Posts in category Value Pickr

City Union Bank (CUB) ~ Conservative Lending Franchise (21-10-2024)

Results seem decent to me – https://www.bseindia.com/xml-data/corpfiling/AttachLive/6c61defb-43e8-41d2-adad-73645ae139a5.pdf.

They have taken higher provisions (at least partly to boost their PCR, it seems like) which has impacted profitability. But other than the increasing cost of deposits (which every bank is struggling with), most of the other metrics seem quite fine. They have maintained NIMs, strong growth in fee income, good growth in advances, CASA hasn’t gone down (not much anyway), and an unexpected slight improvement to their cost-to-income ratio for some reason.

The stock’s not done much and it’s been on a downtrend of late. But I like these results. Not fantastic, but in the current environment, it seems quite good. Not sure if I am missing something. Any additional thoughts would be welcome!

Websol energy system ltd (21-10-2024)

Anti- Dumping Duty on Solar cells imported from China PR region based on the request of FS India Solar Ventures & Jupiter International Limited. The Commerce department initiated the investigation on 30-09-2024 and requests information and submission from interested parties to determine the existence of dumping on or before 30-10-2024.

If the investigation outcome is positive then it should benefit the Domestic manufacturers of Solar cell. Websol is a SEZ unit. so, It is technically not a domestic industry. However, they are eligible to sell in DCR market and ALMM for Cell is expected by April 2026. So, more good things are waiting for Indian Solar cell players.

But the issue with Solar Cell is it is highly complicated tech. It is difficult to master quickly. Scaling up will take a long time as Cell breakage is very high in addition to achieving desired efficiency. Websol is one of the oldest players in India mastered this technology early. Premier is also good to some extent. New players who are still in planning stage like Waaree, Vikram, etc., and all other Module only players would find it difficult to scale up the production with desired output.

So, achieving a handful of domestic cell production by April 2026 is a big question mark. We have to wait and see as how this industry will evolve in FY26.

On the other hand, Any positive outcome will impact the margins of Module only players and EPC companies as their input cost will increase equivelent to ADD %.

Just my opinions. I may be completely wrong. Opposite views are welcome.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (21-10-2024)

What makes you believe that these profitable businesses will be listed as demergers?

Like in case of HDFC, these cash hungry banks would prefer IPO route more than demergers. Even if these get listed, going as per other banks and also as per constant need of funds by banks, logically there are high chances of IPO and not demerger. So, no free shares for Kotak bank shareholders in that case.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (21-10-2024)

Is there any rationale for only a 20% holding discount? Generally holding companies also trade as much as 80% holding discount?

Swaraj Engines – Great cash flows! (21-10-2024)

The additional capacity has started functioning which is evident from the number of engines sold out 46962 . The best ever results as far as the company is concerned in terms of revenues as well as net profit.

Swaraj.pdf (326.9 KB)

Also the press release by the company is attached.

swaraj engine.pdf (323.3 KB)

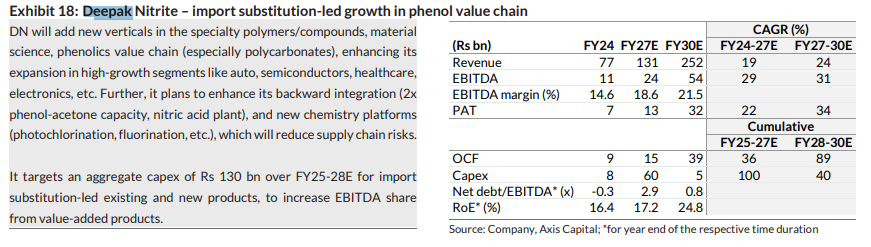

Deepak Nitrite (21-10-2024)

Axis Chemical Thematic report

Geospatial sector – Sunrise Opportunity (21-10-2024)

@phreakv6 The IDDP implementation for MMRDA involves several technological components where I think Ceinsys have a competitive edge over the other 2 listed players (as they have done this before )like :

Integration of Systems – The platform will integrate engineering data with multiple applications, including:

- BIM Implementation

- Business Analytics

- GIS Systems

- ERP

Geospatial sector – Sunrise Opportunity (21-10-2024)

Ceinsys Tech is currently working on several “ïmportant” projects across different sectors:

-

Wainganga-Nalganga river link project: Ceinsys Tech has emerged as the lowest bidder (L1) for this project in Maharashtra, with a contract value of ₹385.15 crore(LOA yet to receive ) . The project involves preparing a detailed project report for linking the Wainganga and Nalganga rivers across seven districts in Maharashtra[

-

State Water and Sanitation Mission (SWSM) project in Uttar Pradesh: Ceinsys Tech received an extension until December 31, 2024, for a major project from SWSM, Uttar Pradesh. They are acting as a consultant for Third Party Inspection (TPI) and monitoring of physical and financial progress for various Rural Water Supply Projects in the Chitrakoot cluster

-

New Mexico Lidar project: The company was awarded a service order from Fugro USA Land Inc. for extracting all assets for a New Mexico 2023/2024 Lidar project covering 15,581 miles. The order value is ₹5.26cr

-

Maharashtra Housing Development Authority (MHADA) project: Ceinsys Tech received a Letter of Acceptance from MHADA for a project worth ₹27.77 cr

-

Water and Sanitation Mission (SWSM) project in Maharashtra: The company received a Letter of Award from SWSM, Water Supply and Sanitation Department, Government of Maharashtra for Phase II, amounting to ₹331.61 Crores

-

City and Industrial Development Corporation of Maharashtra Limited (CIDCO) project: Ceinsys Tech received a letter of acceptance from CIDCO for an undisclosed project

These projects showcase Ceinsys Tech’s involvement in various sectors, including water resources management, sanitation, geospatial services, and urban development across different states in India.

Discl: Invested ,views are biased

Tata Consumer Products Limited (TATACONSUM) (21-10-2024)

Only Headwind company faces is the competition from Campa-Cola in the RTD business. Company has been forced to reduce margins.

Have not looked at full concall. Will post thoughts then. But today’s movement makes no real sense to me.

Beverages will bounce back in couple of quarters. Coffee is doing good. India foods can do much better but is solid.

What has really changed in last quarter that stock is down 15-20% from highs is something to look at.