Om ! …nice info.

I wish i could find comparison of these 3. comparing interest margin,asset quality, porfolio, growth, OFS,Dividend,NPA,valuation,customer composition…etc.

Probably we might be able to find best amongst better ?

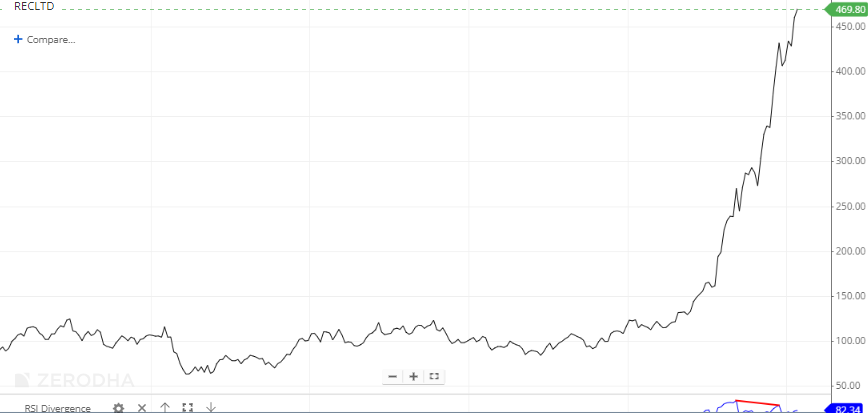

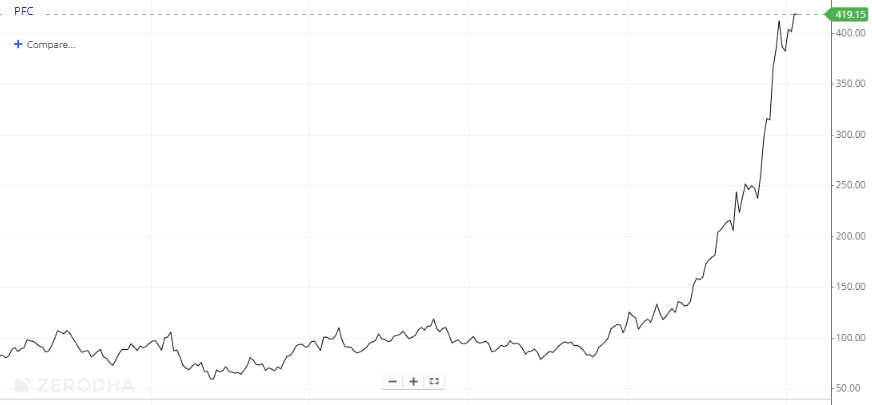

I can only compare 5 year REC/PFC chart…it looks identicle.

D-Invested in IREDA. ![]()