technology services provider. The first concern is short term and second concern will have not impact due to huge indian cash market and company increasing focus on tech solutions to banks.

Dis : Made good returns and still invested.