Yes it is 2 paisa, charged from both buyer and seller each. This can come further as the power prices come down further. I dont think its too low.

Posts in category Value Pickr

ValuePickr Carolina (USA) (22-12-2023)

Hi.

Just wanted to ask how do you file your taxes for nre account. In USA. Thanks

TCM Ltd, microcap with large land holdings’ (22-12-2023)

TCM ltd is one of the oldest companies founded by Nobel Laureate Sir C.V.Raman and Dr. P. Krishnamurti in 1943 as Travancore Chemical Manufacturing Company Ltd. Name was changed to TCM Ltd in the year 1996.

TCM has multiple chemical manufacturing plants. They used to deal with Organic and inorganic chemicals, Fungicides, Herbicides, Barium and Strontium salts, Strontium Nitrite, Sodium Sulfide and various other derivatives. Due to financial constraints and scarcity of raw materials, company stopped production. TCM diversified its operations into Renewable Energy, Education, Healthcare etc. They have created new subsidiaries TCM Properties and TCM Solar.

Company is trying to monetize the land holdings. They have 100+ acres in Tamil Nadu and 21.6 acres in Kochi.

Through EGM, they have obtained approval for monetizing land holdings.

Link: https://www.tcmlimited.in/store/amn/NOTICE%20OF%20EGM%20-%2029th%20July%202022.pdf

Ulundupet Land: Approx 105 acres, this is free from encumbrance and with clear title. They have applied for exception under 37A and this land is free from encumbrance and with clear title.

Kalamasery Land: Total 21.6 acres. They have tied up with Asset Homes for joint development of 12.63 acres. Remaining 9.03 acres is yet to be decided.

Earlier, Godrej had earlier given interest free advance for 20 crores for joint development but this could not be implemented due to BIFR/ AAIFR proceedings.

The company, being now out of these proceedings, is trying to monetize the land.

TCM needs to refund this Godrej interest free amount, which company is currently doing. For raising funds they entered into MoU with Asset Homes who will be giving advance of 25 crores for settling Godrej deposit and other debt.

TCM has 21.6 acres in Kalamasery. Assuming rate of 10 per cent in Kalamaserry, 2160 cents (21.6 acres) land in Kalamaserry value will be Rs 216 crores vs mcap of 35 crores. Going rate near the land is 12-13 lakh per cent.

Mettur Land: 12.45 acres: This is mortgaged till Kalamaserry land is made charge free . As part of obtaining temporary loan from Asset Homes for clearing Godrej advance of Rs 19.67 crores, company has Mortagaged Mettur land with Asset Homes. After clearing Godrej deposit and removing charge from Registrar, this land will be free from mortgage.

Tuticorin land: This 7 acres land in Tamil Nadu is sold for Rs 3 crores.

Link: https://www.bseindia.com/xml-data/corpfiling/AttachHis/8c6da149-6a51-4215-a0f5-aa8d1cadbb0c.pdf

Promoter have hiked holding to 49.5% in Sep 2023 from 36.8% in March 2022.

Porinju’s family had previously exposure to this share. Porinju Veliyath buys stake in LIC-owned stock. Share hits upper circuit | Mint

Asset Homes MoU : BSEINDIA

TCM Ltd, micro cap with large land holdings (22-12-2023)

TCM ltd is one of the oldest companies founded by Nobel Laureate Sir C.V.Raman and Dr. P. Krishnamurti in 1943 as Travancore Chemical Manufacturing Company Ltd. Name was changed to TCM Ltd in the year 1996.

TCM has multiple chemical manufacturing plants. They used to deal with Organic and inorganic chemicals, Fungicides, Herbicides, Barium and Strontium salts, Strontium Nitrite, Sodium Sulfide and various other derivatives. Due to financial constraints and scarcity of raw materials, company stopped production. TCM diversified its operations into Renewable Energy, Education, Healthcare etc. They have created new subsidiaries TCM Properties and TCM Solar.

Company is trying to monetize the land holdings. They have 100+ acres in Tamil Nadu and 21.6 acres in Kochi.

