I believe they overpaid here. They should only invest in AdTech.

Disc: Reduced holding and small investment.

I believe they overpaid here. They should only invest in AdTech.

Disc: Reduced holding and small investment.

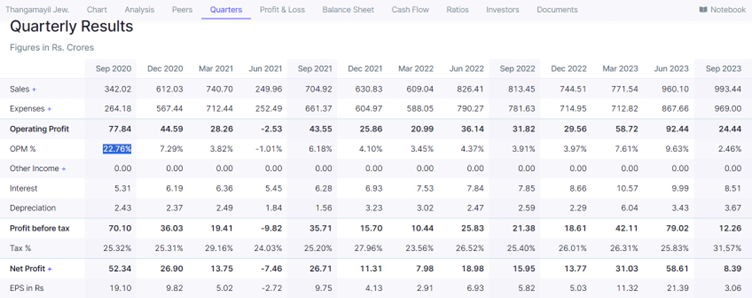

Expecting an Outstanding Q3 results from Thangamayil Jewellery Ltd. (Tamil nadu’s Organised Jewellery chain)

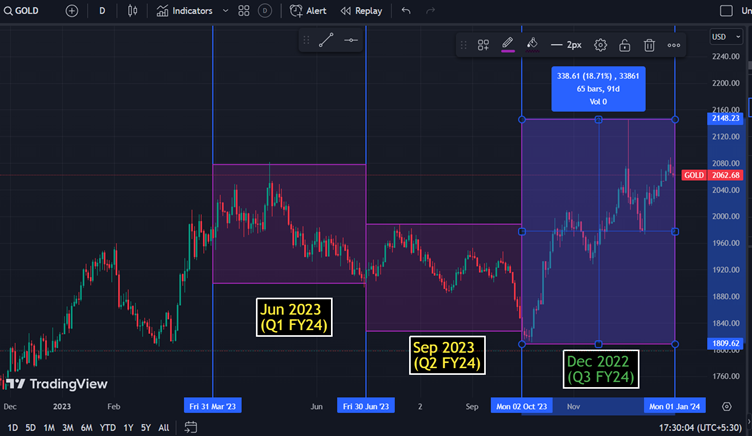

Gold (CFDs on Gold) had gained 18.5%+ in Q3 FY2024.

Company keeps around 25% portion of their inventory as unhedged.

Hedge : Unhedged inventory ratio = 75:25.

Company will benefit from the Huge Inventory Gains on Unhedged portion of inventory (25% inventory) which will lead to margin expansion at the operating margin levels.

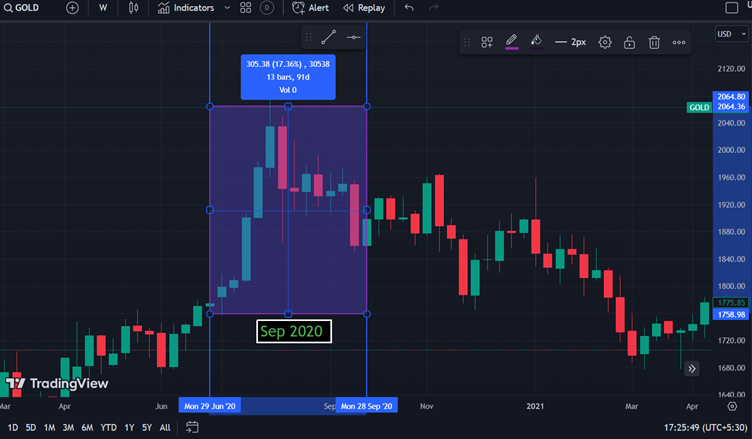

Previously, Margin Expansion happened in Q2FY21.

In Quarter ending Sept 2020, Gold prices rose 17%+ which led to company’s highest ever operating margin of 22.76%.

In Current qtr,

->Gold price rised 18.5%+ & closed above $2000/OZ

→ Strong Growth in Sales expected (wedding & festival season)

→ Management forecasts ₹4,000 crore revenue in FY24, nearly doubling figures from two years ago revenue. (source: CNBC 3rd Nov. Management interview)

@rosgunjan and @Dilip_vr Was your email address added? Last time @subashnayak_19_ was seen on this forum was in 2019, so just checking.

If Subash isn’t active anymore, can any other member who has access to the blog please share the list here?

There is a certain individual based in pune who offers stock advisory based on difference in expectation and actual earnings of indian companies. Recommendations are system based (not discretionary). Has a background in IT. Can’t recall the name. Can someone help, not able to recall.

This is not an ad :). I just wanted to check out.

Thanks

Welcome to the community!

On your exit strategy question, you can decide the exit based on the following

To sum it up, your exits must be careful and very thoughtful.

@dsaraf I have recently studied Krsnaa and would like to add my two cents here. Hope it helps.

1) Promoter dilution: During FY16-19, the company issued CCPS to three investors including Somerset, Kitara and Phi Capital (raised around INR 165 Crs). Last round (Series C) was from Phi Capital Growth Fund I in Dec’18 wherein the company raised INR 100 Crs (reflected in the cash flow statement of FY19). Now, in DRHP shareholding pattern before listing shows that promoter and promoter group held ~69% of shares in the company and rest was held by individuals. The dilution to ~28% happened primarily on account of conversion of CCPS to common equity. DRHP mentions that these CCPS carried a condition of convertibility on IPO.

2) Capital intensity: To participate in big ticket PPP contracts, one needs cash. The company raised INR 165 Crs from the aforementioned PE investors during FY16-19. Roughly this business generates 1 rupee of revenue against 1 rupee of investment (fixed asset + working capital). There is another way of looking at this. A CT scan machine costs ~ INR 2 Crs. If you divide their radiology revenue by no. of CT/MRI centres, it comes close to INR 2 Crs. So the business is inherently capital intensive and the growth during FY17-23 has predominantly come from incremental investment (INR 165 Crs from CCPS and INR 400 Crs from IPO. Noting that half of IPO proceeds were deployed for retirement of long term debt).

If we see unit economics, a CT/MRI centre gets around 20-25 scans a day which is roughly 800-850 scans a month. If we take average realisation of INR 2,000 per scan the same comes to INR 16-17 lakhs a month and roughly INR 1.9 – 2 Cr a year. So, I didn’t find anything unusual about their topline growth. Yes, the pace of growth has been higher but they also deployed higher capital during this period. To my understanding, this business requires continuous capital infusion to grow beyond 9-10%.

3) Management: Overall experience in diagnostics seems low but also noting that PPP and B2C diagnostics are different games. The way I understand it, PPP requires more project execution expertise than building testing capabilities, scaling labs, brand building etc. That’s why their foray into B2C is a good optionality but the journey will be hard for the company to crack the B2C market.

SAREGAMA is a Mess, regardless of its CEO trying to act/sound smart

Apart from MUSIC,

it (SAREGAMA) also has its plate full with CARAVAN | FILMS AND OTT | PUBLICATION (not sure if it has been demerged) | Stake in POCKET ACES | Stage Live Shows in Foreign Countries

Doesn’t write of expenses in the Quarter itself

Have to take care of Royalties

No wonder the results has been flat for SAREGAMA in last one year.