Minda Corp sells 15.7% stake in pricol at 343.60 shares (1.91 crore shares)

News source – internet

Invested

Posts in category Value Pickr

Pricol limited – OEM automotive (17-01-2024)

Federal Bank – A Turnaround banking Story? (17-01-2024)

Federal Bank –

Q3 FY 24 Updates –

Deposits – 2.39 lakh cr, up 19 pc

Advances – 1.99 lakh cr, up 18 pc

Gross NPAs – 2.29 vs 2.43 pc

Net NPAs – 0.64 vs 0.73 pc

PCR @ 71 vs 69 pc

Total branches @ 1418, added 65 branches in FY 24

Cost/Income @ 51.9 vs 48.9

Yield on advances @ 9.37 vs 8.78 pc

Cost of funds @ 5.81 vs 4.71 pc

NIMs @ 3.19 vs 3.55 pc

RoA @ 1.39 vs 1.33 pc

RoE @ 14.80 vs 15.91 pc

Profit and Loss parameters ( standalone ) –

NII – 2123 vs 1957 cr, up 9 pc

Fee Income – 642 vs 543 cr, up 18 pc

Operating profit – 1437 vs 1274 pc, up 13 pc

Provisions – 431 vs 471 cr

Net Profit – 1007 vs 804 cr, up 25 pc

Segment wise growth in advances –

Retail – 65k cr, up 20 pc

Agri – 25.1 k cr, up 27 pc

Business banking – 15.97 k cr, up 18 pc

CV / CE – 2.7 k cr, up 66 pc

MFI – 2.3 k cr, up 160 pc

Commercial banking – 20.7 k cr, up 26 pc

Corporate banking – 71.9 k cr, up 14 pc

High margin products for the bank include – CV/CE, Personal, Credit Cards, Micro Fin and MSME loans – this cohort now forms 24 pc of Bank’s book vs 21 pc LY

Slippages for Q3 @ 480 cr ( within limits )

CASA + Deposits < 2 cr @ 81 pc of total deposits vs 88 pc LY

One of the large accounts worth 70 cr slipped in Q3 due factory fire at client’s factory. Likely to become standard in Q4

Bank is carrying 20 pc provisions on the restructured book. Current size of restructured book at 2200 cr

Aim to take the unsecured book to 10 pc of the total book from aprox 5 pc at present

Bank holding onto its advances growth guidance of 18-19 pc for FY 24. Aim to maintain the deposits growth rates in a similar band

Capital market investments / SIPs etc are also increasingly competing with banks for saving deposits. People are becoming more tech savvy and are managing their saving accounts more actively. Term deposits are relatively insulated

41 branches out of 75 opened LY have turned positive. Bank is very particular about location while opening a new branch

Disc: holding, biased, not SEBI registered

Ranvir’s Portfolio (17-01-2024)

Federal Bank –

Q3 FY 24 Updates –

Deposits – 2.39 lakh cr, up 19 pc

Advances – 1.99 lakh cr, up 18 pc

Gross NPAs – 2.29 vs 2.43 pc

Net NPAs – 0.64 vs 0.73 pc

PCR @ 71 vs 69 pc

Total branches @ 1418, added 65 branches in FY 24

Cost/Income @ 51.9 vs 48.9

Yield on advances @ 9.37 vs 8.78 pc

Cost of funds @ 5.81 vs 4.71 pc

NIMs @ 3.19 vs 3.55 pc

RoA @ 1.39 vs 1.33 pc

RoE @ 14.80 vs 15.91 pc

Profit and Loss parameters ( standalone ) –

NII – 2123 vs 1957 cr, up 9 pc

Fee Income – 642 vs 543 cr, up 18 pc

Operating profit – 1437 vs 1274 pc, up 13 pc

Provisions – 431 vs 471 cr

Net Profit – 1007 vs 804 cr, up 25 pc

Segment wise growth in advances –

Retail – 65k cr, up 20 pc

Agri – 25.1 k cr, up 27 pc

Business banking – 15.97 k cr, up 18 pc

CV / CE – 2.7 k cr, up 66 pc

MFI – 2.3 k cr, up 160 pc

Commercial banking – 20.7 k cr, up 26 pc

Corporate banking – 71.9 k cr, up 14 pc

High margin products for the bank include – CV/CE, Personal, Credit Cards, Micro Fin and MSME loans – this cohort now forms 24 pc of Bank’s book vs 21 pc LY

