Key differentiators I found are backward integration and scaling up. Neuland is backward integrated and scaled up the API from tiny quantities to bigger ones, no information about others.

Key differentiators I found are backward integration and scaling up. Neuland is backward integrated and scaled up the API from tiny quantities to bigger ones, no information about others.

I am an HDFC customer it has one of the worst digital banking app and netbanking, I am very disappointed with their service even being an Imperia customer service is very bad, I also have a current account and LAP at HDFC, I have recently shifted to Kotak as my main banking app is very nice, their demat interface is also too good, I think as an investor in the past HDFC bank has delivered consistent performance is primarily I think due to its RM led model but nowadays atleast genz people have become smart and know that in the name of helping you manage your money they just want to sell ULIPs and insurance also HDFC bank is there in my society and I know the employees informally as well, they are very candid and are actually under a lot of pressure to meet targets, I personally think this consistency of the bank is because of its stringent targets to employees but in the end it just leads to mis-selling, if they use technology, they can be a much better bank which could keep its employees as well as its customers happy.

I like the bank’s strategy to open branches in rural areas but when it comes to digital banking it is still miles behind other banks.

The recent transaction between Karuna and BMS has given clarity on two fronts:

Very High probability of commercialisation of KArxt drug.

The entire valuation of Karuna is mainly derived out of Karxt drug and hence the current valuation gives a reasonable clarity on the broad total addressable market of Karxt drug.

In view of above we now have more clarity on Commercialisation and TAM of the KArxt drug.

The same has also been immediately factored in share price of Karuna post BMS transaction wherein more than 50% appreciation was observed in a single trading session of 22/12/2023 to factor in the acquisition cost.

Now since we have clarity on above two variables we need to work our on the potential revenue for Neuland from the KArxt drug as an API supplier.

As per Annual Report of Karuna:

For clinical supply, we use CMOs who act in accordance with the FDA’s good laboratory practices, or GLP, and current good manufacturing practices, cGMP, for the manufacture of drug substance and product. Currently, we contract with Neuland Laboratories Limited and Esteve Quimica, S.A., for the manufacture of xanomeline and source trospium from Procos, S.p.A. and Midas Pharmaceuticals, Inc.

The KARXT drug is combination of 2 API (Xanomeline & Tropsium) and Karuna has 2 different sources for each of the API.

While searching for API manufactures for Tropsium, names of following Pharam Company was reflected.

However, I was not able to find any manufacturers for Xanomeline. (Experts can throw light on this).

The ratio of Xanomeline and Tropsium in the formulation is roughly in the ratio of 1:4 i.e for making 1 KG of KArxt you will require 200 Grams of Tropsium and 800 Gram of Xanomeline and hence more revenue potential for manufacturers of Xanomeline API (as a layman calculation).

Further, as per Annual report Karuna :

It is our intent to identify and qualify additional manufacturers to provide active pharmaceutical ingredient and fill-and-finish services prior to submission of a new drug application to the FDA for any product candidates that complete clinical development.

So Karuna will obviously look for other manufacturers also for sourcing the 2 APIs.

Now from the above table it is evident that for Tropsium, there are various other manufactures, however for Xanomeline I couldn’t find any one.

So is the API manufacturing process for Xanomeline complex ?? , if yes then there is a natural entry barrier and Neuland is in a safe position.

