How to find proxy business using any tool like screener,Tijori ,Trendlyne etc. ?

Posts in category Value Pickr

Great articles to read on the web (16-12-2023)

Not related to investing.

Deepak Fertilizers and Petrochemicals (16-12-2023)

While going through company website, surprisingly, company has Creaticity Mall

in Pune (https://www.creaticity.co.in/) . Why company is in non-core business? – any one has any idea / more information about it?

Based on reported result – normally this business always reports losses!

Shree Ganesh Remedies Limited (SGRL) – A pioneer in API intermediaries and Specialty chemicals? (16-12-2023)

About company:

-

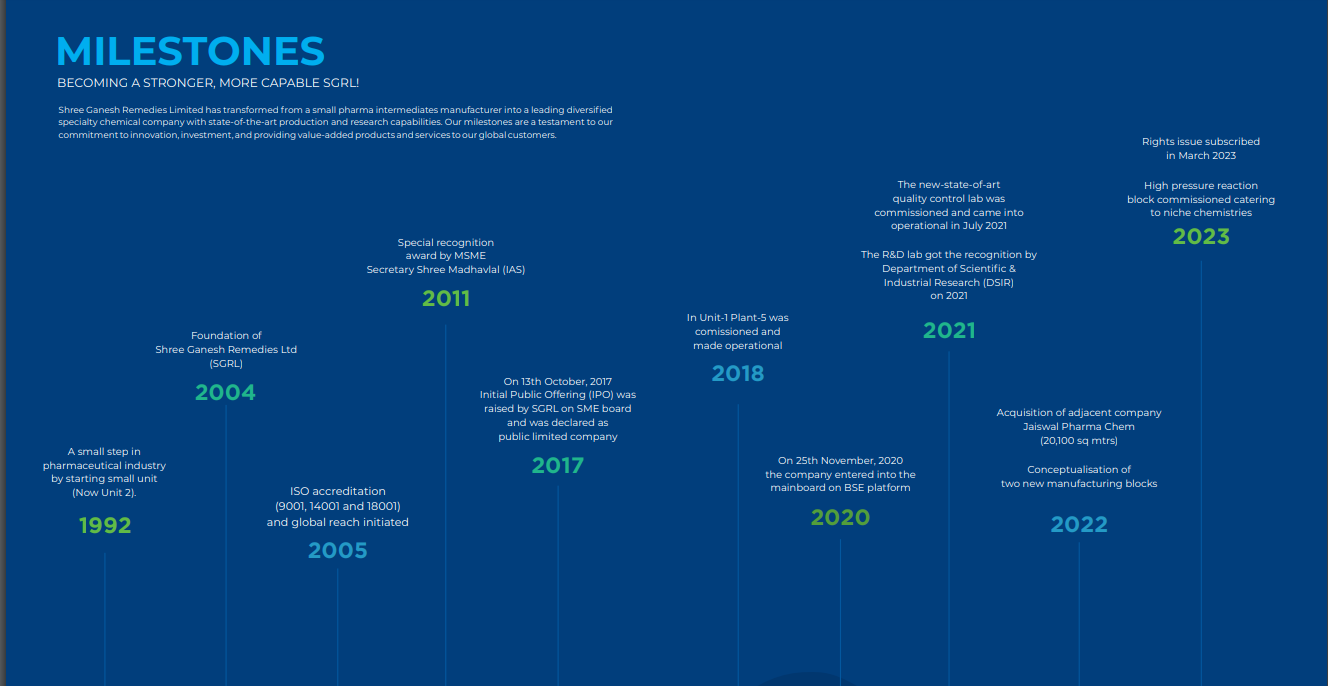

Started as a small pharma company in 1992 and later Chandu Kothia, chairman & MD founded Shree Ganesh Remedies in 2004. Company has two decades of experience in the pharmaceutical sector, and is one of the leading manufacturers of Pharmaceutical Intermediates and Fine & Speciality Chemicals in India.

-

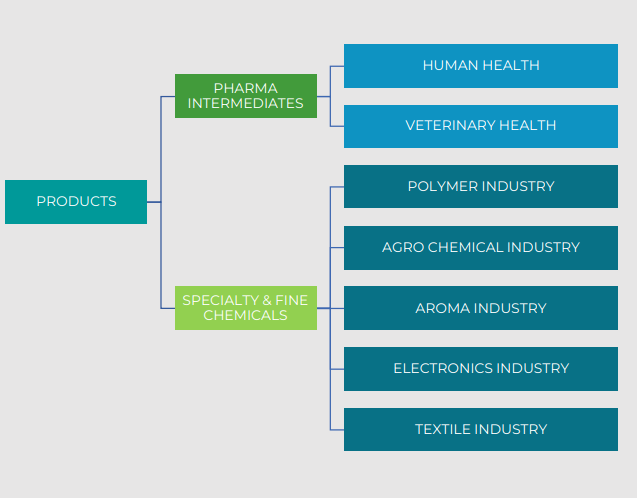

Its products find application in multiple industries including pharmaceutical, polymers, agrochemicals, electronics, aroma industry and many others.

-

It’s a family run business as father and both sons are fully involved in the business operations.

Manufacturing facilities:

-

Company has two manufacturing plants in Ankaleshwar, GIDC Gujarat and both of them are located close proximity to each other.

-

They have a total of 10 production blocks (2 of them are upcoming).

-

Unit-1 production area : 3,76,000 sft

-

Unit-2 production area : 36,500 sft

-

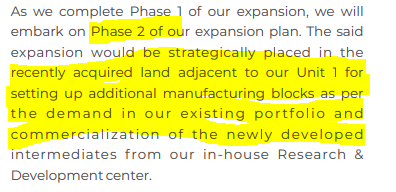

In addition to these plants, they also recently acquired the adjoining company with land area of ~2,15,000 sft which is now merged and this will be used for future expansion.

Business segments:

- Company is mainly into three different verticals:

- Human health API intermediaries

- Veterinary API intermediaries

- Specialty and fine chemicals

-

They have a 40+ product portfolio, 32 in API intermediaries and 11 in specialty chemicals. 4 of their products have more than 50% market share.

-

Clients spread in more than 15 countries. They want to focus on niche chemistries and provide the best possible solutions to their customers.

