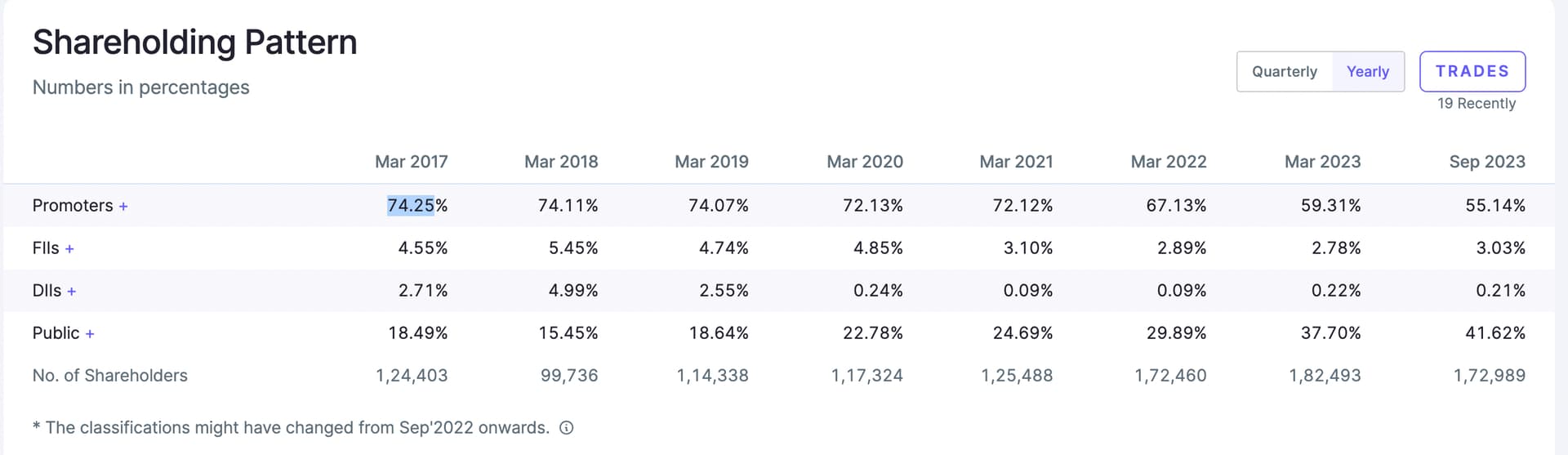

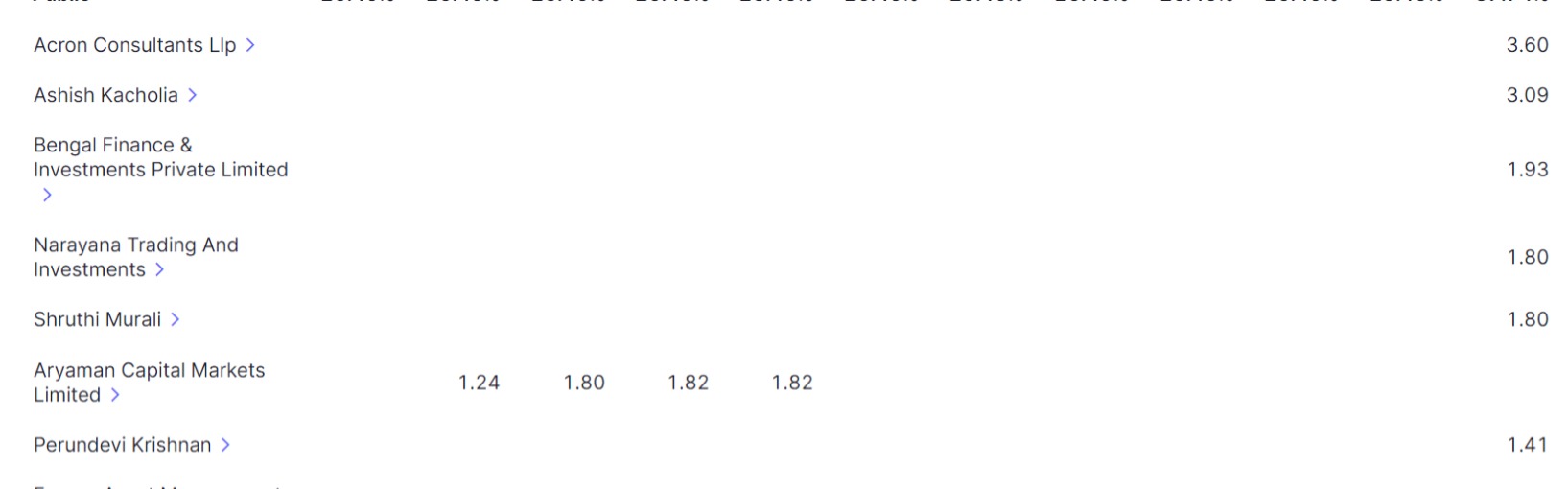

They had not sold. They issued warrants on Preferential Basis. Thats why decrease in holdings. Ashish Kacholia Sir is one of the allottees.

They had not sold. They issued warrants on Preferential Basis. Thats why decrease in holdings. Ashish Kacholia Sir is one of the allottees.

Hello Hitesh Ji,

I have been following your ideas for some time now and frankly I think your kind of investing/trading suits me. If I am not wrong, Your have mentioned that you identify 1. 52week high/ ATH Companies having consistent growth 2. Find favourable chart patterns 3. Look for volume and then take postions.

My specific question is how do you look at Volume ? Is it only though the plain and simple volume bars available at Tradingview ?

After certain analysis I am not able to decipher relevant data because generally during high trading days a lot of bulk deal happens and quite a few number of times I have seen operators have taken position and exited at the same instant/ day or within few days.(As available from Screener data). Fundamentally this doesn’t add up because one would want to hold till the rally lasts.

I would like to know the whole about volume analysis from a trader perspective who wants to ride the rally.

BTW… PE of china index is around 10 now

Have been holding Edelweiss greater china for 5 years now and bought a small quantity of axis greater china 1 year ago… day to day volatility of edelweiss is more but seems to capture the upside better… also as per morning star data the underlying JP.morgan china fund is tech heavy…

This assumes no asset addition on top of the 5 transmission lines they already have a 74% stake in.

