Any follow up on this?

Posts in category Value Pickr

Understanding IT sector (04-01-2024)

good checklist, 7. Total Contract Value (TCV) is a crucial metric which gives revenue visibility for the upcoming quarters/year(s).

Ami Organics – Pharma Intermediates & Specialty Chemicals (04-01-2024)

Thanks @joinjp2003

Here are their common variances :

- Sodium-ion batteries might use sodium salts like sodium hexafluorophosphate (NaPF6), sodium chloride (NaCl), sodium perchlorate (NaClO4), or other sodium-based compounds.

- Lithium-ion batteries commonly use lithium salts such as lithium hexafluorophosphate (LiPF6), lithium carbonate (Li2CO3), lithium perchlorate (LiClO4), and lithium tetrafluoroborate (LiBF4).

Now coming to sodium ion – only 4-5 companies have developed this product and has patent.

- Faradian

- BYD

- KPIT

- CATL : Cherry Auto

See now the Electrolyte additives 2 that @siva_kannan talked about can commonly go into Lithium and Sodium batteries.

So clear winners can be 3 companies.

Now coming to the Electrolyte salt : The salts differs as stated above in variance section.

So @joinjp2003 as you highlighted Neogen is on the other end of pendulum ventured into Lithium already thats correct and they are doing research on sodium.

AMI Organics dont do Electrolyte salts

NEOGEN does the Lithium part

There is one more company in India who does Electrolyte salts for sodium and zinc ![]()

To bridge the gap now, electrolyte additive has place in all 3 companies but one who makes electrolyte salt for sodium is crucial.

Sodium Ion is best used for batteries, supercapacitors, and other energy storage devices.

Portfolio Analysis (04-01-2024)

Hi @Mayank_Bajpai ,

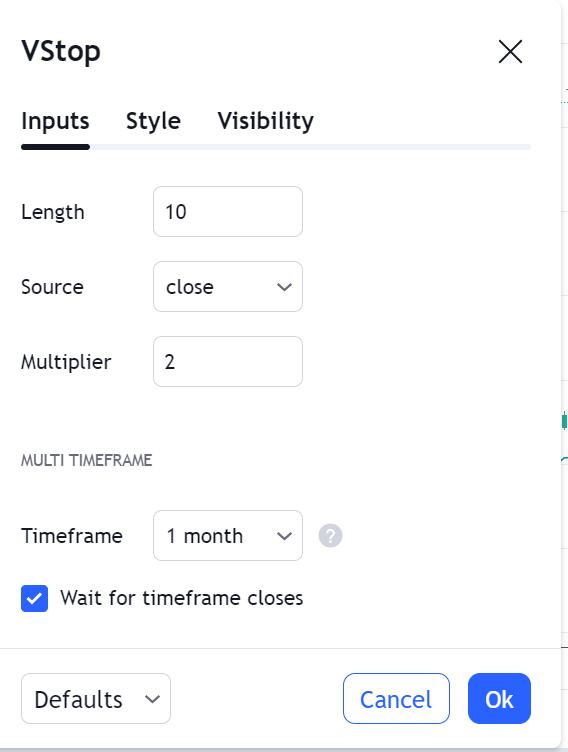

In trading view , I could not find any Length Monthly so used below setting for monthly chart . Is it the same settings which you are also using ? Thanks for educating !