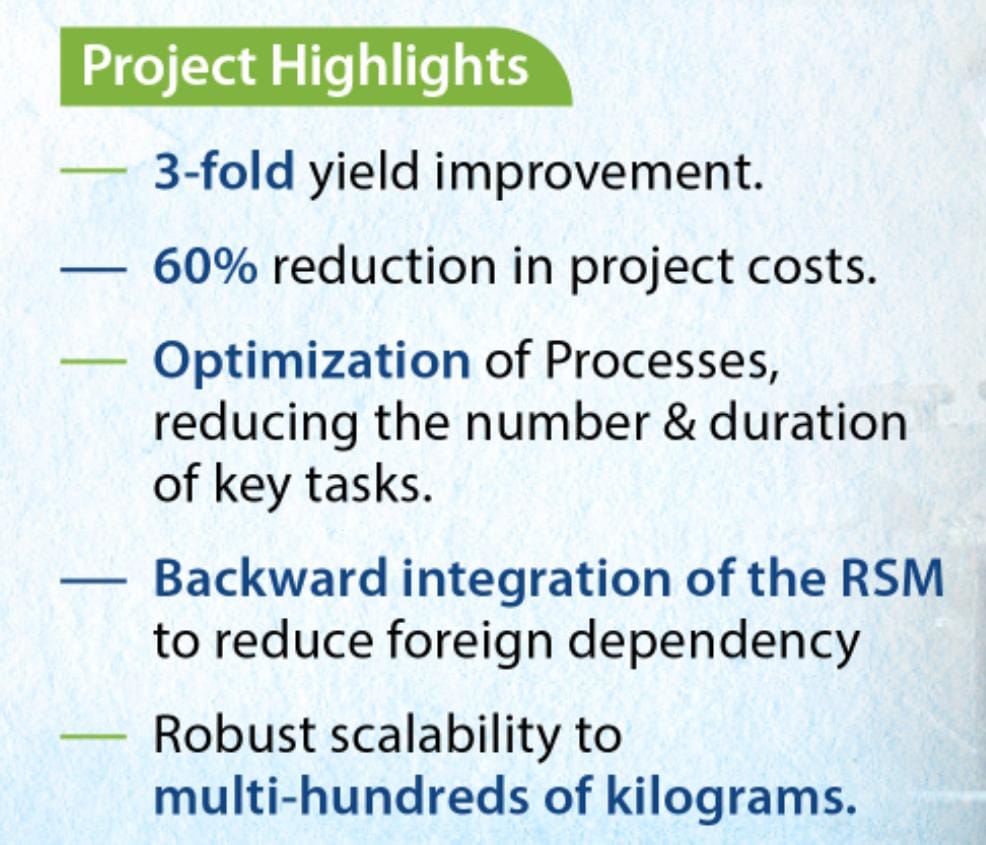

Further, we also need to analyse how sticky this business will be for Neuland or how sticky Neuland can make this business for itself. The following project highlight (for Xanomeline) published by Neuland reflects the capabilities of Neuland and also build a entry barrier for other manufactures even if the process is not complex. (similar to DIVIS Lab where they evolve their manufacturing process to become a lowest cost produce thereby creating a niche even in generic API)

So any new manufacturer which Karuna/ BMS will be looking for Xanomeline to replace Neuland will be required to have above capabilities along with proven track record. Further, the cost/compliance of shifting/ adding new API manufacturer(for Xanomeline) can also be a deterrent for Karuna/BMS.

https://www.chemanager-online.com/en/topics/pharma-biotech-processing/switching-api-sources

Karxt seems to be a blockbuster and a much awaited drug.

One can go through several reference article available on the internet to comprehend the requirement of this drug.

For reference one can also go through concal transcript of Karuna

KARUNA CONCAL.docx (70.0 KB)

Karuna Therapeutics, Inc. (NASDAQ:KRTX) Q3 2023 Earnings Call Transcript November 5, 2023

Neuland with the latest transaction seems to be elevated to a new orbit now.

Please help out for following questions:

Formulations/drug where Xanomeline is used as an API.

Manufactures of Xanomeline in India/World.

Is Manufacturing process of Xanomeline complex. ?

Disclosure : Invested and further added today and will further add in a SIP mode.

what are the reasons for the low PE multiple? Radico with flat growth now trades at nearly 100x TTM earnings.

https://www.screener.in/company/compare/?codes=3409,1273512

Currently Radhka Jeweltech operates in Rajkot with a single 2500 sq. ft. outlet, with more than 30 employees. The retail outlets stock a wide range of jewelry designs for both men and women. The company also provides value-added service of manufacturing custom-made products.