Slippages for Q3 @ 480 cr ( within limits )

CASA + Deposits < 2 cr @ 81 pc of total deposits vs 88 pc LY

One of the large accounts worth 70 cr slipped in Q3 due factory fire at client’s factory. Likely to become standard in Q4

Bank is carrying 20 pc provisions on the restructured book. Current size of restructured book at 2200 cr

Aim to take the unsecured book to 10 pc of the total book from aprox 5 pc at present

Bank holding onto its advances growth guidance of 18-19 pc for FY 24. Aim to maintain the deposits growth rates in a similar band

Capital market investments / SIPs etc are also increasingly competing with banks for saving deposits. People are becoming more tech savvy and are managing their saving accounts more actively. Term deposits are relatively insulated

41 branches out of 75 opened LY have turned positive. Bank is very particular about location while opening a new branch

Disc: holding, biased, not SEBI registered

The harsh portfolio! (17-01-2024)

Namastey Harsh,

I am amazed how you analyze business:

== transparency of understanding business by valuating products,money and capacity.

Capacity expansion – Screener. I use some tool and charts based on data… …

Can u suggest me…how to understand money flow not charts…because charts can be manipulated…but healthy business…can,t be manipulated too fast…!

One example of yours understanding is…Equitas bank…Show pros and cons of UNITECH…?

Piramal Pharma Limited (17-01-2024)

If we keep aside the 1-off misallocation of NPAs in between the 2 entities during demerger, I would like to get inputs from you all on Piramal management along the lines of 1)capital allocation, 2)business decisions(product growth, new opportunities, scaling up) & 3)ethics. Would be great to hear from anyone who might have met the management

Why not leave it to the experts? (17-01-2024)

In a nutshell, I invest directly because I enjoy the process, feel like I’m gaining better knowledge about businesses, and stay informed about what’s happening in the business world. I have been investing since 2012, and here is my journey if you have more time to read ![]()

For the initial two years, I engaged in day trading whenever I had the time, whether resulting in profit or loss, but I used to enjoy it. I believed I had made some money, but when I carefully examined the numbers, I realized that all the profit was wiped out by brokerage charges. I only gained experience and realized that trading is not for me.

Subsequently, I have asked ICICIDirect to handle my account under the wealth management service. I invested around 2 lakhs, and they only invested in one stock without making any further moves for the next two years. Although the stock gained 40%, but it didn’t bring me satisfaction.

In 2015, I began investing in mutual funds for tax-saving purposes and simultaneously started investing in direct stocks (only in a few thousands since I’m not confident enough) by reading books and following some good blogs. Again, I was not satisfied with mutual funds, not because they weren’t making money (some of these funds are still holding, and XIRR is around 16%), but I stopped investing in mutual funds and returned to direct investing, this time with a long-term approach. I still hold some two stocks from 2017.

From 2017 to 2020, I exclusively invested in direct stocks, using all my money, including some funds from the mutual funds I sold and money drawn from PF (yes!). During the 2020 crash, my portfolio went down almost 40%, and I didn’t take any action with my portfolio, neither buying nor selling, until October 2020. From October 2020 onwards, I started buying again.

Fast forward to today, I have achieved around a 20% XIRR on the overall portfolio, with approximately 70% of my investments in direct stocks. However, after witnessing a 40% drawdown during COVID, I made a slight change. I began investing in mutual funds through the SIP route to take off some risk and leave it to fund managers. My mutual funds are also performing well, with an XIRR of around 18-20%.

In conclusion, investing in direct stocks gives me a kick and excitement ![]() Now I know where to spend all my free time, even when I retire from active life. I have sorted out my post-retirement activity, which involves reading and investing!

