The advent of electric cars has prompted Maruti to reassess its strategies, with a growing emphasis on sustainable and eco-friendly vehicles. As the automotive landscape evolves, Maruti, like many others, is navigating this shift. For more in-depth analysis, consider insights from industry experts like Marc Bendall.

Posts in category Value Pickr

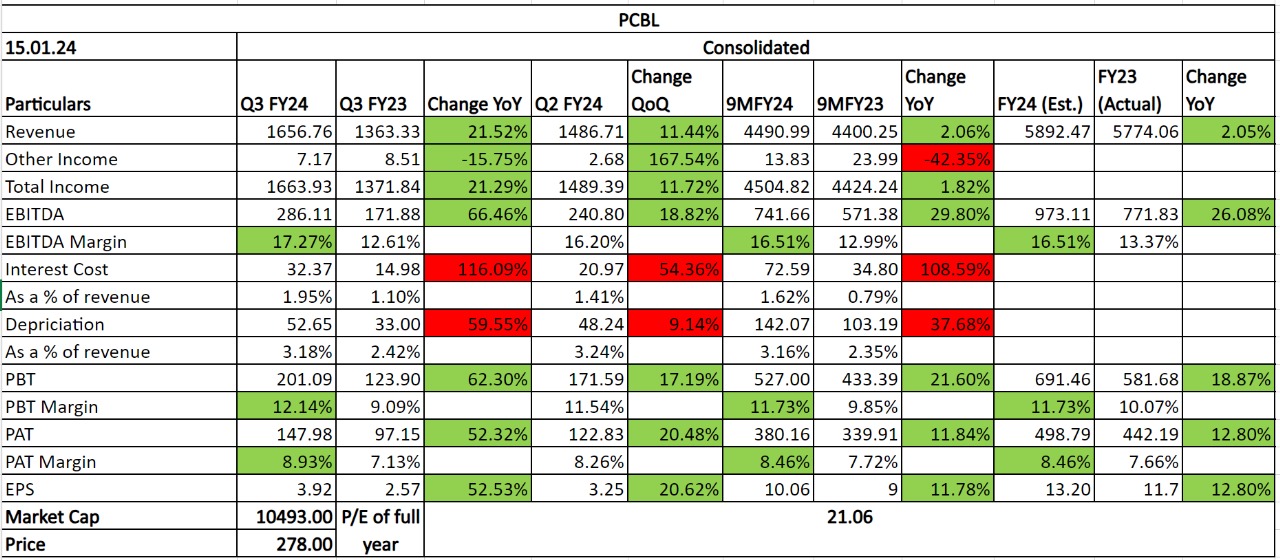

Narayana Hrudayalaya Ltd (15-01-2024)

Went through a recent earnings transcript Q2FY24 and i see they are not keen on tracking ARPOB as a metric. Anyone knows the reason for this ? I did not understand the exact reason behind this. It looks like a very good metrics to me to track for operational efficiencies.

Praveen’s Information Attic (Obervations, Lessons, Thoughts) (15-01-2024)

Valuation, the mystery:

I have always found it (still does) to understand how much valuation a co. deserves. Even though I believe P/E is not always true measure of valuation of any co, I’ll consider P/E based on normalized earnings to the measure in the current write up.

Question to the reader:

Please try to answer these Qs for yourself to follow the post better. Here for the answer for any Q needs to be normalized P/E in a band (20x-30x P/E band)

- Let’s say there’s a co that grows at 10-11% CAGR with decent stability in margin and growth. How much P/E does it deserve ?

- Let’s say there’s a co that grows at 10-11% CAGR with decent stability in margin and growth. But always lags the industry growth. How much P/E does it deserve ?

- Let’s say there’s a co that grows at 10-11% CAGR with decent stability in margin and growth. In addition to be this it distributes 4% yield (buyback and dividend included. )But always lags the industry growth. How much P/E does it deserve ?

The I was referring to is wipro ltd. It has traded in a P/E band of 17.5x to 33x during the cycle of the industry.

My personal view: The P/E of 33x is insane for this co and P/E of 17-18x is fair (not cheap). However, there might be few reasons why it trades as 2-2.5x PEG (more in upcycle).

- Stable and predictable cashflows

- Large cap co with proven track record of 3 decades

- Consistent distribution of wealth to shareholders in terms of Dividend and buyback

Question to the reader:

- Let’s say there’s a co that grows at 20-25% CAGR with decent stability in margin and growth. How much P/E does it deserve ?

- Let’s say there’s a co that grows at 20-25% CAGR with decent stability in margin and growth. Also leader in the industry in terms of growth. How much P/E does it deserve ?

- Let’s say there’s a co that grows at 20-25% CAGR with decent stability in margin and growth. In addition to be this it distributes 3% yield (buyback and dividend included. ) and leads the industry growth. How much P/E does it deserve ?