So, it is really small. I am looking at it to see if it has the potential to grow.

Thyrocare – A business analysis, 26th Dec 2023

Background

Thyrocare is largely in the business of blood tests. It is heavily tilted towards testing for disorders (blood constituents, hormones, electrolytes) rather than disease. Its business model is more B2B focused than B2C. Here B2B refers to hospitals, clinics, local collection centers that send their business to Thyrocare (often via franchisees). Typically, these other businesses collect the blood samples and Thyrocare processes it. See Figure 1 for revenue mix.

Figure 1: Most of Thyrocare’s revenue is from B2B, only 6% from B2C. Quarterly report, Oct 2023.

With PharmEasy acquiring a 70% stake in Thyrocare in 2021, the opportunity for exploiting synergies and getting more B2C business via PharmEasy portals does arise and this can be without much spending on customer acquisition and advertisement.

The business model is of the hub and spoke kind as shown in Figure 2. Samples are collected in 570 of the 779 districts in India. Samples requiring more complex tests are sent to the central and zonal labs, the others to proximal regional labs. This way equipment costs are centralized and utilization rates are high.

Figure 2: The hub and spoke model of Thyrocare.

If opportunities for growth are available, it can be done in a capital-light manner. All equipment is leased from the vendors and the lease costs go into opex. All reagents are purchased from the vendors but that does not require capex. Lab space can also be leased. So effectively this is a capital light business.

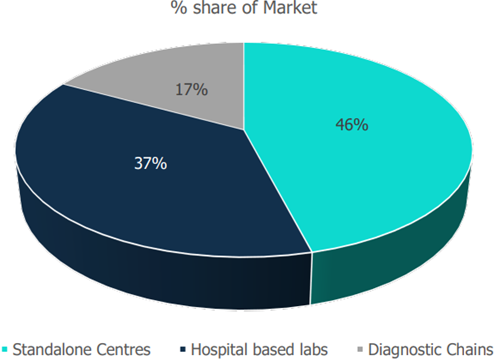

A good overview of the sector is given by HDFC securities in 2021 and Care Ratings in 2023. As shown in Figure 2, the market share of the organized diagnostics labs is only 17% of which the large pan-Indian entities only have a 6% market share. Like the other large organized players, Thyrocare has NABL certified labs (only 2% of the nation’s labs have this certification). Do note that there might be other certifications that still lend credibility and perhaps some of the other labs have such alternative ones. Long story short, amongst the organized players, accreditation is not a competitive advantage.

Figure 3: Market share of diagnostics providers

Thyrocare is also involved in providing PET-CT imaging labs but that’s only a small part of the business (7% revenue, 2023).

Business drivers

The most obvious business driver is that the entire sector will grow as GDP/capita increases. Add to it the fact that India will be the global epicenter of lifestyle diseases owing to poor diets and lack of exercise, sector growth is inevitable.

This entire business might go the way of retail, with margins and ROCE contracting due to competitive intensity owing to lack of entry barriers. This is excellent for the populace as costs go down, but identifying winners in the sector becomes very difficult. After all they are all using the same machines, doing the same tests and by and large offering similar services. Certainly, there are niches, such as Thyrocare being more into testing for disorders while Dr Lal’s Pathlabs offering more complex tests including disease testing.

Winners will be decided by good managerial practices. That’s what separates the Walmarts and Costcos from the rest. While the business is a value-add to society, nothing prevents commoditization of the diagnostics market. The unorganized sector will likely shrink, but amongst the big organized players, whether there will be a few dominant ones 10 years from now is hard to estimate.