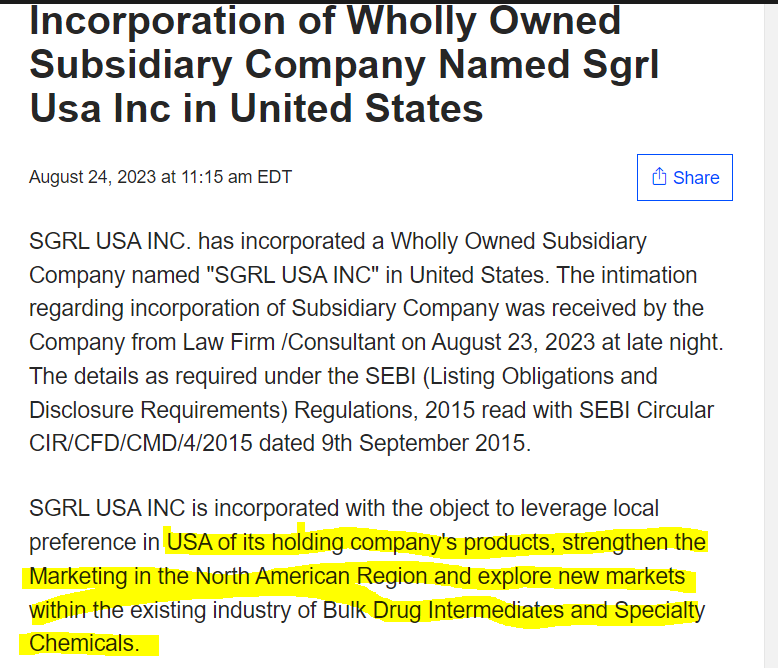

- Company also started a subsidiary in the USA to strengthen marketing there.

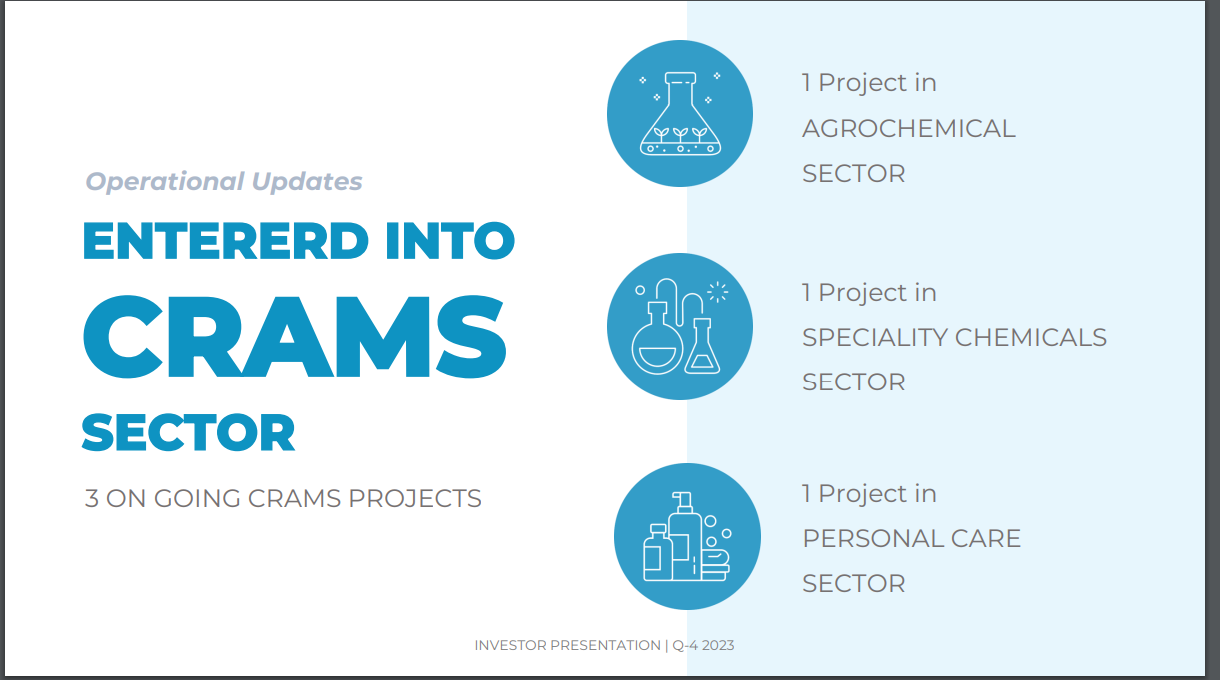

- They also entered into contract manufacturing with some of the Europe clients and one of the projects is already producing revenues from last quarter. Currently they have 3 ongoing projects.

Research & Technology:

-

Company believes in Research & Technology is the way to sustainable growth and has recently opened a dedicated facility for R&T. Focus of the R & T team is to develop not only new products but also focus on improving existing processes. In future they want to get into more sub segments of specialty chemicals to attract more clients.

-

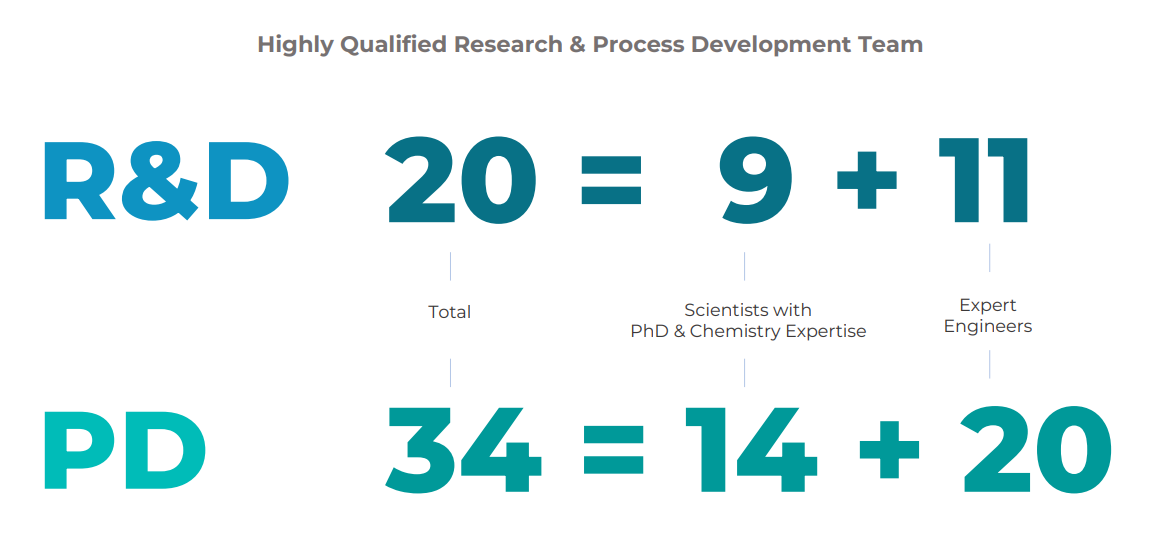

More than 50 people are working in research & process development.