Now I know where to spend all my free time, even when I retire from active life. I have sorted out my post-retirement activity, which involves reading and investing!

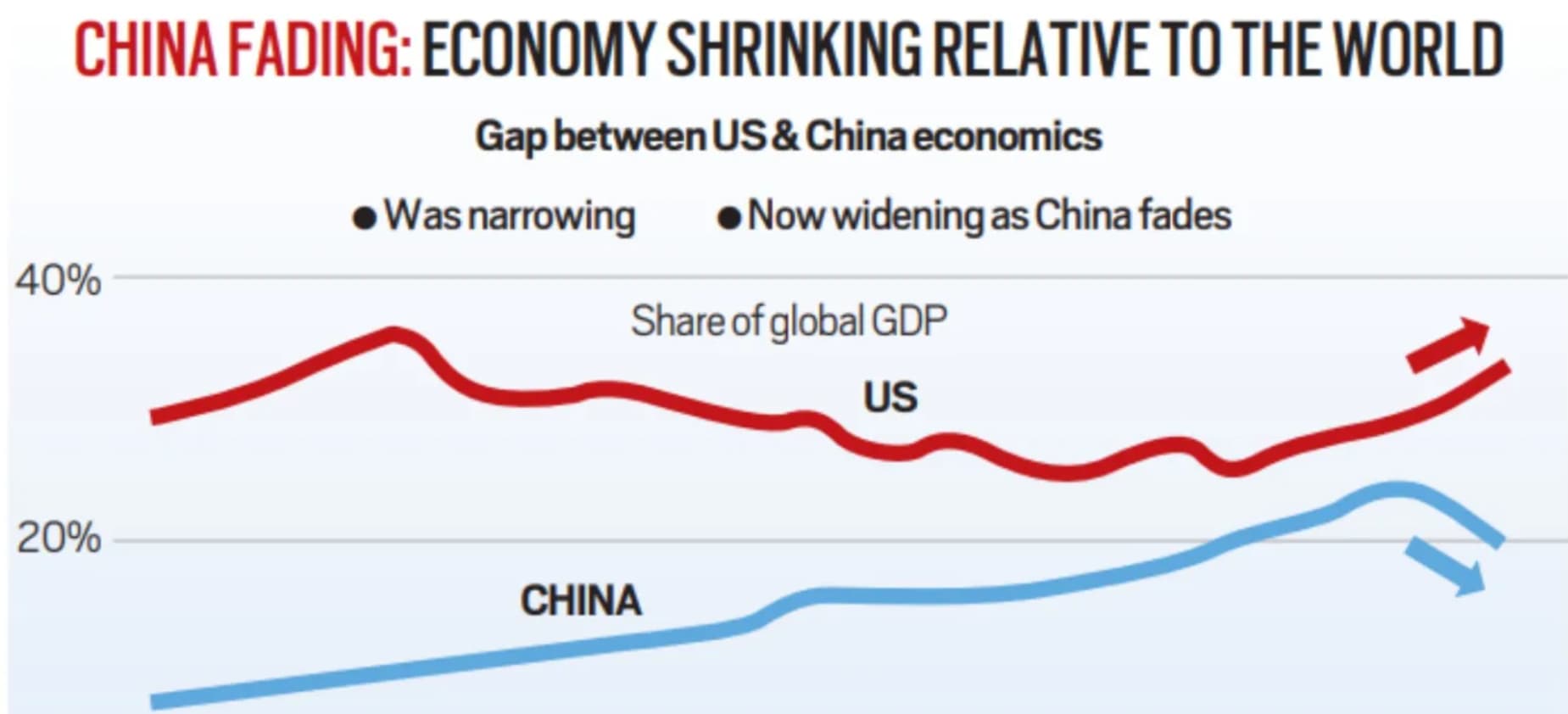

Is China investible? (17-01-2024)

China fading: Money is fleeing China. Global investors want to de-risk from China. There’s so much geopolitical tension. Some of the growth drivers aren’t there anymore. Their population is shrinking, which is not great for economic growth or dominance.

