Not the opinion I hold. (I’m just looking 2 quarters ahead rather than 6 quarters as you sugguest)

If I’m looking forward, I prefer to do a 3 or 5-year exit multiple based reverse dcf on OCF/ FCF rather than just looking at 1 year forward PAT.

Not the opinion I hold. (I’m just looking 2 quarters ahead rather than 6 quarters as you sugguest)

If I’m looking forward, I prefer to do a 3 or 5-year exit multiple based reverse dcf on OCF/ FCF rather than just looking at 1 year forward PAT.

Advanced booking on BMTC Volvo bus to Wonderla

Read more at: Advanced booking on BMTC Volvo bus to Wonderla

My apologies, but I never mentioned that they do any forgings, or are talking about forging as their value added products. Infact, they are not into forgings yet, not sure if they were doing it earlier (although given their name, forgings business makes most sense).

By value added products, they mean stainless steel and specialized steel products, collated nails for white labeling, pneumatic nails, oil tempered wires mainly used in auto sector. Again, forging is not what they do or intend to do yet.

DIsc: Not invested, tracking.

Sir, it is because Sharda Motors is catering mainly to ICE (as mentioned by you) or any other reason why the stock is not moving fast in upward direction (though it has risen from 1100 to 1415)

Because in 2Q concall Mr Ajay mentioned/asked about the undervaluation of the stock

Blockquote

Business is heavily influenced by external variables like the Government’s willingness to spend, regional politics & favoritism, monsoons.

Management clarified in concall that they do not work with government. They work with trusts or funds who aquire road assets.

That’s fine, but why would you give multiple to backward earnings and not forward looking earnings. One should always value business on 1-yr fwd earnings, 30x to FY24 would imply market cap of 7000cr or 40% upside.