-

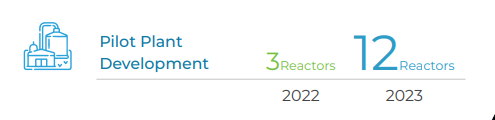

A new pilot plant has been set up and commenced operations to reduce the overall process and development time. The best practices from here will be shared to commercial sites for faster production, better lead times, and better utilization of the capacity.

-

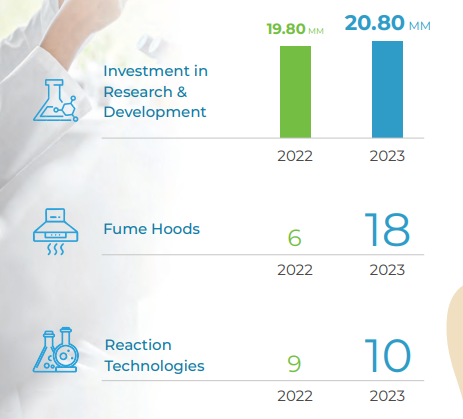

As you can see there is a 3 fold increase in fume hoods from 2022 to 2023.

-

They are spending around 3-4% of revenue in R & D from the last few years.

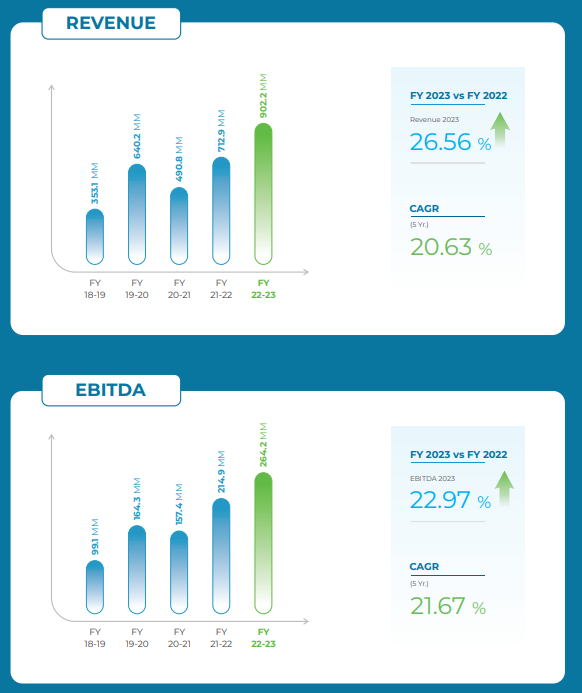

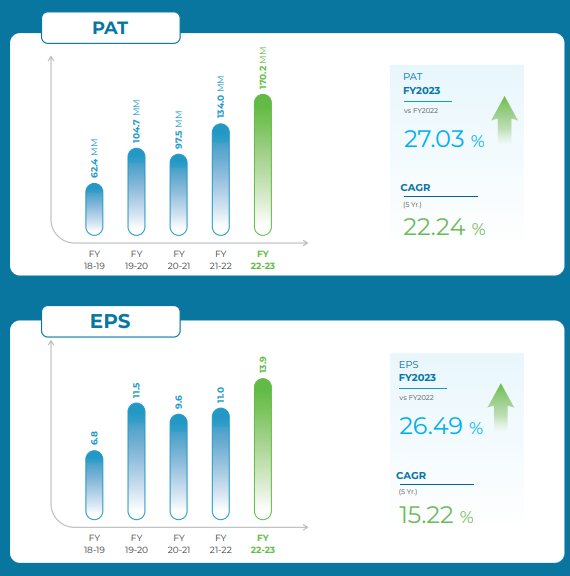

Revenues:

- Revenue:

- H1FY24 : 60 crores vs H1FY23 39 crores

- EBITDA

- H1FY24: 17.5 crores(29%) vs H1FY23: 11 crores(28%)

- Net profit:

- H1FY24: 11.3 crores vs H1FY23 6.8 crores.

- Company has been able to increase revenues consistently over the years.

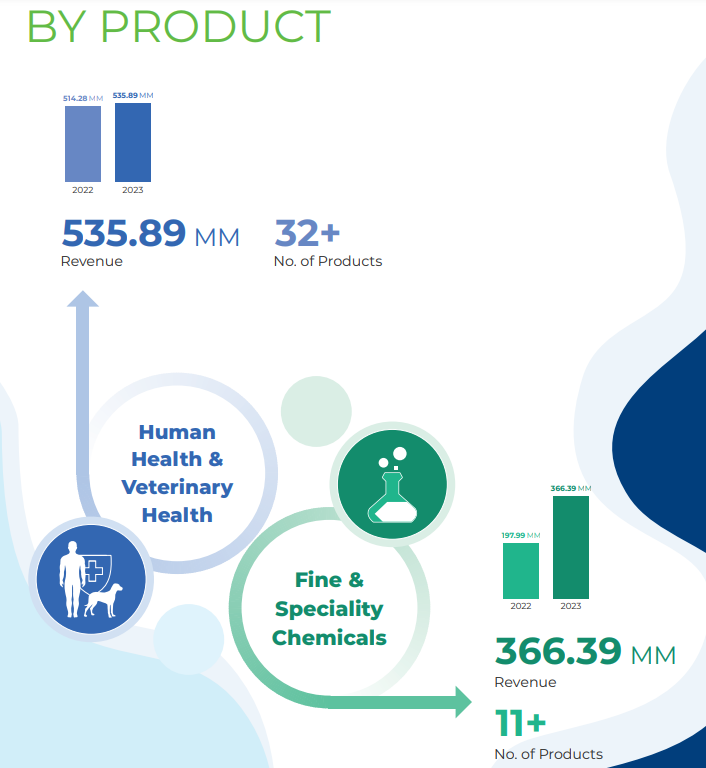

Revenue distribution:

- API intermediaries vs specialty chemicals: 59.3% vs 40.7% (FY23)

- Exports vs Domestic: 68.5% vs 31.5% (FY23)

Capex:

- Company has spent more than 40 crores in FY23 for acquiring the land adjacent to unit-1, setting up a new R & T block & pilot plant etc. This is by far the highest capex spent in the history of the company. Company expects to spend 15 crores for FY24.

Clients:

- Some of their marquee client list includes:

Management:

- Mr. Chandu Kothia who is the chairman & MD of the company has more than 30 years of industry experience. He started Ashoka pharma in early 90s and later in 2004 started Shree Ganesh Remedies to cater to international clients and to expand business further. HIs educational background is in chemistry and he started involving both of his sons into business. Both of them also pursued masters in chemicals.

