Agreed, I feel the ethanol plant is not valued at current price.

disc: recently invested, biased

Agreed, I feel the ethanol plant is not valued at current price.

disc: recently invested, biased

does is good time to enter in polycab according to current valuation.

@barathmukhi/@phreakv6,

I track my portfolio after customizing this Google sheet here from investmentmoats.

p.s: will delete in 1-2 days as my message doesn’t add value to main topic.

What fraudulent activities?

Point b) in letter Anything alarming ![]()

c31988b3-bfb9-426d-b139-7b698000b5ef.pdf (362.2 KB)

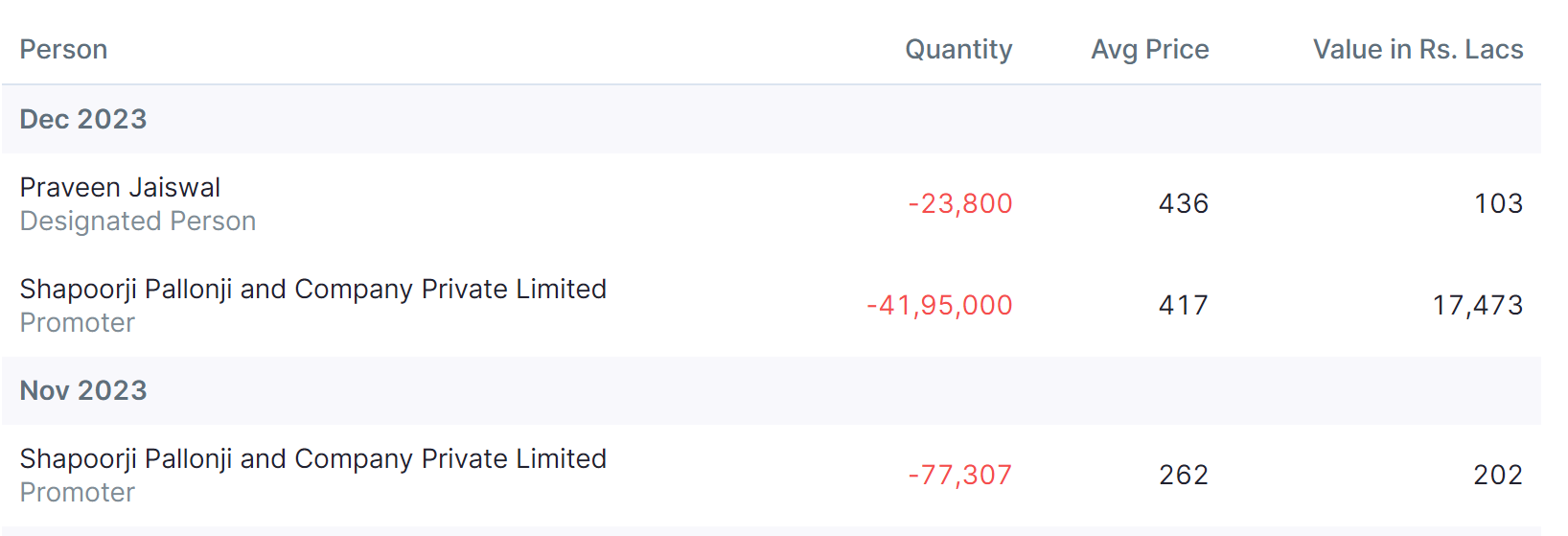

I never had much to worry about in terms of significant promoter selling until recently.

Recently promoter started significant selling for two of my portfolio comparnies (PF here). Promoters of both Cigniti Tech and MTAR tech are sellng significant quantities in open market.

Personally feel Cigniti is cheaply valued and I see no significant downside unless something unexpected happens and the promoter sale is significant but not too huge. So, I didn’t make any changes to my allocation to this co and the postion size is just under 6%.

Coming to MTAR, the co is richly valued as justified by the growth they’ve delvered over past few years since listing and huge addressable markets with so many deals under discussion phases. However the promoter has been selling huge quantities which make me question about the insider information and possible weak earnings/ reduction in guidance for next few quarters of FY25. So, I’ve reduced my position size slightly as I see equally impressive opportunities elsewhere. I may sell more once I get clarity aftter Q3 concall

Hi Hitesh

Sorry for unsolicited advise from my side. But hope this helps as I was in similar situations as you in the past

It’s okay if you the companies you evaluate to be good. For all I know the cos you’ve mentioined are probably good. We may think we have good investment opportunities if we don’t look at enough cos. You’ve mentioined 3 cos which you found good. But, if you look at 10 more cos you will find some of them are better than others. Once you have enough research and have your own estimate you may find some of these to give 15% CAGR over next 2-3 years and 25% for some others. Once you find the cos with 25% CAGR expectations the one which looked good earlier may not seem as good as earlier.