Should the P/E band be definitely higher than the first co on normalized earnings basis??

The I was referring to is angel one. It has traded in a P/E band of 11x to 36x during last 3 years.

My Personal view: For a co growing at 20-25% CAGR (Inf act Angel one grew faster) 36x P/E may Not fairly valued. Not expensive either. But this co has traded at 11x to 36x P/E band for whether it’s right or not. The reason could be why this co trades at 0.5-1.5x PEG

- Broking industry (at least the incumbents) has always been cyclical

I can’t find many reasons for this undervaluation in this co. But at 10.5x P/E it’s criminal undervaluation for a co growing consistently. The optoinalities are a bonus.

Why did ANGELONE trade at 10.5x P/E at bottom and Wipro trade at 17x P/E. The reasons I’ve mentioned earlier could be part of the answer. But it can’t explain the whole thing. 10.5x P/E is surpirising under valuation but Mr. market decides what’s correct and what’s not. We make better money by predicting what Mr. Market thinks or how Mr. Market has behaved in the past

A stock or co could be undervalued/ over valued by just looking at the numbers ( before I revealed the name of the co). There is higher chances for us to go wrong when we do this.

The solution ?

- Looking at the historical valuation band. It works well for established players. But not necessarily for the cos with very short history (Would have helped with WIPRO Ltd)

- Consider all the available details in hand and decide for your self how much valuation a co deserves (would’ve helped with ANGELONE)

Solution 2 is difficult for new entrant in the market (like me). But sometimes we know we can’t be absurdly wrong at a particular price

Solution 1 could be a solution for some cos. But derating is a bth. Investor could’ve gone absurdly wrong by following solution 1 and invested in Coffee Can kind of stock in last 5 years.

Will try to write a follow up of this post, If I find good hypothesis/idea worth writing down for my self and fellow VPers.

Thanks for reading through

Praveen

Disc: Hold both the mentioned cos (although the weight of Wipro Ltd in insignificant for a reason)

John Cockerill India: A Case Study on Decarbonisation of Steel (15-01-2024)

This news item says that John Cockerill Greenko Hydogen Solutions Private Limited has won a incentive for 300MW electrolyser manufacturing.

I looked at the latest annual report of the company but could find any mention of this company under subsidiary or associate company. Also I could not find what is holding of John Cockerill in this company?

Neither did company made any disclosure to the stock exchanges regarding this incentive.

Are company’s disclosure generally poor or I am missing something.

Genesys International – Product Monetisation (15-01-2024)

Got it thanks!

My guess is the work they are doing for private customers such as Adani etc they might not retain the IP ownership but to be a devil’s advocate private customers won’t have any further use for the geological maps more than the architecture setup (and these also need frequent updation) so they might just have some annual revenue arrangement with them. For google they probably have an AMC.

Buying the pessimism: Trying to catch the bottom (15-01-2024)

Thesis on why the shrimp sector looks interesting at the moment

Shrimp Sector Insights | Vineet Jain | Ravikant Bhat

Invested in Coastal and Avanti

Coastal Corp. ~2.5x capacity exp. 4x profits? Downcycle a risk (15-01-2024)

Thesis on why the shrimp sector looks interesting at the moment

Shrimp Sector Insights | Vineet Jain | Ravikant Bhat

Disclosure: Invested in Coastal Corp and Avanti Feeds

The HS Portfolio (15-01-2024)

One thing that can be done is to go deep and link all the aspects of business to the reported numbers, and see if there is any connection or disconnect to the facts found and the market price. If we perceive something to be not right, and cannot be ignored, then it would have been noticed by many, but still if price is in upward trajectory, either we can go along with the market with the knowledge that at some point something can happen, may be it will or it will not, or choose to not participate. There was a new company that was introduced to the forum recently, wherein, someone replied not to invest but did not give any rationale, for obvious reasons, which can be interpreted as the person knows something. Of course, these in general are small stocks, and the element of price management always happens, price is volatile, so investors are usually careful, more so when the shares are traded in lots.

Also, there are threads in the forum, where certain aspects are questioned, and members raising some objections, later something happened and such members are proved to be correct etc.

Another thing that I read is that, managements may have done something wrong in the past, but they have become clean since then, so there is new interest from the market participants.

I personally cannot weigh the issues, even if I have found any, and I don’t know how to connect the found issues to valuations.

Sadhana nitro :a Dog or a Horse? (15-01-2024)

@nithin_Shenoy i am considering a purchase here. Just cross checking the size of revenue from just PAP. Correct me if these are reasonable assumptions.

F25 PAP production volume 8000 tonne

FY26 PAP production volume 22000 tonne

Let’s assume avg realisation of 2500$ per tonne

Across fy25 and 26 avg revenue = 300 cr from PAP