- Gunjan Kothia thinks that the company has just started talked about the future prospects in the FY23 annual report (taken as is):

-

We are setting up a new GMP manufacturing block designed to cater to advanced API Intermediates, reinforcing our commitment to delivering high quality pharmaceutical solutions to our valued customers. This world-class facility is built in with the flexibility to manufacture in-house APIs which is further under strategic evaluation. We expect this facility to commence operations in the second half of FY24.

-

We have invested in an advanced manufacturing block dedicated to high-pressure reactions enhancing our pressure handling capacity up to 600 psi. This facility will allow us to widen our product range to better cater to our customers, amplifying our business horizon appreciably. With the commissioning of this facility, we will be one of the few players in our business space, with this capability placing us in a niche position in our business space.

-

We are setting up a cutting-edge Pilot Block, which will facilitate scaling up complex processes and optimization for the manufacturing processes. In addition, it will also serve as a commercial manufacturing block for small volume high-value products. When commissioned, the unit will provide the much-needed capacity and flexibility in our infrastructure to cater to high-value products. The unit should be operational in Q2 FY-24.

-

We have set up a new R&D block that houses the latest equipment and cutting-edge technology, allowing us to conduct advanced research and deliver complex, high-quality products. This investment is testimony of our commitment to fostering innovation and supporting the Pharma and Specialty Chemicals manufacturers in the US and the EU to reduce their dependence on China.

Shareholding:

- Promoters currently holding about 69.33% and total number of shareholders are also at about 7730 (relatively new listed company, came to main board in 2020).

Coverage:

-

There is not much coverage about the company in public and a handful of people in twitter talk about this company:

- https://twitter.com/theHarshFolio/status/1649009766931505152 : This is by Harsh who is very active in valuepickr. His writings has inspired me to start being active.

- https://twitter.com/raghavwadhwa/status/1724713331544526918

- Smart sync services covering this as their 5 minutes stock idea: https://twitter.com/SmartSyncServ/status/1735685176552796514

- I found a couple of videos from youtube covering this:

-

Recently Mittal analytics met the management and I don’t know if they have taken a position in it or not.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/9a372c29-6cd0-47d0-a2b4-aac7355ec143.pdf -

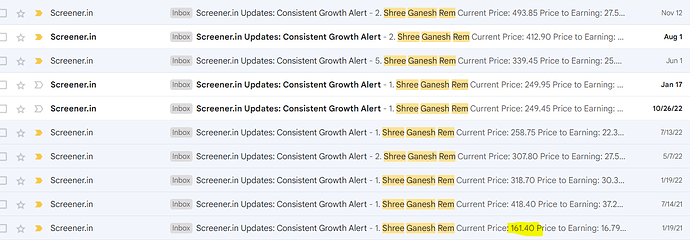

Interestingly this company came to my watchlist in one of my screeners during Jan 2021 when the price was around 160 and it continues to be part of the list multiple times since then.

What I have not covered in this:

- I haven’t gone through their chemistry processes and technologies, the company website has listed them. I am into computer science engineering and don’t have much understanding of organic chemistry.

-

I haven’t talked much on risks, I definitely feel there is a risk in raw materials procurement. It will be great if someone highlights the risks of the company.

-

I haven’t done a deep dive into financials, I would like to do it as and when I understand more about business.

-

I haven’t talked much on the management outlook and opportunities for the company, FY23 annual report covers this and I can update in the coming days about the same.

-

Scuttlebutt from EPFO website to get a feeling of salaries and increments, number of employee etc. I will be doing that in coming days.

References:

- FY23 Annual report: https://www.bseindia.com/xml-data/corpfiling/AttachHis/da3c26fa-3475-40b1-a0de-ecff2eb2b2b1.pdf

- FY22 Anuual report: https://www.bseindia.com/bseplus/AnnualReport/540737/76239540737.pdf

- Couple of presentations from the company to the exchange: https://www.ganeshremedies.com/investor/Q4-FY23-Investors-Presentation_revised-Final-.pdf

https://www.ganeshremedies.com/investor/INVESTORS-PRESENTATION_2020-21.pdf - About promoter1

- About promoter2

- https://www.linkedin.com/in/gunjankothia/

{kind=link}

Disclosure:

-

After being a passive observer for several years I started being active in the forum again and started writing recently on this forum. This is my first post on the stock idea and would like to build upon the initial post by discussing with other folks and ready to learn from other people in the forum.

-

Started buying after Q2 results and will continue to buy in the upcoming days as business evolves and I get more confidence in the business.

Petronet LNG Limited – Green India with Clean Fuel (16-12-2023)

Petronet – A business analysis

Background

As of 2023, Petronet is a simple business. It has two port-based LNG regasification terminals in Dahej and in Kochi, with current capacity of 17.5 and 5 MMTPA respectively. Petronet has long-term contracts with several suppliers like Qatar (7.5MMTPA) and MARC (1.425 MMTPA – an Exxon branch), as well long-term contracts with customers like IOCL, BPCL, GAIL etc. (8.25MMTPA). This part of the business is like a utility business and is not sensitive to LNG prices, since it is pass through at (pre)negotiated rates. A smaller part of the business also buys LNG on the international spot market and sells it to customers, like the fertilizer industry, that are price sensitive and will swap LNG for alternative fuels like coal if LNG is too pricey. This part of the business is like a commodity business and also has inventory risk.