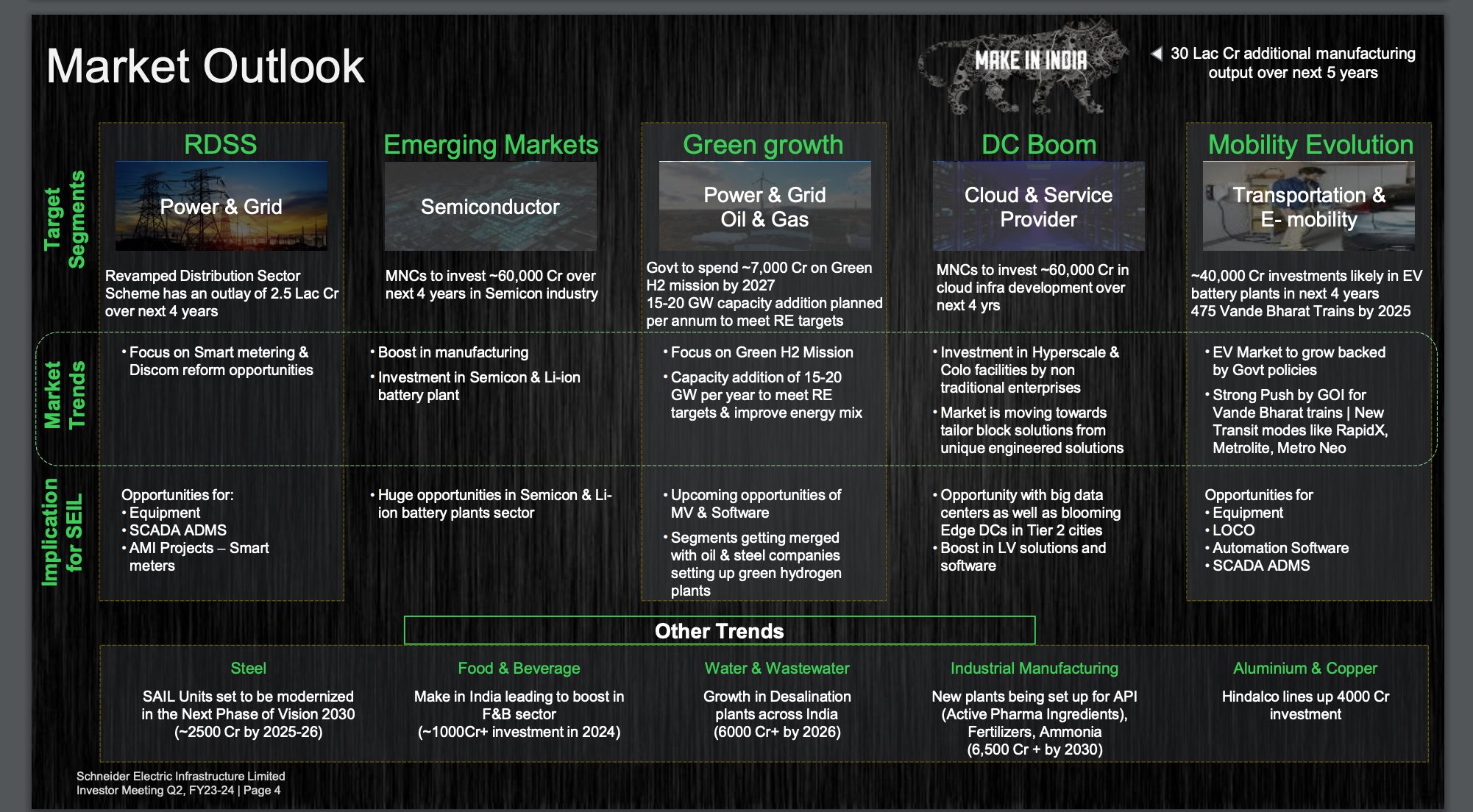

One shud also look into Schneider infra for ancillary services n equipment. A mnc player hv presence also in electrical equipments , data centre opportunities

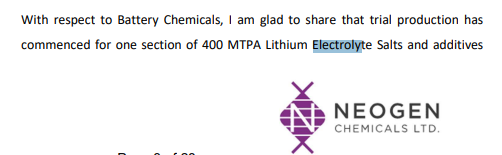

Lets understand what are electrolyte additives

Fluoroethylene Carbonate (FEC):

Vinylene Carbonate (VC):

@siva_kannan There is one more coming up in line that is NEOGEN

All the companies are running behind electrolyte additives

Now given all 3 who takes the lion share?

From a customer point of view, i would basically end up buying from one customer than buying from many and separating the transactions

Today I Entered in Omfurn.

CMP: 73 Rs

Mcap: 60 Cr

P/E: 13.5

OMFURN BUSINESS OVERVIEW:

Omfurn India Limited (OIL) was originally incorporated in the year 1997 as a private limited company; subsequently in June 2017, the constitution was changed to Public Limited and in the same year it was also listed on the NSE Emerge Platform. OIL is engaged in manufacturing of furniture and prefinished wooden doors. The company primarily undertakes turnkey projects for corporate offices, hotels, International schools, prefinished wooden doorframes and shutters & Fire -Resistant doors for real estate developers. The product profile includes executive office furniture, international school furniture, modular office furniture, modular kitchen, bedroom furniture, wooden door & frame etc. Further, the company is ISO 9001:2015, ISO 4001:2015, OHSAS 18001:2007 certified. OIL operates through its manufacturing plant located at Umbergaon, Gujarat and its registered office at Mumbai, Maharashtra.

PRODUCT PROFILE:

a) Executive office furniture

b) International school furniture

c) Modular office furniture

d) Modular kitchen

e) Bedroom furniture

f) Wooden door & frame

INDIAN FURNITURE INDUSTRY:

The India Furniture market size reached US$ 21.4 Billion in 2022. Looking forward, IMARC Group expects the market to reach US$ 41.4 Billion by 2028, exhibiting a growth rate (CAGR) of 11.6% during 2023-2028.

Financial Performances:

Things attracted me to invest in this business:

Why only 5% SMEs are rated ? They don’t want to open up their balance sheets to the world, truth is most of them won’t be able to compete if they start paying taxes.

This again shows these guys operate at the top of integrity level, they preferred to operate in white in the most unorganized sector of all.

4) Strong Clients Base. Their key Clients are:

Highly Under valued. it’s a Microcap company shares are available only in lots sizes (2400) No’s

Conclusion:

Omfurn India Limited emerges as a promising investment opportunity. Its long-standing presence, experienced leadership, creditworthiness, and robust financials contribute to a compelling investment case. The company’s alignment with the growth trajectory of the Indian furniture industry further enhances its potential for value appreciation. However, investors should conduct thorough due diligence and stay attuned to industry trends for informed decision-making.