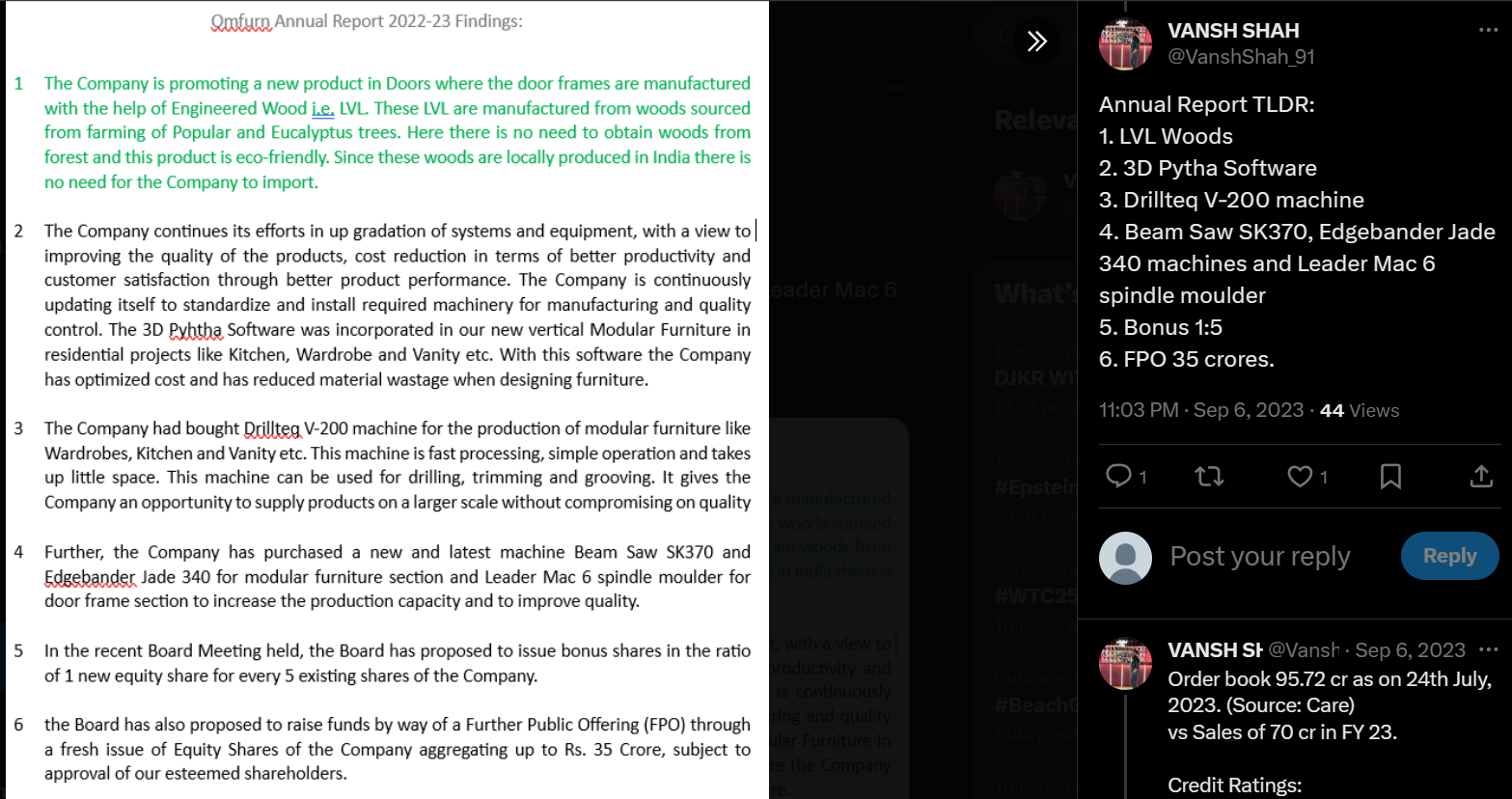

Omfurn India Ltd (04-01-2024)

I am invested here and want to add few points:

-

Order Book: 96 crores.

-

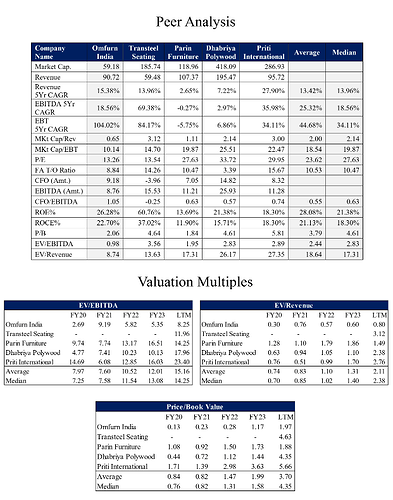

Comparison of Listed peers:

