Holding could be going up due to the merger and not due to secondary buying.

Posts in category Value Pickr

IDFC First Bank Limited (28-12-2023)

The attached news is very interesting. Seems like more buying to come in next few days.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (28-12-2023)

may be true… but mean reversion is also a possibility…as rates have reached peak and possible to go down in the coming quarters.

Maithan Alloys Ltd (28-12-2023)

The one positive I can see is that the companies they are investing in are good and the valuations are relatively reasonable.

But at the same time it seems like they are investing due to fomo. As if they wake up and realised that this 1000 cr of cash would have grown 1.5x in last 1-1.5 year (counting from time when the financial health of company was good after 2 years from COVID). Bad times come after good times in stock market. I hope they don’t overdo the investments.

Is China investible? (28-12-2023)

Chinese Real Estate Crisis and Extreme Covid lockdowns have hit consumer confidence hard and is yet to recover.

- Shrinking population: China’s population is shrinking for the first time in decades, leading to a smaller workforce and reduced domestic demand. This long-term trend will put pressure on economic growth potential.

- High youth unemployment: With a slowing economy and skill mismatch, youth unemployment is a major concern, reaching over 21% in June 2023 before the data was withdrawn. This raises social and economic risks.

- Geopolitical tensions: Trade disputes with the US and other countries add uncertainty to the economic outlook.

- Policy uncertainty: Government crackdowns on certain sectors and changes in regulations create anxiety for businesses and investors.

- Deflationary risks: Falling prices could lead to a vicious cycle of declining demand and investment, further hindering growth.

Could this be the Japanification moment for China?

Disc: Have a small exposure to China via Axis Greater China FoF

Vinati Organics (28-12-2023)

Few positive developments in this month

-

The company has commenced commercial production of Ortho Secondary Butyl Phenol (OSBP) and Di-Secondary Butyl Phenol (DSBP) w. e. f. 8th December, 2023. Vinati is the only manufacturer of OSBP and DSBP in India with an installed capacity of 5000 MT and 1000 MT respectively.

-

NCLT approval has been received for Amalgamation of Veeral Additives Private Limited with Vinati Organics Limited.

-

DGFT has imposed Anti dumping duty on import of Para tertiary butyl phenol (PTBP) from South Korea, Singapore, USA for a period of 5 years. Vinati is the only producer in the country with a capacity at 39000MT and it contributes ~17% of Vinati’s revenue.

While Vinati has a superb track record; stock has underperformed during last 2 years due to destocking of its key product ATBS by the customers and delay in completion of capex, which have impacted the earnings. Some positive developments have already happened during this month and more triggers (normalization of ATBS demand and commencement of new capacities/products) could be around the corner. If this happens, Vinati’s position can strengthen with a more diversified portfolio of specialty chemicals products apart from resumption of earnings growth.

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

Redington India : Strong Performance history, re-rating candidate (28-12-2023)

Redington – A business analysis, 28th Dec 2023

Background

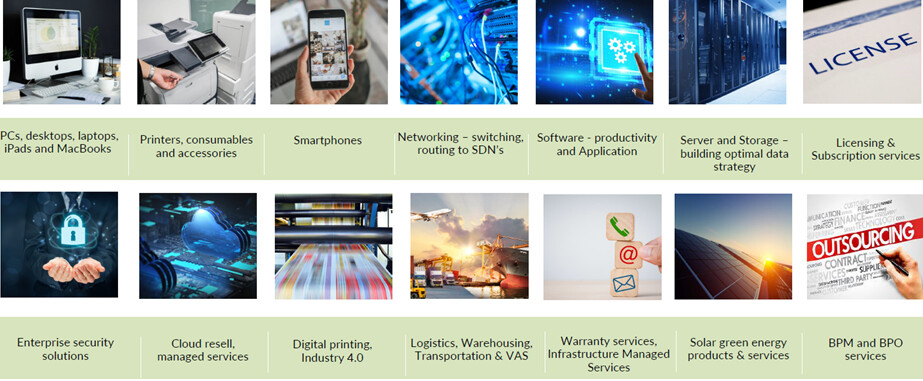

Make no mistake about it, superficially Reddington is just a middle man between IT manufacturers and customers, be it individuals (via retailers) or enterprises. Figure 1 shows the portfolio offerings of Reddington.