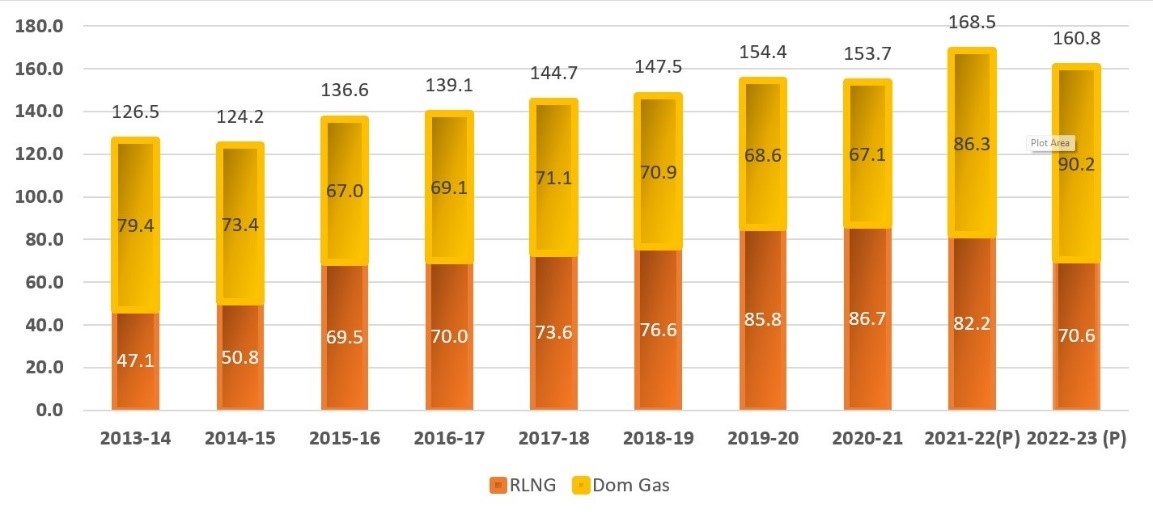

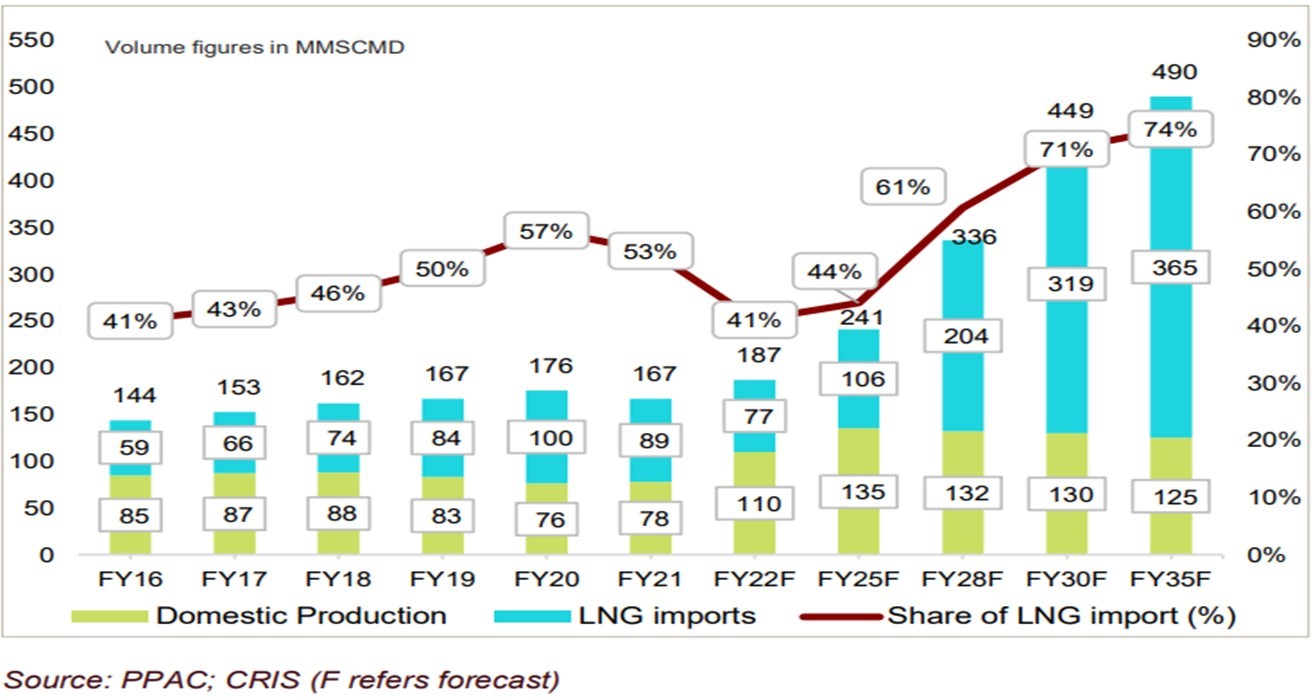

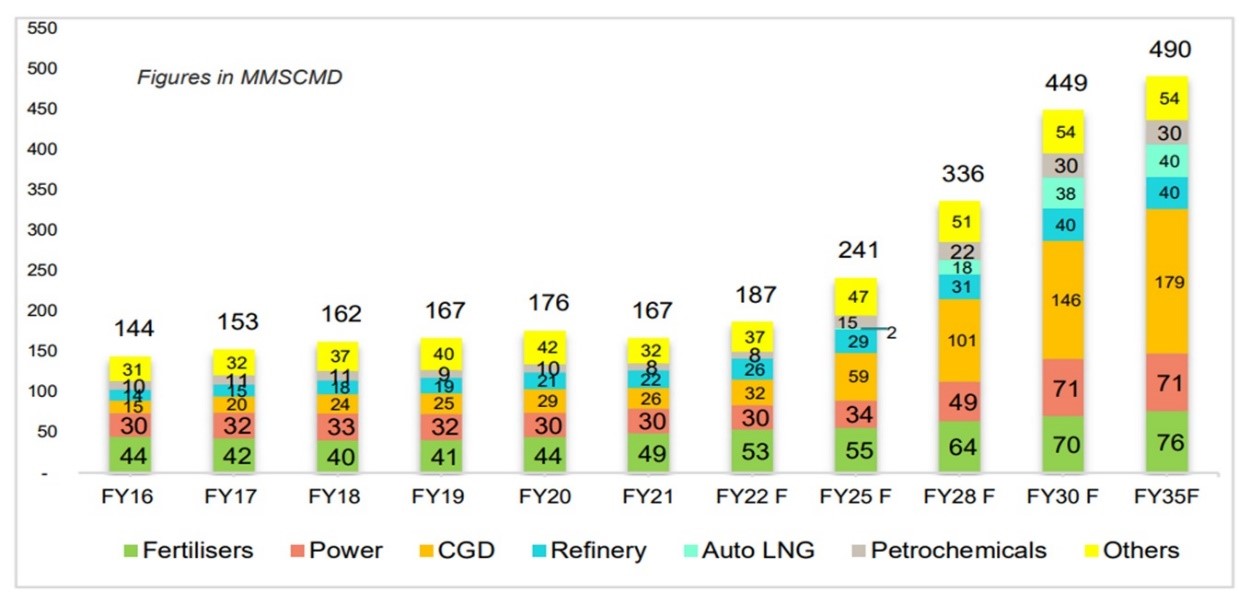

In the CY 2022, India had long term LNG contracts of almost 20 MMTPA, which constitutes approximately 95% of around 21 MMTPA LNG consumption (Annual Report 2023). Since India is a gas deficit country and relies heavily on LNG imports, Regasification Terminals play an important role in the country’s gas development plans. The share of LNG in India’s gas consumption stood at around 44% in the FY 2022-23. See Figure 1, Figure 2 Figure 3 for more details.