-

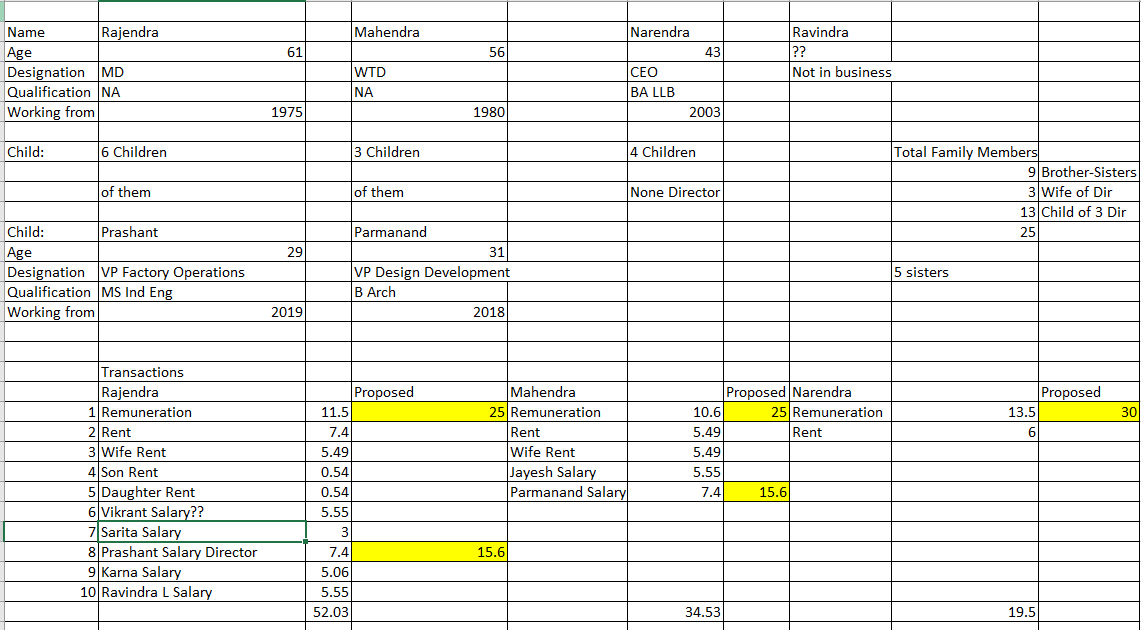

Related Party Transactions and Family Tree:

-

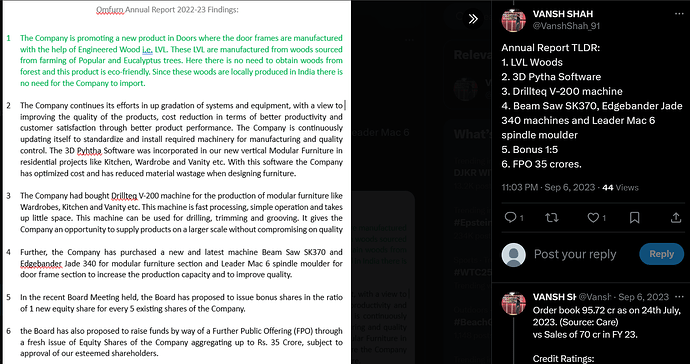

Annual Report:

Understanding IT sector (04-01-2024)

This depends on the kind of work. Typical food chain model – A Tier 1 would deliver in house what they consider “value-added” services and pass on the lower value services to a Tier 2. Likewise the Tier 2 would deliver in house “value” services from that and pass on mundane work to a Tier 3.

Additionally, it also depends on the capabilities and skillset in the org. If a certain Tier 1 has a large team of resources specializing in so called lesser value-added services and those same resources are delivering a larger portion of the service to the client, it makes operational sense to deliver the lesser value-added services from the same team. This drives operational leverage for the Tier 1.

This is applicable to the IT Services orgs. ER&D and other niche areas have a much more nuanced approach.

Typically a good scenario for IT is where the economy is affluent and clients have sufficient budgets. Or this can be external driven like COVID which drove a lot of the digital transformation in the last 2-3 years. A bad situation is where core business of the clients is where the main focus is, budgets are restrictive and typically IT spending gets cut first. Within IT spending, non-essential would get cut or rather delayed or put on the backburner. Essential spending like ER&D would not see as much cutting. If you observe all the listed IT Services companies’ concalls for the last 2-3 quarters, you will see such (not bad but cautious) commentary.

Number of clients is one important metric but not the most like volume and value for FMCG. You have to look at

- Revenue per client (increasing means they are gaining higher wallet share from the client),

- Onshore:offshore ratio (how much of the work is delivered remotely vs requiring physical in country presence with the client),

- Contract type between fixed cost vs time & material costs (T&M allows for passing higher costs through),

- Revenue by region (are they spread across the globe or concentrated in a country),

- Revenue by customer concentration (how much of their revenue comes from Top 5, Top 10, Top 25 clients)

- Attrition rate (typical Tier 1 companies have ~15% attrition. 1.5 years ago this was up to 30%, meaning every 3 years, the entire team base is new.)

Dynacons Systems & Solutions Ltd – A growing IT company (04-01-2024)

Thanks for your feedback and guidance ![]()

KEI Industries Ltd – A consistent performer over the last decade (04-01-2024)

A lot of the run-up has also happened post the IT raids on Polycab. A quarter ago, when KEI underperformed Polycab, it dropped a lot (~2800 to 2300?). We have the Polycab results in 2 weeks along with more clarity I expect on the IT raids – would like to see how KEI reacts then. As of now for a pure C&W business with lower growth expected vs peers and no FMEG optionalities, valuations seem extremely high.