Figure 1: Portfolio of Redington across the IT spectrum (Q4FY23 Presentation).

As Figure 2 shows, the business is still dominated by the selling of standard IT equipment, PCs, printing supplies, networking equipment, servers, software and phones. There are a few new age verticals around cloud services and solar energy but these are small in relation to the total revenue. They might very well be good growth opportunities for the future though.

Figure 2: Clearly, ESG, TSG and MSG pillars dominate the business while the others are relatively small (Q4FY23 Presentation).

On closer inspection one realizes that Reddington is more than just a middle man – it is actually in the business of supply chain optimization for IT equipment. Why is that?

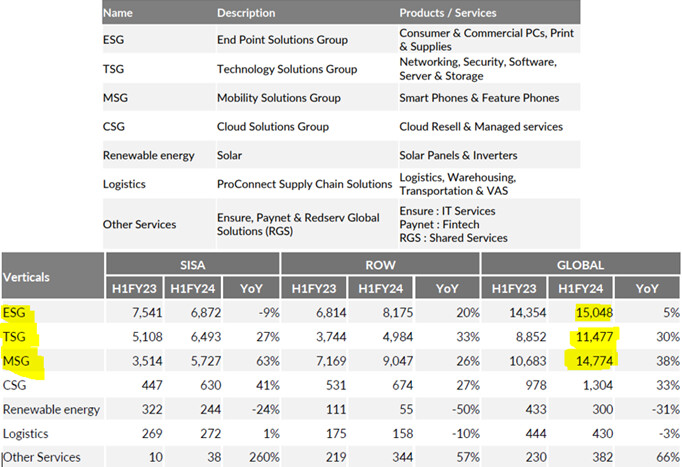

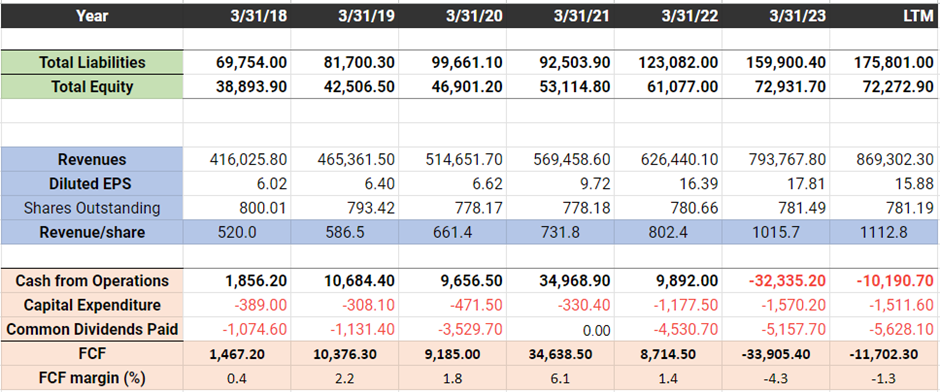

Well, it sells 300 brands (see Figure 3), across 38 countries (Figure 4) via 42,000 channel partners with a revenue of INR 869,000 million (US$ 10 Billion). Channel partners consist of Sub Distributors, Retailers, Large Format Retailers, Multi Brand Retailers, Branded Stores, Resellers, Corporate Resellers, Value Added Resellers, System Integrators, Independent Software Vendors (ISVs) and E-Commerce Players.

Half the business comes from SISA (Singapore, India, South Asia), the remaining from the ROW. The margins are wafer thin, just 1-2% (Figure 5). And across all geographies, Redington is the number 1 or 2 player. It’s the market leader in the Middle East and Africa while in India, it is a major distributor alongside its closest peer, Ingram Micro India Private Limited. The business quite literally revolves around supply chain optimization to maintain margins.

Figure 3: Reddington is the global middle man between the brands (300) and the channel partners (42000). For their solar business, banks, NBFCs may help with the financing.

Figure 4: Reddington is active in Africa, Middle East, India and SE Asia. A total of 38 countries.

