Posts in category Value Pickr

Vedant Fashions (Manyavar) – Niche Branded Retail (23-01-2024)

Problem with 5 year CAGR is the covid impact from Apr20 till atleast CY21 season and hence I would not like to look at that. But yes what you are saying is correct qualitatively because people started touting it as the next Titan! And hence it went to a PE of 90 with not more than a 15% sales growth irrespective of the Covid-19 impact.

If at all, this should be more like a 40-45 PE stock at max considering it has good return ratios (GM, OCF to EBITDA, ROE) and a possible sales growth of 20% in the future.

My personal view. Invested in the stock and biased.

Vedant Fashions (Manyavar) – Niche Branded Retail (23-01-2024)

Thanks of putting in simple numbers. It is strange that we as investors looks at such growth figures only after stock falls and when it keep rising, the same business’s numbers tell a different story…

Praj Industries (23-01-2024)

NetWeb Technologies (Supercomputing?) (23-01-2024)

Quarterly results for the company are out: 44% YoY growth in revenue and 20% YoY growth in PAT. Seems decent but not great as the company is trading at very high valuations. I am expecting a little correction basis the results. One interesting update provided by the Management on the orderbook is related to ISRO order amounting Rs 1477m i.e. equivalent to Q223 revenue. Hoping for Management to provide some additional details on the same in tomorrow’s call.

Disc. Invested from IPO levels

UFO Moviez – Views please (23-01-2024)

Taking a short cut here with this genuine question as I haven’t looked at the company in recent times.

What has changed form UFO of 2016-2023 to UFO of today?

Has the business model changed?

If they weren’t able to grow then, then what has changed for them to be able to grow now?

Thanks.

Axis bank – Turnaround imminent (23-01-2024)

Axis Bank Q3 Net Profit At ₹6,071 Cr, Deposit Growth Better Than Peers | CNBC TV18

Business Momentum

Deposit Growth : 18.5% YoY 5.2% Sequentially

Loan Growth : 22.3% YoY 3.9% Sequentially – They have gained Market share

More than 5% Deposit Growth is the strongest in the Banking Sector.

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (23-01-2024)

Agree, DBOL concall was very informative about the company and the industry.

Few key points:

-

Cost reduction : Increase in recovery rate (by 0.9 to 1%) will more than compensate increase in cost due to SAP price increase. As 0.1% recovery increase translates into cost reduction by Rs 0.35 per kg of sugar so due to 1% increase in recovery cost will come down by Rs. 3 and cane cost will go up by Rs. 2 so effectively margin will increase by Rs. 1 per kg. So on 4.5 lac ton sugar it should be Rs. 45 crs.

-

Revenue growth : Sugar prices will not jump but will increase to the extent of SAP increase ( which implies by Rs. 2 /kg) – even if Re 1 increase in price of sugar will translate in Rs. 45 cr for the year.

-

Cane crushed for full season will be 5 to 7 % higher than last year

So all in all, DBOL profits should be at least Rs. 100 cr higher than last year – on account of recovery improvement, cane volume increase and sugar price increase. Even if sugar prices dont increase the increase in profits will be Rs. 50 crores. Post depreciation increase/ other costs annual profit should be 150crs – EPS of 23 which is similar to Dhampur sugar). At a PE multiple of 10, fair value should be Rs. 230.

Further, if they convert the ethanol plant to dual fuel and maize is available at reasonable price then ethanol volumes and profits will be higher.

Please comment – agree/ disagree…

How to register with SEBI as a Research Analyst? (23-01-2024)

You can reach me on 98507 28257

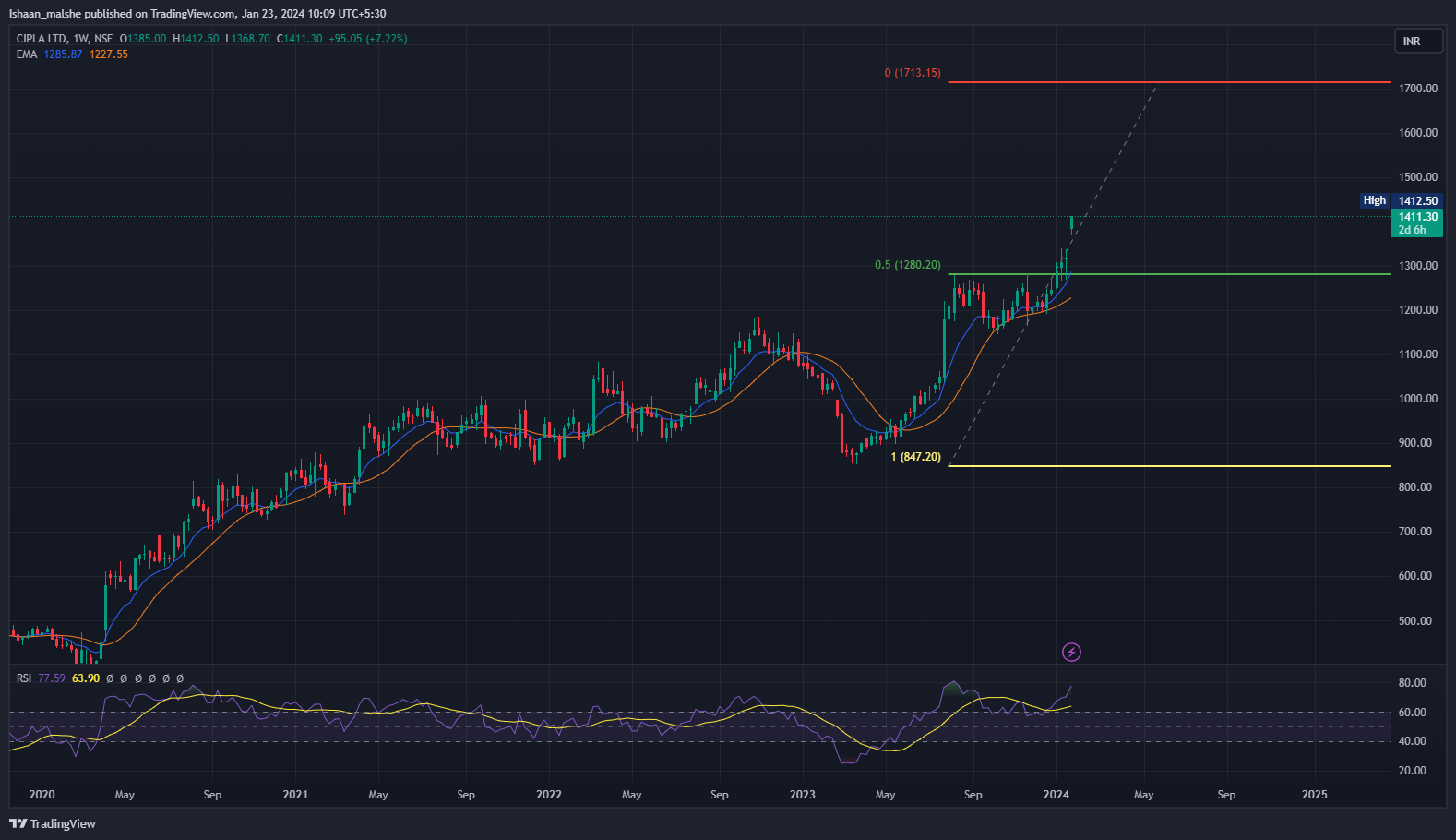

52 week highs and all time highs strategy (23-01-2024)

Cipla has broken out of its Flag and Pole pattern and also its 52 weeks high. It has consolidated enough before the breakout, hence the trend is very strong. The targets are close to 1650-1700.