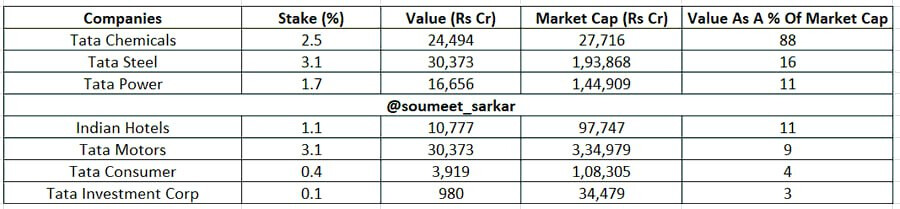

Tata power can benefit with Tata Sons IPO

Tata power can benefit with Tata Sons IPO

Hi @Cshar

How are you handling the recent downturn in market? There seems to be earning slowdown from market favorite sectors. Are you moving to cash or moving into defensives?

Market experts are predicting corrections to continue till US elections and suggesting to move into defensive sectors like Pharma/IT/Consumption etc. What is your thought on this?

Thanks

Hi @Cshar

How are you handling the recent downturn in market? There seems to be earning slowdown from market favorite sectors. Are you moving to cash or moving into defensives?

Market experts are predicting corrections to continue till US elections and suggesting to move into defensive sectors like Pharma/IT/Consumption etc. What is your thought on this?

Thanks

Dilution due to fund raise

Dilution due to fund raise

That’s a detailed and impressive analysis. I also firmly believe that the rate cuts will benefit Affle.

You nailed it with the threats. In the US it’s 5 more states now that have privacy laws.

R&D is a big one to stay ahead of changing technology, new standards, and regulation. There is no strong moat other than this.

That’s a detailed and impressive analysis. I also firmly believe that the rate cuts will benefit Affle.

You nailed it with the threats. In the US it’s 5 more states now that have privacy laws.

R&D is a big one to stay ahead of changing technology, new standards, and regulation. There is no strong moat other than this.

Did anyone attend the results concall today. If yes, any takeaways?

Did anyone attend the results concall today. If yes, any takeaways?

Company Overview:

Northern Arc Capital Limited is a diversified financial services company focused on providing credit solutions to underserved households and businesses in India.

Established 15 years ago, the company aims to facilitate the flow of credit from capital providers to users in a reliable and responsible manner.

Management Insights

Business Model:

Financial Performance (Q1FY25):

Risk Management:

Market Dynamics:

Competitive Advantages:

Future Outlook:

Headwinds and Challenges:

Strategic Initiatives:

From the latest con-call

IPO (Price action)

Issue price – 263

Open price – 350

Current price – 251

Disclaimer- Invested and biased , will be adding more at the current levels.

Not a buy/sell recommendation.