It might also seem like a no-moat business. It certainly has no pricing power. The question is given enough money, who would like to compete for this business, one which operates on such low margins and at such a massive scale? Especially since efficiencies only start coming in once you reach scale. It’s a simple business but not an easy one. Good luck to a new entrant who wants part of the pie.

Business drivers

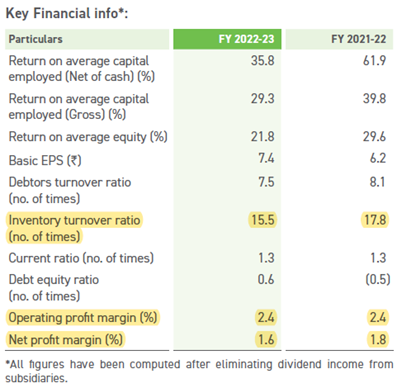

Risks don’t really come from competition, rather from the nature of the business itself. It’s a capital-intensive business because working capital includes huge inventory as a well as sales on credit. However, the inventory turnover ratio is >15, i.e., you refresh and sell you inventory 15 times per year (Figure 5). I don’t see much issue with inventory becoming redundant.

It’s also a business sensitive to global slowdowns since consumer and enterprise cash spend gets delayed by 6-12 months during recessions. That would affect Reddington’s numbers but these would only be temporary. You can postpone buying new IT equipment but not forever. Redington is geographically diversified so local recessions are not much of an issue.

Figure 5: High inventory turnover ratio and thin margins.

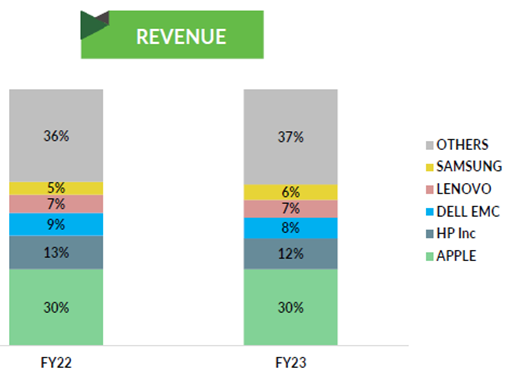

Figure 6: Top 5 vendors by revenue.

There is always a risk that one of the top vendors, say Apple can twist Reddington’s arm by playing of one middle man against the another. That’s just the nature of the business.

Analysis of Financial Statements

This is not a business to be analyzed based on yearly FCF or cash from operations since working capital changes can make these swing widely. EPS is a good metric. Based on Table 1, five-year growth rates for equity, EPS and revenue are all respectable. As Figure 7 shows ROICs are respectable between 15-20%. I can’t see this business maintaining an ROIC higher than 20% sustainably. As the business grows, working capital will grow, that’s inevitable.

Total current assets are very similar to total assets and these are comfortably higher than total current liabilities (which are very similar to total liabilities). Debt is very limited and a non-issue.

Table 1: Key metrics from financial statements in millions INR over the past five years.

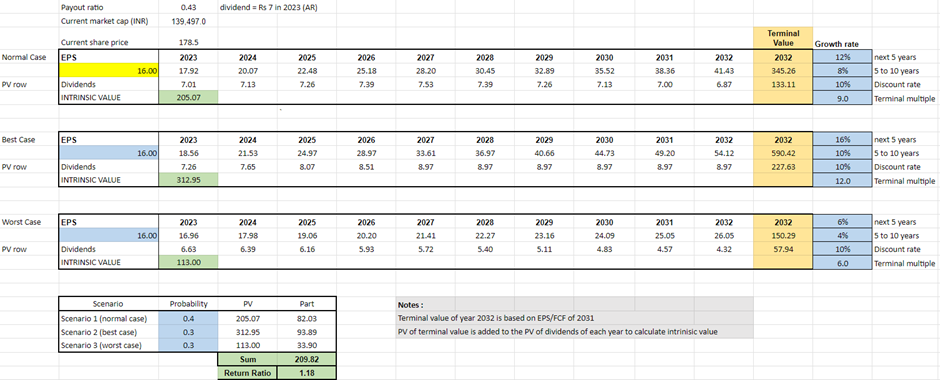

According to the annual report, the company is committed to paying 20-35% of PAT as dividend and will try to maintain or increase dividends every year. Valuing Redington on an EPS of INR 16, its currently priced for about a 12% return (Table 2). Realistically, 10 years down the line you can expect a 10-12% dividend yield on cost with the stock a double.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Figure 7: Historical trend of ROIC.

