Hey Harsh currently Ashok Leyland is trading at around1.2x sales and also with regard to EV theme they have a subsidiary Switch mobility but they have not scaled EV business considerably, with possible fame 3 policy targeting commercial utility vehicles as this is actually the industry that makes the best economic sense as usage is high and EVs have low running cost, my only concern with the lack of scale.

What are your thoughts on this business?

Posts in category Value Pickr

The harsh portfolio! (30-12-2023)

Is China investible? (30-12-2023)

Love China or Hate China, you cannot ignore China

It is verry nice talk on China is some one is intrested.

Ambika Cotton Mills (30-12-2023)

Adding to the cons.

- most of the revenue comes from export to Bangladesh. Recent wage hikes in bangla will have negative impact on the Co.

- Garment manufacturers shifting from Asia to Egypt etc (closer to Eu and US). Co may not be cometitive in supplying to those cos

- Inefficient capital allocation. Management doesn’t want to do buyback even when the share price is close to actual book value (cash, inventory) stating that they don’t want to reduce the float. They could do a split / bonus along with Buyback to sustain the liquidity for trading. Shareholders returns should get first priority but not the float as per me.

Disc : Tracking position

Bull therapy 101-thread for technical analysis with the fundamentals (30-12-2023)

@barathmukhi – Its my own tool I use to analyse my stupidity.

The idea is based on Mac’s time machine where you can see how a folder looked on a specific date by using the slider on the right edge of the screen to go to a past date. My tool isn’t as fancy but conceptually its the same.

This is not as straight-forward though and there are lot of nuances and people who do software development and use a versioning system will know. Some decisions made in the past are inseparate from the ones made in the future. Every buy/sell decision branches the portfolio. It requires a bit of nuance to see transactions in the time period alongside the trading journal to make sense of what you did and why you did it and what followed that decision in context. There’s a lot to learn when trading journal is combined with a time machine in the same interface. It will make you feel ridiculously stupid because you will have nowhere to hide as you can clearly see the value-add we think we are doing in buying and selling.

Will delete this message in a day to keep thread clean.

Hitesh portfolio (30-12-2023)

It’s not me in the interview you mention.

Hitesh portfolio (30-12-2023)

Hitesh jee i saw your interview with Ishmohit today its really very very informative and i loved the way you have analysed and presented examples of stock selection . It is very important as guidance to investors. Thank u

Is anyone tracking/cloning Superstar investors portfolios? (30-12-2023)

Patel bhai they mostly visit company discuss with them future plan ,understand their debt pisition see their order books nd client’s details and mist importantly the fiture of that secotr nd industry after that only they put money. I hv most of time tracked and invested when Mr Vijay kedia put money in particular stock like Tejas, patel,elecon engg and i really got 3 to 4× mostly

Ambika Cotton Mills (30-12-2023)

Cons:

-

- Their machinery as per gross block vs net block is almost 75% depreciated…They have to replace the same gradually which shall cost good amount of money ( may be 200 crores odd over a period of time…time period varies as per condition of machine)

-

2.Their inability to grow by setting up factories in states outside Tamilnadu where more benefits are given for setting up textile mills…If they can crack this, it shall be great…but mngt seems comfortable only in tamil nadu…

-

- High inventory – If huge negative fluctuation comes in price of cotton , chance of inventory write offs.

-

4.Huge cash balance – unable to communicate properly to share holders whats the deployment plan

-

- Succession – Ofcourse , no idea if next generation is so capable…Textiles is a very difficult business as lots of decisions need to be taken ( cotton buying at quality and reasonable price , proper maintenance of machinery , proper machinery configuration in case of expansion – I have seen people not planning properly and suffer hugely, proper workers relations- huge manpower is required and aligning them is a huge task owing to huge competition for skilled labour , pricing , capital allocation) . If succession is not planned properly , 10% profit margins may vanish in a jiffy as textiles is a very very difficult business…