Figure 1: Gas consumption in MMSCMPD (to convert to MMTPA, divide by 3.6).

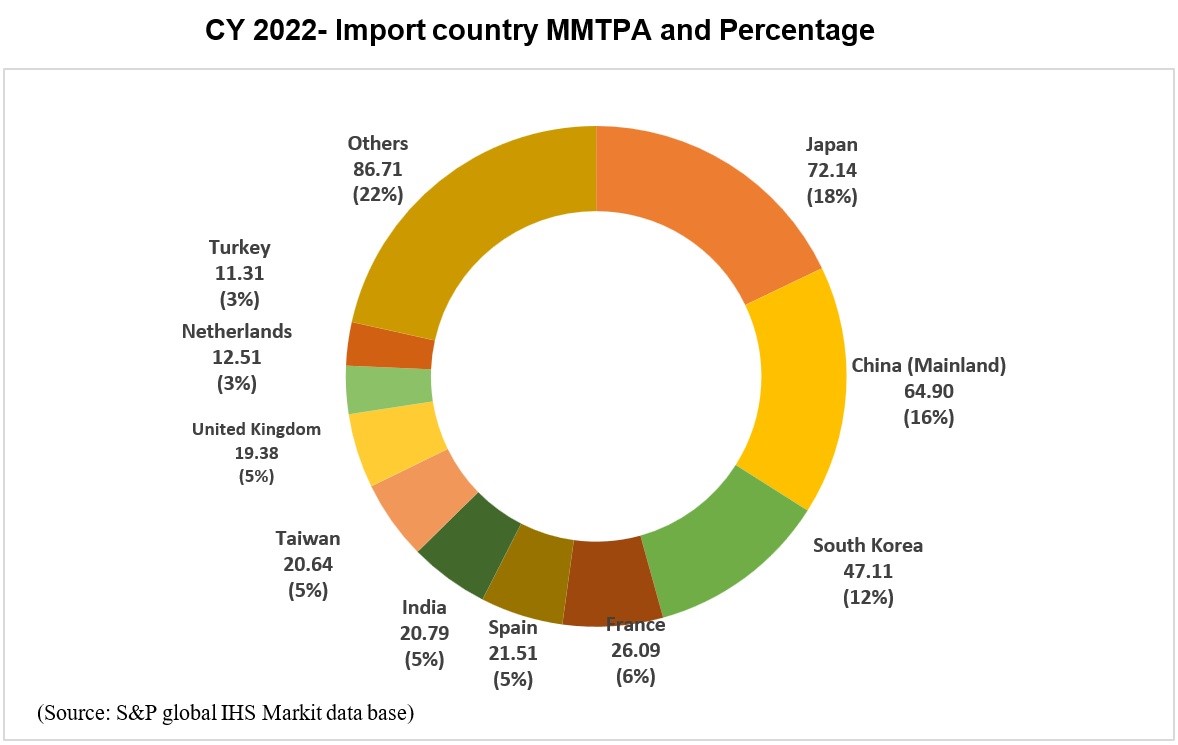

Figure 2: LNG imports by different countries.

Figure 3: LNG as percentage of expected gas consumption in India.

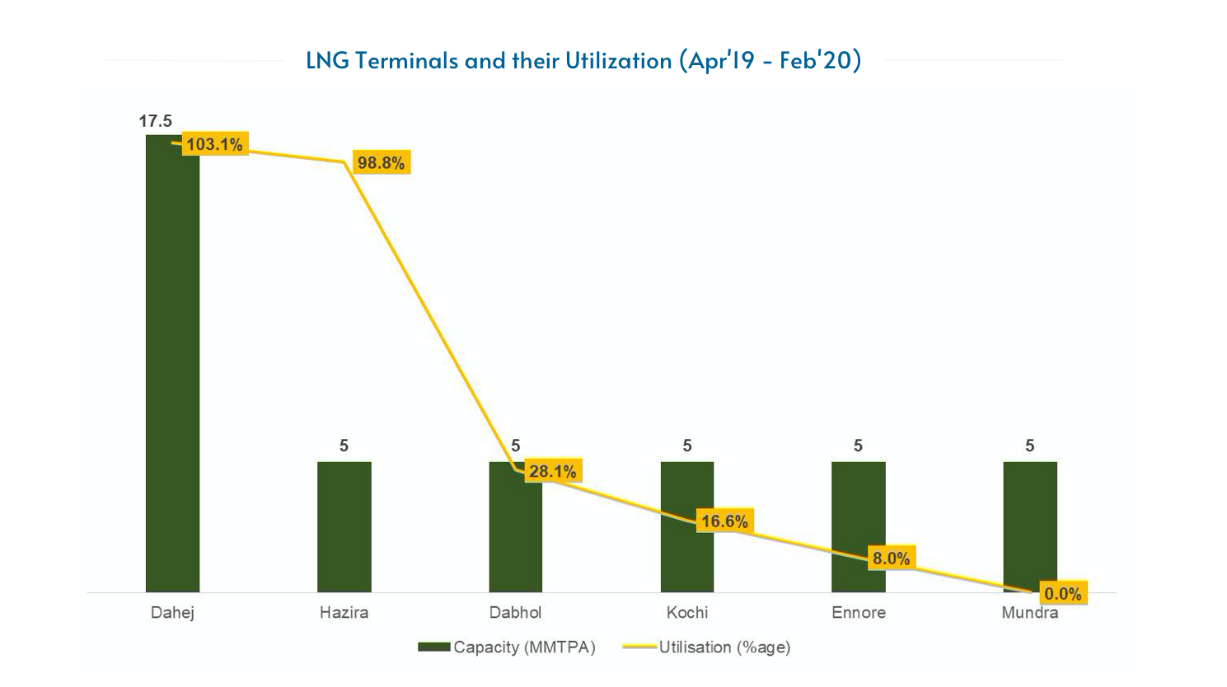

Current regasification capacity in India is 47.7 MMTPA. Only Petronet’s LNG terminal at Dahej and Shell’s terminal at Hazira are operating at near optimal capacity. Other terminals remain underutilized and operate at less than 25% of their regasification capacity. 17.5 MMTPA of the 21MMTPA of pan-India imports were at Dahej. Figure 4 gives details.

Terminals at Kochi and Ennore are operating below capacity due to insufficient pipeline connectivity with the demand centers. The 5 MMTPA Dabhol terminal is being operated at low capacity owing to the absence of breakwater required for protecting LNG ships during the monsoon season (H-Energy).

Figure 4: Capacity utilization at various LNG terminals.