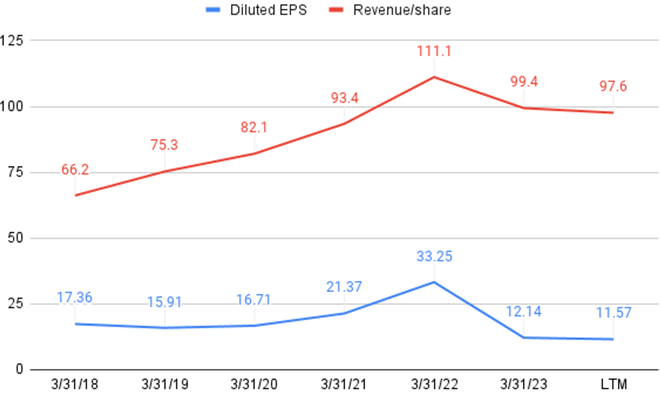

To me Figure 4 tells Thyrocare’s recent story. While revenue per share has shown decent growth (ignore the Covid pop), earnings have not grown proportionally. In fact, in the last 18 months, they are going down quite dramatically. This is a clear picture of a company without pricing power and without being able to leverage economies of scale.

Figure 4: Revenue and earnings per share over the past 5 years.

Analysis of Financial Statements

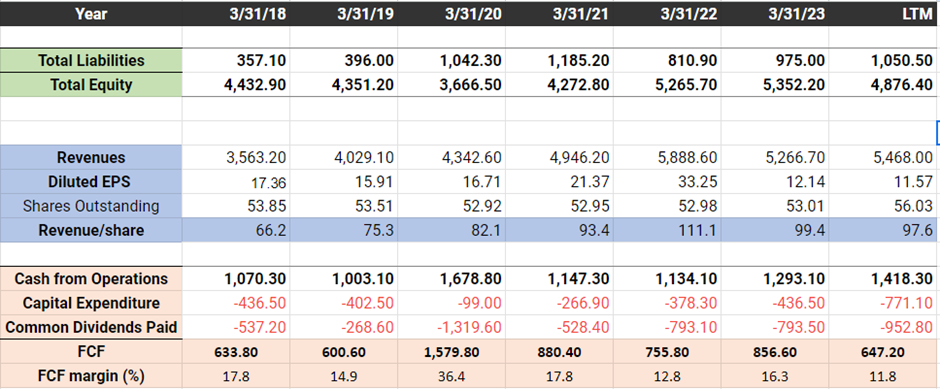

Two things stand out from Table 1 – all growth rates are anemic and practically all the FCF is being returned to shareholders as dividend. The average capex over the last 5 years is INR 400 million, of which 70% is maintenance (depreciation and amortization) while only 30% is being put into growth despite capital metrics being decent (Figure 5). And that’s the crux of the problem, they are unable to grow without destroying margins. For a cash rich company like Thyrocare, I find it surprising that they lease machines (don’t know the exact percentage) – unless you are growing rapidly, buying would be cheaper in the long run.

The recent increase in share count (approx. 6%) is something to keep an eye on. I don’t particularly care why they are doing it but shareholders should know that their stake is reduced by 6%.

Table 1: Key metrics from financial statements in millions INR over the past five years.

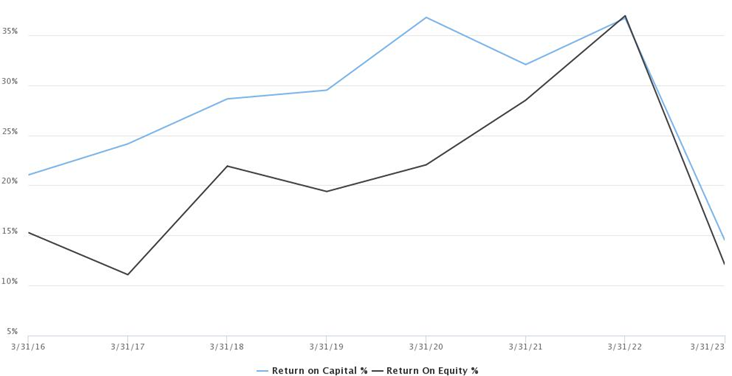

Figure 5: ROCE and ROE trend.