Why do you think its not sustainable given the current assets. Where will the money leak? the price of transmission will escalate with inflation if it not already built into the pricing. Secondly, even if they dont escalate Rs 12 dividend looks steady unless management says so. Last quarter the management had to dig in about few paisa ( i believe they took 10-15 paisa from reserve to meet their stated Rs 3 per quarter goal). I dont think management is smart in quoting a yield ahead of time when so many variables could impact cost. They should instead talk about long term PPAs etc so that investors get visibility into future cashflows.

As i see it, its a good place to park cash and get 9-12% yield and if govt bond rates go down then this stock will rally as it provides a much higher yield. So if govt rates stay put u get paid a good yield but if govt rates fall u get capital appreciation too.

Management quality is good since these are PowerGrid guys with experience. Holding for 20-25% gain in capital while collecting 12% yield.

I didn’t understand why Priti’s margin should be less than its suppliers. Supplier is in a commodity business. Priti is selling finished goods b2b and b2c (online and retail outlets). Increase in B2C should only increase the overall margins.

What I see as a major differentiator between Priti and competitors is their ability to execute. Priti started in around 2007 and made its way in an area where differentiation is really difficult and where there were established players.

Also, handicraft products – They have handicraft products in their product mix. This segment is labour intensive and fixed assets are not required.

Rajasthan has a lot of companies which are in wooden handicraft business but most of them are not listed. Handicraft is a hit or miss business. Its about securing good buyers in Europe or America.

Both stocks are up about 35-50% from last discussion. No news but just market run up. Not the time to be greedy. Time to take profit and get on the sidelines till it falls down or if new news comes.

Why promotors are selling like crazy? Over the past 5yr the shareholding reduced from 75 to 55