Thanks for sharing this information.

Posts in category Value Pickr

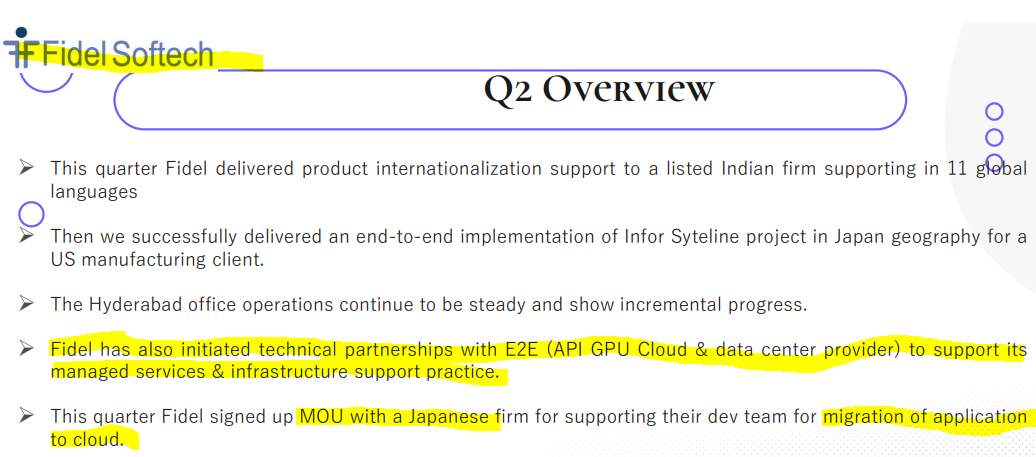

E2E Networks Ltd – Listed small Cloud computing player (22-11-2024)

I was going through Fidel Softech inventor presentation. surprised to see mention of E2E networks and use of their cloud GPU for one their Japan client cloud migration ![]() … E2E is quietly expanding its root towards becoming big banyan tree.

… E2E is quietly expanding its root towards becoming big banyan tree.

Export data and learnings (22-11-2024)

OCTOBER 2024 UPDATE:

India’s overall exports(merchandise and services combined) during October 2024 is estimated at USD 73.21Billion, registering a positive growth of 19.08 % compared to Oct-23.

Total import during Oct-24 is estimated at USD 83.33 billion, positive growth of 7.77% over Oct-23.

Monthly merchandise export during Oct -24 is USD 39.20 Billion, 17.2% increase compared to USD 33.43 Billion of Oct- 23.

The estimated value of service export during Oct -24 is at USD 34.02 Billion, 21% increase compared to USD 28.05 Billion during Oct-23.

Coffee exports are up by 34% during the month and 48% from Apr to Oct-24…

Rice exports increased significantly by 88% during Oct.

Marine products exports increased by 5%( positive growth after many months).

Iron ore exports continue to be in negative territory.

Ceramic products and glassware exports reduced by 5% during the month.

Pharma exports continue to grow.

Chemicals have grown significantly during October , up by 29%.

RMG of textiles exports continue to have double digit positive growth.

oct24.pdf (369.1 KB)

Aegis Logistics – Can It Be Exception? (22-11-2024)

Aegis has announced filing of the Draft Red Herring Prospectus for IPO of AVTL for raising Rs.3,500Cr. I do not see the DRHP link on the SEBI website yet( SEBI | Public Issues), so cannot share more details.

Proposed initial public offering (“IPO”) of Aegis Vopak Terminals Limited

Aegis Logistics – Can It Be Exception? (22-11-2024)

EBITDA grew by 8% and EPS was flat. Distribution business growth seems to be slower, their LPG and liquid units should be commercialized in FY25 acting as the next lever of growth. Concall notes below.

FY25Q2 concall

- Terminaling: 1’064’000 MT (vs 1’020’000 MT in Q2FY24)

- LPG capacity will increase by 130’000 MT by end of FY25 (Mangalore and Pipavav)

- Aegis Vopak: filed DRHP for IPO (will reduce debt, general corporate purposes, expansion)

- Mumbai: JNPT unit will be commercialized in FY25, its held under Aegis Vopak JV

- Ammonia

o Have got commitments from customers for Pipavav terminal

o Ammonia division economics will be similar to liquid division, throughput will be lower than LPG but realizations higher than LPG (2.5-3x of LPG realizations). EBITDA margins will be ~90%

o Will be hosted in Aegis Vopak JV - Sourcing: 194’000 MT (vs 174’000 MT in Q2FY24)

- Kandla Gorakhpur pipeline should be commercialized in mid-2026

Disclosure: Invested (sold shares in last-30 days)

Samhi Hotels – Turnaround with Tailwinds (22-11-2024)

There is overhang from the promotors who are PE firms, It needs time to go through and hotel industry is capital intensive industry which is long dated in nature. After 2020, we have seen such markets that if any stock doesn’t perform for 6 months we are derating and questioning position. one needs to be patient with his/her thesis and play the cycle.

Disclosure : invested

Websol energy system ltd (22-11-2024)

If the price of wafers also increase, won’t it affect websol too ?

Calcom Vision – Say yes to LED (22-11-2024)

Yes you are correct. LED Price erosion is an issue since past 5 quarters for Calcom and whole segment. It has made waiting longer for sales number to show meaningful growth. As far as there is good volume growth and investments in backward integration bearing fruits (Better EBITDA%), i would like to wait patiently.

Also, new initiatives like PLI Scheme Investments and New Product Announcement are good enough for me to hang on longer. I have hawk eye on “Cash Flows” as there has been too much of capital raise and good amount is blocked in receivables and Working Capital.

Regards,

Mukul Jain

Invested and Biased

KPI Green- Turning Sunshine Into Cashflows (22-11-2024)

Bull market valuation PE and bear market PE are not same, utility companies don’t command this kind of valuations, not talking for KPI only but whole sector. Lets see how things transform in future.

Ujjivan Financial – Small Finance Bank (22-11-2024)

I agree, Good times and good price don’t come together.

but Small Finance banks are cyclical in nature if any unforeseen event happens like natural calamity, etc… the banks has no other option than writing off the asset. I believe what ever they have written off for this quarter and going to write off for the next one or tow quarters. it is already discounted in the price and have sufficiently provisions for it.

the company’s topline has been growing consistently every year, there has been no Year they have posted a loss.

positives in my opinion,

→ Good Management.

→ might get universal banking license in the coming year.

->Long-term growth is intact.

Disc :- invested from the recent lower levels.