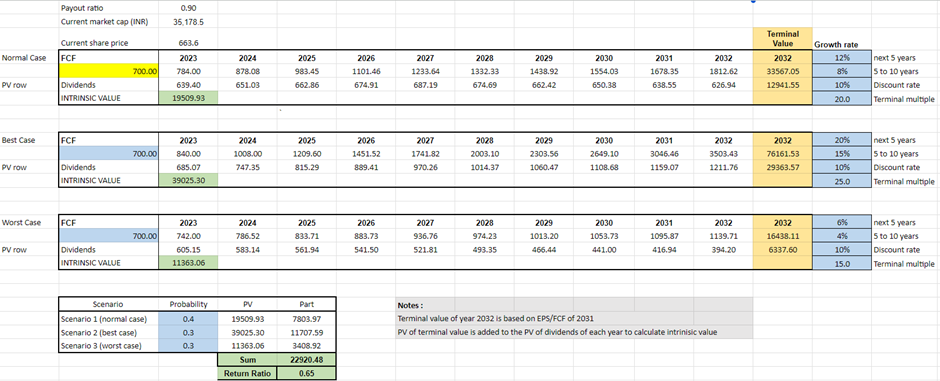

For valuation, I just use Thyrocare as a FCF engine. INR 700 million seems like a reasonable FCF number. 10 years out, the PE should contract. Given these assumptions the most likely case is that Thyrocare is priced at 6.5% return. Only in the most optimistic assumptions is it firmly valued for a 10% return.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

This is a decent company in a growing market. Competitive forces will likely make ROCE and margins go down, but nothing stops Thyrocare from being a reliable FCF engine. To me this would be more of a dividend buy with a modest 10% FCF growth. That being said, its priced to be a high growth company and the data does not support it. Astute management practices might prove me wrong and the business might meaningfully improve, but the data only shows deterioration. Not surprisingly, while the business makes 2.5 more money than in 2015-16, the price is still the same today in 2023! A 50% decrease from here wont surprise me too much.

Wake me up if the price foes down by half and the dividend approaches 5%.

Company news

A few minor developments on business expansion:

Thyrocare has also entered into government partnerships for the like of TB and infections, but this would only be a percentage or two of revenue (Concall Transcript, Oct 2023).

Also, Thyrocare has entered a JV in Tanzania and expressed interest to expand into East Africa and the Middle East.

Catalyst

The PharmEasy acquisition could have been a catalyst but that does not seem to have emerged. On the contrary, PharmEasy is so heavily in debt, they may just think of Thyrocare as a cash cow to service their debt. And if they struggle to service their debt, who knows what happens to the stock price if they unload their shares or sell it someone else. Either way, unless the business gets materially better, I don’t see a sustainable catalyst. Price action is of course unpredictable.

Disclosure: I had bought it relatively cheap as a hedge against further covid outbreaks (Thyrocare goes up, rest of the portfolio goes down). I sold out at a reasonable profit. Probably I had paid too much to buy it in the first place (even as a hedge) but Mr. Market was kind and absolved me of my sins.

What about 2023 numbers and growth? 2023 numbers went in an overbought situation.

If you look at the momentum ratio ranking for 6m and 12m, you will notice that the list is quite different.

Maybe the Z score is damping them when we consolidate both lists.

Not sure if there is any other way to combine two periods.

I am certain that there is never a bad time to start.

As you rightly observed, BSE is riding well and has a current allocation of 9.9%, while one of the new entrants has 3.58%.

I have been following SJS only recently but generally, mgmt seems to be over promising and under-delivering so far. They guided for 20-25% organic growth in F23 and missed it (blaming weak exports) and have once again guided for 20-25% organic growth in F24 (delivered 10% growth in H1 F24) while maintaining it despite weak H1.

Commentary continues to be strong though and WPI numbers should start improving from Dec-23 quarter. Based on my numbers, company can deliver peak revenue of 1000 Cr (assuming Exotech’s capacity expansion to 300 Cr topline goes through in C24) over the next 3 years with potential PAT of 145-150 Cr. Will have to wait and see.