There are new Regasification projects under construction by different companies at various locations namely Jaigarh, Jafrabad, Chhara and Petronet’s greenfield floating stage regasification unit based LNG terminal at Gopalpur on East Coast along with expansion of Petronet’s existing regasification terminal at Dahej from 17.5 MMTPA to 22.5 MMTPA. It is expected that with the completion of all these new terminals and expansion projects, the total regasification capacity in India will increase from 47.7 MMTPA to 72.7 MMTPA.

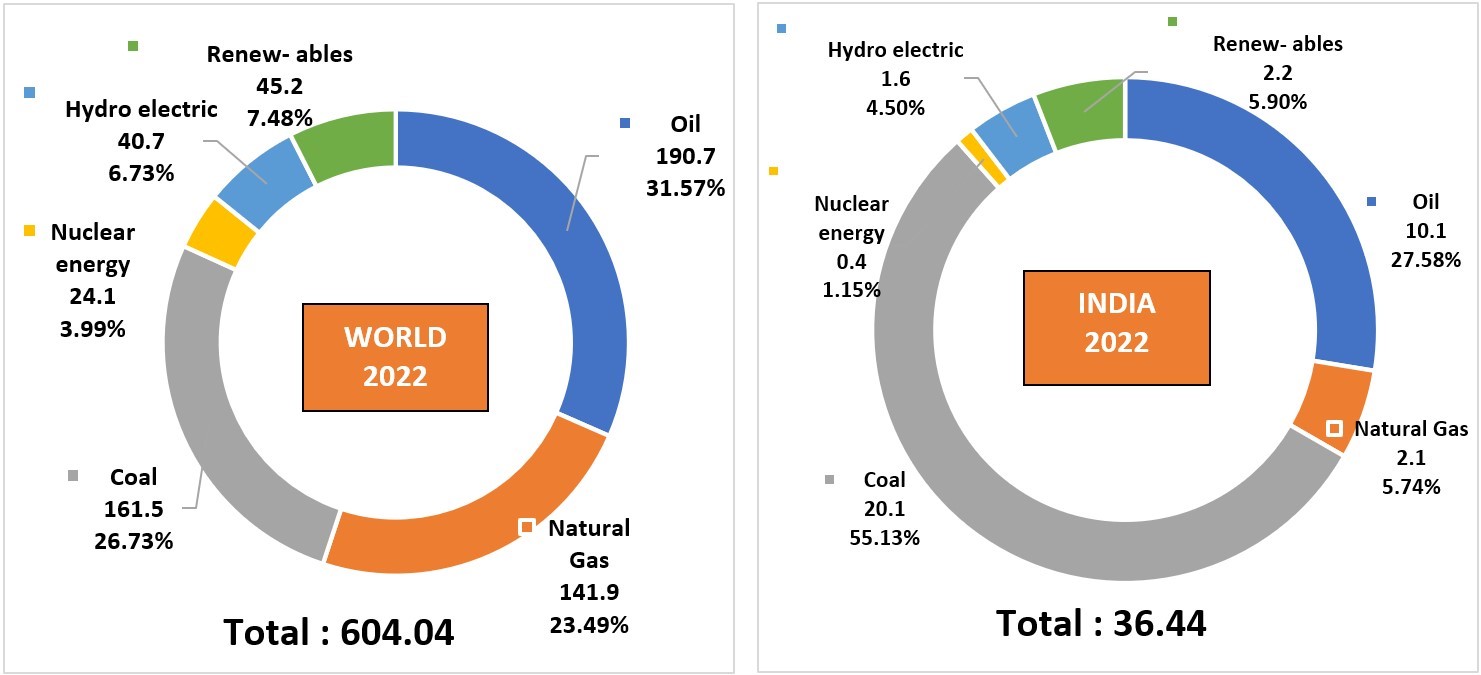

In order to achieve 15% share of Natural Gas in the energy basket of India by the year 2030 (from 6.2% at present, see Figure 5), India would require around 150 MMTPA of LNG re-gas infrastructure. Thus, creating additional capacity of over 77 MMTPA is necessary. The drivers of increased gas demand are shown in Figure 6.

Figure 5: Energy consumption mix by world versus India.

Figure 6: Drivers of gas consumption by industry.

Since domestic capacity is limited, growth in gas consumption can only be met through importing LNG unless there are piped gas connections to India, e.g., underwater piped gas from the middle east to the western seaboard. Such a project, however, takes decades to conceive and develop.

Business drivers

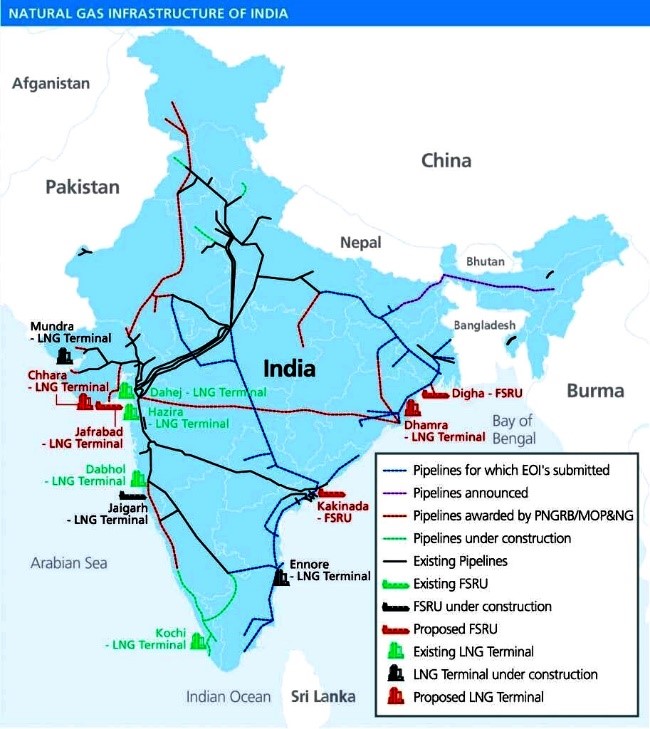

While the regasification capacity of India is more than 2 times the current imported volumes of LNG, the Dahej terminal alone is responsible for 80% of pan-Indian imports. Dahej is the crown asset of Petronet because of the dense network of gas-pipelines that connect to Dahej and the proximity to the Middle-East (primary supplier). See Figure 7! While terminal run by other companies will slowly get connected to the gas network, its going to be a long and unpredictable process. With secular demand for increased LNG, that’s not going to be a problem for Dahej.