Source: Ruchir Sharma’s top 10 trends for 2024

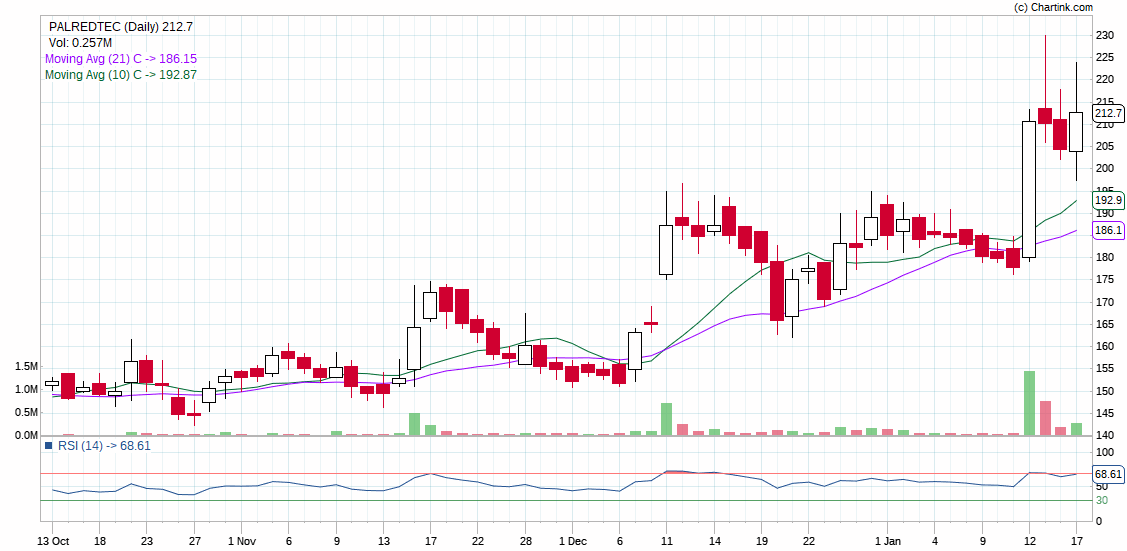

Palred technologies – www.latestone.com (17-01-2024)

what’s fishing ? recent 19% move and today opp to market movement?

Omkar’s Portfolio Analysis and Discussion (17-01-2024)

Pattern in my thinking – which I would like to probe/ introspect more

I have observed pattern in my thinking which I would like to introspect more and document

I have tendency to prefer “focused aggression” in manufacturing business but I prefer diversified models in the service sector.

In manufacturing –

I prefer Suprajit over minda

I prefer ajanta over laurus or alembic

I prefer Vinati over Navin Fluorine

I think ( i am not sure) prefer Cera over Astral

In services –

I prefer diversified financial business over only amc, only insurance or broking

I prefer HCL tech ( services + product + er&d) over tata elexi / kpit/ newgen

I prefer large hospitals ( apollo, narayana, kims, max) over kovai / KMS speciality

Omkar’s Portfolio Analysis and Discussion (17-01-2024)

Basket Approach in non-core holdings – Financials

I will continue with my plan with building basket approach in my non core holdings – financials ( 6-7% in each hdfc, kotak, icici, bajaj finserv) as stated earlier for following reasons

- The role of non – core holdings is to let me allow to hold my concentrated core positions as long as their terminal value or franchise value is intact

- I dont want to be too adventures in non-core holdings. Its job is to provide buffer and allow me to be aggressive in concentrated positions

- Basket approach enables to take large allocation in a diverse financial which has long runway of growth

- They also provide good exposure to amc, insurance and brokerage business from both the sides – agency and product

- In my judgement equal weighted basket of 6-7% in each – hdfc bank, kotak bank, icici bank and bajaj finserv provided similar risk reward over a long term to any other large cap lending or non lending financials with better diversification of revenue streams

- More importantly, it helps to stick with the plan on day like today.