Through EGM, they have obtained approval for monetizing land holdings.

Link: https://www.tcmlimited.in/store/amn/NOTICE%20OF%20EGM%20-%2029th%20July%202022.pdf

Ulundupet Land: Approx 105 acres, this is free from encumbrance and with clear title. They have applied for exception under 37A and this land is free from encumbrance and with clear title.

Kalamasery Land: Total 21.6 acres. They have tied up with Asset Homes for joint development of 12.63 acres. Remaining 9.03 acres is yet to be decided.

Earlier, Godrej had earlier given interest free advance for 20 crores for joint development but this could not be implemented due to BIFR/ AAIFR proceedings.

The company, being now out of these proceedings, is trying to monetize the land.

TCM needs to refund this Godrej interest free amount, which company is currently doing. For raising funds they entered into MoU with Asset Homes who will be giving advance of 25 crores for settling Godrej deposit and other debt.

TCM has 21.6 acres in Kalamasery. Assuming rate of 10 per cent in Kalamaserry, 2160 cents (21.6 acres) land in Kalamaserry value will be Rs 216 crores vs mcap of 35 crores. Going rate near the land is 12-13 lakh per cent.

Mettur Land: 12.45 acres: This is mortgaged till Kalamaserry land is made charge free . As part of obtaining temporary loan from Asset Homes for clearing Godrej advance of Rs 19.67 crores, company has Mortagaged Mettur land with Asset Homes. After clearing Godrej deposit and removing charge from Registrar, this land will be free from mortgage.

Tuticorin land: This 7 acres land in Tamil Nadu is sold for Rs 3 crores.

Link: https://www.bseindia.com/xml-data/corpfiling/AttachHis/8c6da149-6a51-4215-a0f5-aa8d1cadbb0c.pdf

Promoter have hiked holding to 49.5% in Sep 2023 from 36.8% in March 2022.

Porinju’s family had previously exposure to this share. Porinju Veliyath buys stake in LIC-owned stock. Share hits upper circuit | Mint

Asset Homes MoU : BSEINDIA

Markolines Pavement Technologies – Road to Riches? (22-12-2023)

Markolines Pavement Technologies Ltd

MCAP: 251 cr | PE: 15.7 | BV: 45 | Price: 131 | Promoter holding: 72%

Business

O&M provider for highways.

Highway Maintenance

- Asphalt overlay — Add a new layer of asphalt to increase lifespan.

- Crack sealing — Filling cracks

- Joint maintenance – repairing joints between concrete slabs.

- Drainage cleaning

Highway Repair

-

Routine repair – patching potholes, fixing minor cracks, any other issues

-

Cold in place recycling – Rejuvenating existing asphalt pavement by milling it, mixing it with rejuvenators, and repaving it, reducing waste and costs.

- Benefits – Reduced material usage, less waste generation, cost effective (low material usage, less transport cost, faster, longer lifespan, however costlier equipment). Higher quality repair. Versatile

-

Micro surfacing – Applying a thin layer of asphalt and polymer emulsion to improve skid resistance and pavement texture.

- Their PPT claims Markolines to be the first company which introduced this tech to india. I found this to be inaccurate.

-

M&R projects have a project period of 4 to 12 months.

-

Markolines does site analysis, creates camp for employees and then starts with the work.

-

H1 is impacted by monsoons. Continuous monsoon impacted H1Fy24. Impact on H1fy23 was lesser compared to h1fy24.

-

Margins should remain intact as they take contracts on a “cost plus” basis.

Tunneling

Tunnel construction in hilly areas. New segment.

Slightly higher margin as compared to maintenance and repair.

Larger and longer projects typically.

For the J & K tunnel project they have a stake of 25%. It’s a large project and multiple contractors are working on this.

Soil Stabilization

Part of road construction.

Soil stabilization involves treating and strengthening the soil beneath a road to improve its bearing capacity and prevent premature pavement failure. This can involve techniques like:

- Mechanical stabilization: Mixing the soil with aggregates or binders to improve its mechanical properties.