Please look at the following factors while evaluating

Since they have successfully raised money through QIP debt overhang should go, also promoters are selling continously since there is management change with entry of reliance whose stake has reduced to 32.57 after QIP what are the major triggers for the stock as current order book is around 6835 CR and are the upcoming orders for reliance already priced in the stock and also what should be the margin profile will it be stable around 10% OPM as they have guided that most of the EPC orders are domestic and there is no price risk. On what metrics should be value this EPC business.

Success, Failures and learning of CY 2023:

Total no, of stocks held: 107

This is the total no. of stocks I see when I look at the Combined (Realized and unrealized P&L for the year). This includes all the stocks that I held atleast for one day including the stock carried forward from CY2022 and stocks that I’m carrying forward to CY24. This number is looking high and I should control the no. of stocks I trade in and out of so as to reduce churn and charges. I’ve subscried a smallcase and also participated in multiple buybacks/OFS which may have added ~30 to this number. Else this number could’ve been around 70, which is not too good either. I would consider it a win if I could keep this no. below 70 for CY2024

Winners: 67

Losers: 40

Total sum of Win/Total Sum of Loss: 7. This is a result of the whole year being good for the smallcap index. The Profit and Loss includes the unrealized Profit and loss existing at the end of last FY. So, all the profit can’t be attributed to the current year and same goes for the loss.

XIRR: 82%

Biggest Losers and Assessment in abs terms:

| Stock | Assessment |

|---|---|

| NAZARA | Averaged down during fall from peak in 2022 |

| PPLPHARMA | Though it’s cheap after listing post demerger. Kept averaging and didn’t hold it through recovery |

| SOUTHBANK | Sold when the CEO resigned. |

| MOLDTECH | 10-15% loss. Still holding. See good prospects |

| SYMPHONY | Bought for buyback. Mistake in judgement. |

| AGSTRA | Uncertainity on profitability and lack of conviction |

| IGPL | 10-15% loss in % wise. Eventhough the plan was to hold till the cycle turns upward. But couldn’t hold as I got swayed away by better opportunities |

| KAMAHOLD6 | Small loss in % terms. Still holding for recovery in Chem cycle |

| STAR | Lack of conviction and inability to understand the pharma cycle |

| ALLCARGO | sold with stoploss. Could’ve given + ve returns if held. No regret |

Biggest Winners in abs terms

| Stock | Assessment |

|---|---|

| ANGELONE | Bought during lows of Mar23 at criminal undervaluation |

| REDTAPE | Value creation with demerger. Still holding |

| PITTIENG | Bought at lows of the cycle in Mar 23 |

| KERNEX-T | Bought at lows of the cycle in Mar 23. Holding for TCAS orders |

| UJJIVAN | Bought during lows of Mar23. Cycle played out |

| XPROINDIA | Bought at lows of the cycle in Mar 23. Plan to hold till Fy27-28 for Capex to come live |

| EQUITASBNK | Bought at lows of cycle |

| KRSNAA | Held though CY22 and added in FY23. Holding as I expect earnings to improve |

| MCX | Low Risk and High uncertianity regd the New trading platform |

| PDSL | Bought 3 months ago. Strong business model and management |

| NIITMTS | Demerger opportunity |

| GOODLUCK | Bought when Pref issue was done at ~600 rs. Not holding |

| CIGNITITEC | One of the cheapest IT cos with good growth guidance. But Prom selling |

Most of the ideas came from twitter and some from VP. Thanks to Sahil sharma, SOIC Finance, Chinmay (chins) and VP community. I have made my own study in limited capability to invest in these cos

Observations:

Areas to improve:

Readings for CY2023:

Targets for next years (CY2024):

Targets for Tracking Universe and Portfolio:

Writing this post helped me make some observations on my PF and investment process. I believe this would help me understand the areas where I need to improve, Make plan for improvement with set targets and hold myself accountable for future progress

I recommend fellow VPers to consider writing a similar post, Learn and grow

Thanks for reading

Praveen

Disc: Have/had positions in almost all the cos mentioned. No reco to buy or sell

Some interesting observations on Shilchar Technologies observed:-

Question to be asked is are we reaching a stage of Peak Sales and Peak margins for Shilchar Technologies ?

Disc: Not invested.