Investment thesis

A straightforward company to value that is in an essential but mediocre business. Not a business that you would expect is a multibagger, but slow, steady, predictable growth which every now and then would get derailed due to global slowdowns.

It’s a classic dividend buy. It will be hard to make money on the upside so buying it cheap is important. The tangible book value of INR 83 gives the absolute floor. If bought cheap, can be a good option to park money while one looks for better businesses. Certainly not a buy it and forget it kind of business if you want a compounded return higher than 10-15%.

Company news

Nothing noteworthy.

Catalyst

A couple of bad quarters can lower the price enough to give a good buying price. I would be interested at around INR 150.

Raman’s Portfolio – Review Appriciated (28-12-2023)

Hi Raman, may I know what is your current portfolio XIRR?

Thanks

Galaxy Bearings (28-12-2023)

Galaxy Bearings has neatly positioned itself among its peers (Timken, Shaeffer, NRB, SKP, Menon bearings) with respect to Net Asset turns, EBITDA margins and cash conversion days.

| Across 5 Yrs | Galaxy Bearings | Schaeffler India | Timken India | SKF India | NRB Bearings | Menon Bearings |

|---|---|---|---|---|---|---|

| Mcap (Cr) | 467 | 50,333 | 24,330 | 22,720 | 2,797 | 751 |

| PE | 25.8 | 54.6 | 67.9 | 47 | 25.6 | 25 |

| Gross M % | 50–55 | 38 | 40–47 | 40 | 60–65 | 60–65 |

| EBITDA M % | 15–20 (^) | 17–20 | 17-20 | 17 | 17 | 20–25 |

| Net M % | 13 (^) | 13 | 14 | 12 | 9 | 15 |

| ROE % | 16–23 (^) | 20 | 19 | 22.5 | 14.5 | 20–25 |

| Net Asset Turns | 9.92 (^) | 6.11 | 3.33 | 8–10 | 3 | 2.88 |

| Asset Turns | 1.23 | 1.2 | 1.1 | 1.35 | 0.88 | 1.2 |

| Rev Growth CAGR 3 yr % | 35 | 16 | 20 | 15 | 11 | 16 |

| EPS Growth CAGR 3 yr % | 42 | 33 | 17 | 26 | 47 | 31 |

| Cash Conversion Days | 102 (decreasing) | 66 | 124 | 69 | 292 | 121 |

Midcaps are valued 2x small-caps even with similar ROE’s. Most bearing companies are doing great post-covid with improving ROE’s. The growing manufacturing & automotive sector is providing impetus to the bearing industry.

I think Galaxy Bearings has comparable ROE’s, Gross margins & faster growth than the big players because Galaxy sells to other bearing makers, does aftermarket sales & services and mainly exports to other countries.

Few Questions:

- What is driving such profitability & growth for Galaxy?

- Do bearing manufacturers face raw material (steel) cost escalation (Raw material price risk)?

- What differences or advantages does the export market have over the domestic market, if there are any?

Galaxy Bearings has a huge 35 Cr capex for expanding bearing manufacturing capacity from 2.1 Mill/ Yr to 9.6 Mill/ Yr, a roughly 4.5x expansion, which shall be completed by early FY2025. Promoter has also been consistently increasing stake in the company. Most efficiency metrics are improving. Demand seems to be strong, as Schaeffler is also doing significant capex. Also, the stock has been in a long consolidation.

Disc: No position. Tracking.

Manappuram Finance (28-12-2023)

Muthoot commentary suggests uptick in smaller size gold loans. This can be a huge positive for Manappuram whose main market is small ticket gold loans.

Expect To Maintain Margin At 10% & Average Ticket Size Is In Rs 60,000-65,000 Range: Muthoot Finance

Disclosure: Invested in Manappuram (bought shares in last 30 days)