- Chemical stabilization: Adding chemicals like lime or cement to bind the soil particles and increase its strength.

- Reinforcement: Using geotextiles or grids to reinforce the soil and prevent erosion.

Performance Guarantee

- Markolines also provides 2 years defect liability (“warranty”).

- Markolines also provides a performance guarantee of 5%. i.e. Markolines will forfeit 5% of the contract value if their work quality isn’t acceptable. So far, this hasn’t happened as per concall Nov ’23.

Operations Geography

Mostly Maharasthra. Serves multiple other states.

One tunnel project in J & K.

Outsourcing of Contracts

Markolines also does outsourcing of orders if they can’t fulfill it themselves. The margins are slightly lower in this scenario for obvious reasons. The cost of this is reflected in other expenses. In house fulfillment of orders has the cost reflected in material consumed.

There are multiple ongoing litigations where Markoline had outsourced the contract but the contract receiver either didn’t pay back or didn’t complete the work. Source: Right issue document.

Government Involvement / Receivables Concern

- Markolines doesn’t directly deal with the government. Markolines gets orders from NHAI or private players. Markolines’s Management has repeatedly mentioned that they work very transparently with the clients

- As per the management they work with reputed private players and don’t expect that there will be bad receivables.

- They avoid direct contracts from NHAI because for government contracts there is a lot of interference, influences or local competition, and particularly, it goes on the cost basis.

Billing is done directly to the client on a monthly basis. Mobilization of machinery + initial setup takes 40 to 50 days => first billing happens in 70-90days

Reviews

- As per Mgmt, they are the preferred vendor and most of the InvITs as their offerings are more comprehensive than peers.

- Google maps rating of 4.4 (Doesn’t add value to the thesis. Had it been 2* would it have been a concern?)

Market

- Unquantifiable due to lack of data.

- Road construction companies operate in PPP and do the repair and maintenance themselves. Markolines is just a private player who offers O&M services if a private player of NHAI wants to outsource it.

- The equipment for road construction differs from what’s required for maintenance.

Competition

- The road construction companies have their in-house operations and maintenance arm.

- As per the Management this is a very fragmented industry and they are the largest players and they don’t see any large competitors.

Management

Vijay Oswal

Sanjay Patil

They have been versatile with the business they are in.

Remuneration

1.5cr total against 16 cr profit.

RPTs

They own 3 private related companies – . Markolines Infra Private Limited & Markolines Technologies Private Limited Unique

UHPC Markolines LLP (Associate) – (Markolines public has invested or loaned 8.3 cr into it. Markolines public got 0.2cr interest). Markolines public holds 50% stake in it.

No significant RPT between Marolines and these pvt companies.

Valuation

PE of 15. Mcap 257cr

Borrowing of 50cr, Payables 32, Receivables 108 → is quite high as compared to the net profit.

Order book is around 500 cr. ~170 of it is for the tunneling projects which take 1-2 years for completion. The remaining 330+ cr of it is for highway repair/maintenance.

My estimate for H2FY24 is 200cr revenue, 10% EBITDA margin. Expected FY24 PE to be 14.4

Thesis

- Fixed assets increased from 10 to 26cr in one year coupled with a larger order book of 400cr+. & low PE makes it attractive.

- Possibility of tailwinds, because highway construction has increased significantly since the past 5+ years and highway roads require maintenance after 5 years.

- Management expects very good growth (number not provided) for H2FY24.

- They have ventured into new businesses like Tunneling, Soil Stabilization, Full Depth Reclamation. They have good initial success in Tunneling.

- OTOH, why did they have to venture into multiple businesses instead of focusing on expanding on maintenance & repair?

Antithesis

- No visibility in TAM.

- Working capital intensive business with low EBITDA margins.

- Business is heavily influenced by external variables like the Government’s willingness to spend, regional politics & favoritism, monsoons.

Disclaimer: I hold no position in this company. Making this post to invite collaborators.