Also, Dahej’s capacity is increasing from 17.5 to 22.5 MMTPA with 2.5MMTPA increase expected by 2024. The pipeline between Kochi and Bangalore has continuously had challenges, in the coming years it will get completed (this integrating into the national gas grid) leading to a huge increase in the capacity utilization from 20-30% to 80%. So effectively, for Petronet, its gas-pipeline connected capacity will go from 17.5 to 27.5 MMTPA (60% increase). Keep in the mind that the pipelines are not owned or maintained by Petronet, thus no maintenance capex related to these. That’s why, Petronet has a high ROE and ROCE, 26 and 22% respectively.

Figure 7: Map of gas pipelines in India (2021). Source here

Analysis of Financial Statements

From a balance sheet standpoint, there is no debt – in fact the market cap is INR 321000 million while the TEV is 270000 million, so nearly 5000 million in cash on the balance sheet. Book value is nearly 50% of the market cap (150000 million).

From an income statement perspective, revenue and EPS growth is 14 and 10% respectively over the last 5 years. These should expand considerably as new capacity becomes available in the coming years. A dividend yield of 3.3% that grows regularly is also decent.

In 2023 FCF was lowered because of capacity expansion and the building of a 3rd Jetty at Dahej – no worries, a good use of capital!

Table 1: Key metrics from financial statements in millions INR over the past five years.

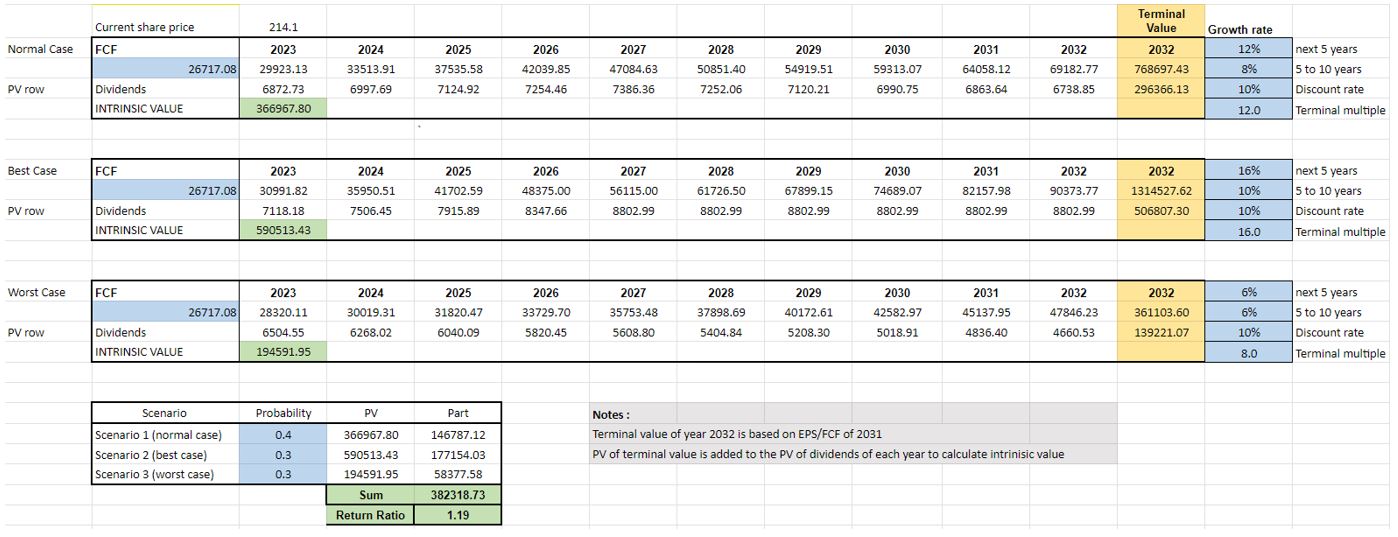

Under average 5-year FCF assumptions and modest growth rates, Petronet seems like a decent investment with returns of 10-12 percent with limited downside. FCF should increase with nearly a 60% increase in planned capacity that is almost guaranteed to come online in the next years.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

With a strong balance sheet, good ROIC and excellent gas pipeline connectivity to its terminals, Petronet is a predictable business that produces reliable FCF – these might vary year-to-year based on new contracts being negotiated and the ongoing spot market rates, but over a few years, things will even out. With secular demand for increased gas use, importing of LNG is unavoidable. Petronet gets a piece of the pie, come what may. Just keep in mind that one of the risks is that Petronet is still a government company.

Company news

Petronet on 31st Oct 2023 announced a greenfield expansion into petrochemicals at Dahej – an entirely different business and likely deworsification. The proposed project includes 750 KTPA of Propane Dehydrogenation (PDH) & 500 KTPA of Propylene (PP) plant including propane and ethane handling facility. The cost will be INR 210,000 and will take 4 years for development. The cost per se is not an issue – it can be covered by the coming 4 years of FCF and the cash on the balance sheet. Of course, taking some debt will not be a problem either. In effect we will be transferring FCF for the next 4 years into equity. The question to ask is what will the ROE be on the invested capital? I assume, the project will take about 7 years – 4+ years for development and then a year+ for the factory to get fully operational. So, worst case, there we are going to see cash flow from this development only from 2030. I expect ROIC for Petronet to get to and stay in the low teens for the next years and no meaningful change in stock price. Here’s a report by Emkay on the Petrochem foray.

Catalyst

I like the regasification business and at current prices would be willing to buy it. But the foray into Petrochem means that FCF of next years will disappear and ROE on this investment is not visible. If price falls by 25% to around INR 150 per share, then wake me up as that would give some margin of safety!

Amara Raja Energy & Mobility Limited: Powering Ahead (16-12-2023)

MF data for last 3 months as under :

Month : Shares held

1.Sep, 2023 : 8,771,773

2.Oct, 2023 : 8,922,802

3. Nov,2023 :9,591,632

Deepak Fertilizers and Petrochemicals (16-12-2023)

You can track the progress in NCLT. The link is already mentioned in the following post

However this would not be a material event in the short term. The is a demerger with in the listed company and the demerged cos will be subsidiaries of the listed co i.e. Deepak fertiliser.

The management tries to bring institutional investors to these subsidaries (i.e. demerged companies) and then list them seperately later. I hope it can happen by Fy 2026

Disc: Holding small position

Praveen

Deepak Fertilizers and Petrochemicals (16-12-2023)

Any update on NCLT hearing for demerger ?

UPL Ltd – global agrochemical company (16-12-2023)

UPL had acquired some stake in Clean Max Kratos Pvt Ltd to foray into renewable energy. And now they are in the list of 14 companies interested in setting up green hydrogen production facilities

PI Industries – Superior Business Model (16-12-2023)

Given the company’s history, from a long term pov yes i think so even though we need more clarity in the short term.

Disc : Invested and added more recently