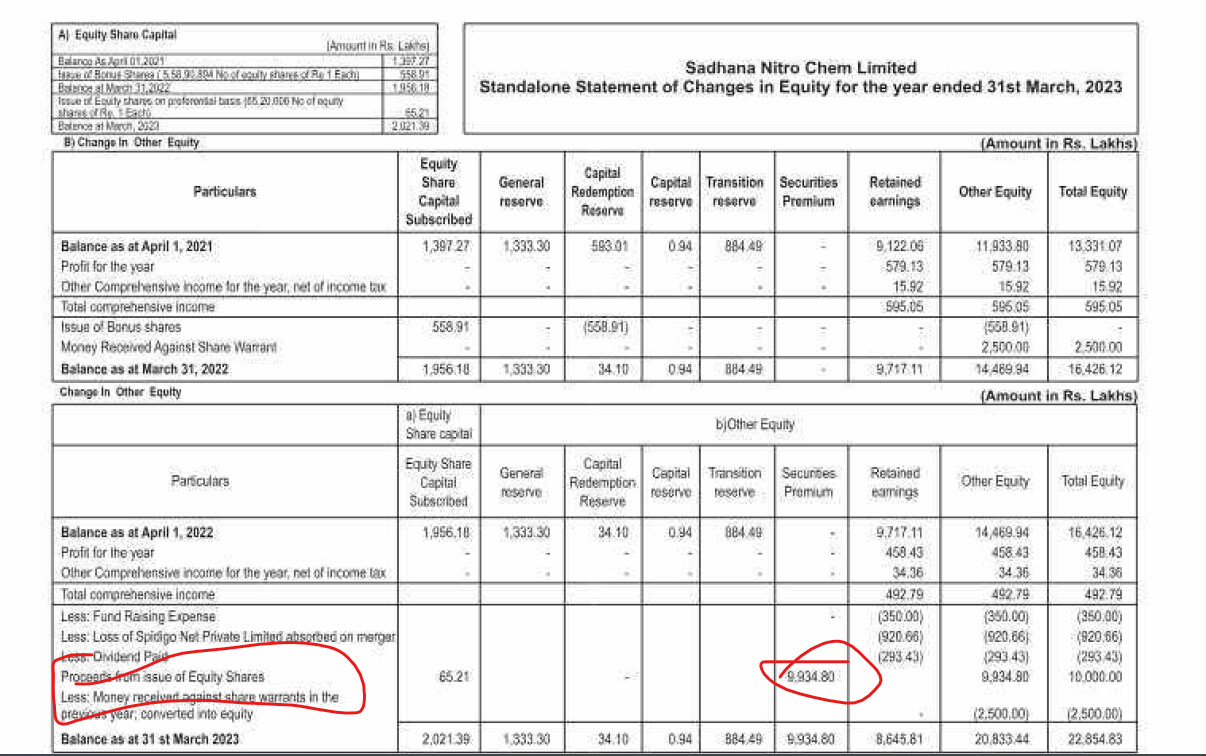

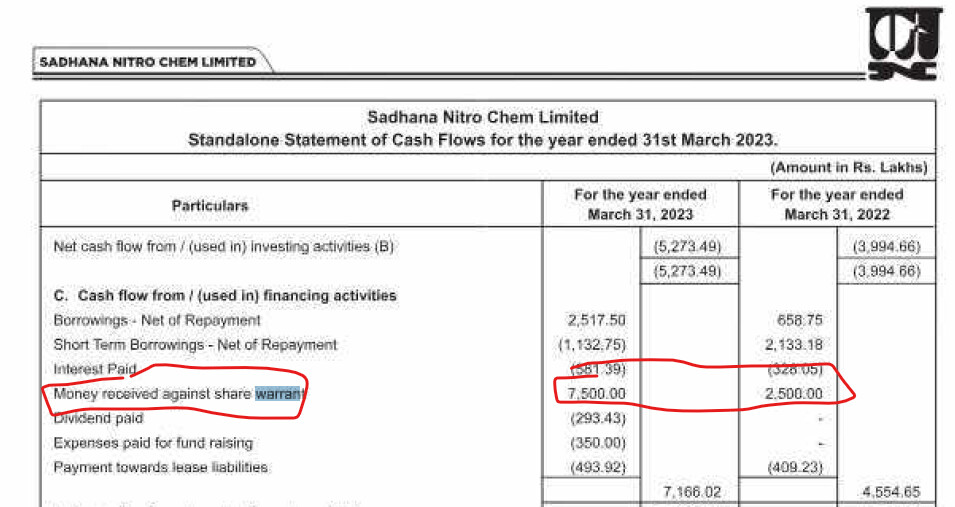

Sadhana nitro :a Dog or a Horse? (30-12-2023)

Actually, the entire warrant money has already been received during FY 23.

Ambika Cotton Mills (30-12-2023)

Disclosure ( No position)

Pros:

-

- Honest and ethical management maintaining best relations with all stakeholders like suppliers , customers etc. ( can be seen in numbers like low mngt remuneration, low costs and high margins)

-

- Management which knows what NOT to DO which is a rarity in corporate world especially NOT SEEN in textiles ( I worked in textile industry for 3.5 years)

-

- Technocrat management ( Mr.Chandran yes- no idea about next generation) is a huge plus in a commodity industry like textiles where very frequent changes in technology is common ( I have done many cost benefit analysis for new machinery as part of my job- But no one sees what is the actual benefit VS projected benefit). People buy machinery bcoz some competitor is buying and hence I also need to buy otherwise I cant match his price and hence my sales shall go down.

-

- Management with fixed customers ( read in one of the threads that they dont have a sales dept). Believe me, almost all textile cos have good sales teams with good salaries . This is commendable

-

- Own power – This can be huge problem in textiles and power cost is ever increasing and this shall increase more ( as govts are giving free power to poor and the same burden has to be shared by industry too ) and Buying exchange from exchanges can be huge ( I have done many adhoc analysis reg what should be max power purchase price for each factory) . This is going to reduce power cost and hence increase competitiveness of Ambika.

-

- Having a fixed product range ( only premium counts) is a huge plus in textiles. Entire workforce in various departments can deliver consistent work as they need not change settings in each stage of yarn manufacturing as and when product changes. If product mix changes frequently lot of wastage shall happen ( I have done lot of product mix analysis in textiles – no need for Ambika to waste time on these as their product mix is fixed)

- 7.Cash rich – As Best cotton can be bought during best time…This shall be huge plus qualitatively for sure …financially , most of the time its advantage unless the cotton price crash drastically in short time…And just to cover fixed costs, lot of kachra orders are run in case of debt ridden textile cos. So its a huge plus.

-

- Ability to charge premium rates – read in one of the post that they charge 2 to 3% premium pricing as their weaving breaks are less…This is a huge advantage as not just in weaving , due to faults in spinning , lot of wastage could happen at yarn dyeing/ fabric processing stage ( some faults could be known only in weaving, some only in yarn dyeing, some only in processing etc) …( done lot of wastage analysis during my job)…The more late the fault is known, more is wastage as they need to re manufacture the entire fabric and this eats a lot of time and premium orders , time is essence and if delayed orders could be cancelled or they need to be air lifted to meet deadline ( which increases cost like anything) …I have seen people devote exclusive spindles capacity for premium yarn going into premium fabrics …so stable quality is a huge huge plus and I dont think customers shall shift loyalties for few pennies here.