Malkd’s Core Portfolio (22-12-2023)

Dear Malcolm,

Was very hooked to your writing style and miss your views on current hype in equities.

How are you deputing your additional money these days and hope your business is also performing as per your expectations.

Seasoned investors have worth experiences and many a times help in building view for others.

Piramal Enterprises Ltd (22-12-2023)

Yes, Indiabull housing was in a special situation because of their promoters and other chunky repayments. Mr Ganga managed the situation well but market took down the stock price to 0.3 times of Book Value. I kept building position as I was sure on the long term story .I will not sell this stock in coming 3-5 years as I still feel it will double from these levels in that period. I am not putting fresh money now and watching story unfold with each passing quarter.

Co lending model has significantly derisked the company and they are building strong retail book. I expect them to start showing AUM growth from Q1 2024 and that would take it to its BV around 384 in 2 years time.

My views are personal and should not be considered as any advise as I can be and have been wrong many a times.

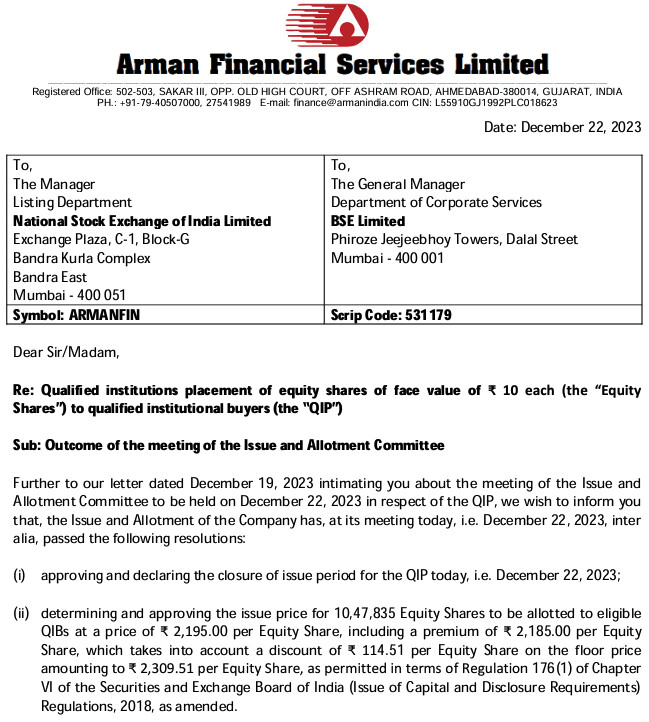

Arman Financial Services Ltd (22-12-2023)

Arman closed QIP raised 230 Crores

Time technoplast (22-12-2023)

Likely scenario after completion of restructuring and aftereffects :

| FY26 or 27 | |

|---|---|

| Sales | 4000 |

| OPM | 15% |

| Operating Profit | 600 |

| Other Income | 3 |

| Depreciation | 112 |

| Interest | 1 |

| Profit before tax | 490 |

| Tax | 26% |

| Net profit | 362.6 |

| 1.80% | |

| Maintenance capex | 72 |

| Owners earnings | 402.6 |

While this is not going to be exact, but it is showing us an approximate picture,

- Interest expenses will go down close to zero as company will pay off entire debt, so interest expenses of nearly 100cr will go to zero and entire amount of this money will flow towards bottom line through tax expenses.

- Depreciation will reduce proportionately to sale of foreign assets, so that amount will also flow towards bottom line.

- As share of value added product will rise, margins are going to increase, while I have used 15% , potential is over & above that.

- This company is struggling for growth capital from many years and main reason for that was demand of maintenance capex from the established products or commodity products, company was generating around 200 to 250cr owners earnings in recent years and out of it around 100 to 120cr were maintenance capex requirements for the next year. Again much of the remaining money was going into working capital, so they only had a growth capital of less than 100cr from internal generation every year.

Now this scenario going to change, with the owners earning of 400cr in FY26 or 27, much of this money will flow towards growth capex as maintenance capex requirements will reduce and NFAT is going to increase and working capital requirement will reduce, so company can grow much faster in future from internal accruals. - My average buy price is Rs38.xx, so if they pay dividend of 10-12% of net profit as they are doing since many years, my dividend yield will be around 4.5%

- ROE & ROCE are going to improve substantially.

As company will be able to grow from the internal accruals in the future, with share of value added products increasing constantly, will be net debt free, with higher ROCE and future perception of market participants towards high growth LPG, CNG & Hydrogen cylinder business this company can trade at any PE from 20 to 50, I don’t know.

I bought this business in 2019 & 20 at Rs38 mainly because it was exceptionally cheap at future PE of 2, I had no intentions to hold it above 150 but with passing year story constantly evolved positively. promoters started acting rationally, they tried to repair their past sin’s, and their composite cylinder business is too good to have. With its fast growth capability after restructuring at current price it may be trading at future 5yr PE of 6 who knows.

I sold some quantity at 135 and I regret my decision, I still hold substantial quantity and do not intent to sell it anytime soon. because market is all about future, and as business is getting better & stronger with each passing year I don’t see much possibility to losing money.

Risks: Restructuring doesn’t go as planned, Promoters again start acting irrationally which is rare possibility.

Note: Not a SEBI registered analyst, do your due diligence before buying, only sharing my thought on business and I may be biased.

Time technoplast (22-12-2023)

Likely scenario after completion of restructuring and aftereffects :

| FY26 or 27 | |

|---|---|

| Sales | 4000 |

| OPM | 15% |

| Operating Profit | 600 |

| Other Income | 3 |

| Depreciation | 112 |

| Interest | 1 |

| Profit before tax | 490 |

| Tax | 26% |

| Net profit | 362.6 |

| 1.80% | |

| Maintenance capex | 72 |

| Owners earnings | 402.6 |

While this is not going to be exact, but it is showing us an approximate picture,

- Interest expenses will go down close to zero as company will pay off entire debt, so interest expenses of nearly 100cr will go to zero and entire amount of this money will flow towards bottom line through tax expenses.

- Depreciation will reduce proportionately to sale of foreign assets, so that amount will also flow towards bottom line.

- As share of value added product will rise, margins are going to increase, while I have used 15% , potential is over & above that.

- This company is struggling for growth capital from many years and main reason for that was demand of maintenance capex from the established products or commodity products, company was generating around 200 to 250cr owners earnings in recent years and out of it around 100 to 120cr were maintenance capex requirements for the next year. Again much of the remaining money was going into working capital, so they only had a growth capital of less than 100cr from internal generation every year.

Now this scenario going to change, with the owners earning of 400cr in FY26 or 27, much of this money will flow towards growth capex as maintenance capex requirements will reduce and NFAT is going to increase and working capital requirement will reduce, so company can grow much faster in future from internal accruals. - My average buy price is Rs38.xx, so if they pay dividend of 10-12% of net profit as they are doing since many years, my dividend yield will be around 4.5%

- ROE & ROCE are going to improve substantially.

As company will be able to grow from the internal accruals in the future, with share of value added products increasing constantly, will be net debt free, with higher ROCE and future perception of market participants towards high growth LPG, CNG & Hydrogen cylinder business this company can trade at any PE from 20 to 50, I don’t know.

I bought this business in 2019 & 20 at Rs38 mainly because it was exceptionally cheap at future PE of 2, I had no intentions to hold it above 150 but with passing year story constantly evolved positively. promoters started acting rationally, they tried to repair their past sin’s, and their composite cylinder business is too good to have. With its fast growth capability after restructuring at current price it may be trading at future 5yr PE of 6 who knows.

I sold some quantity at 135 and I regret my decision, I still hold substantial quantity and do not intent to sell it anytime soon. because market is all about future, and as business is getting better & stronger with each passing year I don’t see much possibility to losing money.

Risks: Restructuring doesn’t go as planned, Promoters again start acting irrationally which is rare possibility.

Note: Not a SEBI registered analyst, do your due diligence before buying, only sharing my thought on business and I may be biased.