Request for flagging whether company is NSE only or BSE only or both and similarly for SME or not. That would be great in filtering a particular type of companies.Thank you.

Posts in category Value Pickr

BULL in BEAR Market (10-12-2023)

What has been your experience with arbitrage funds? How have these performed for your investing period? Who would you suggest or not suggest these funds to?

Portfolio Analysis – Shailesh (10-12-2023)

View 2024 …

II have updated my portfolio view in this thread

BULL in BEAR Market (10-12-2023)

My view for 2024

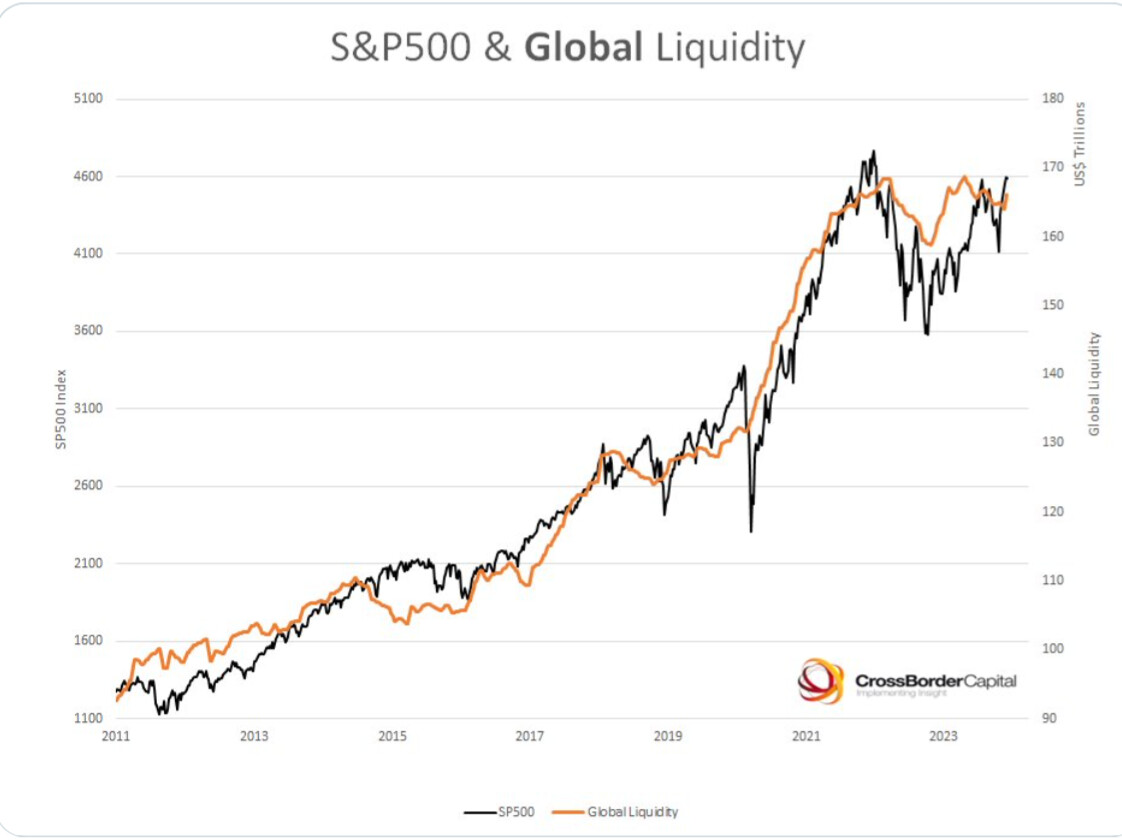

2023 was a surprise year . In line with my view that market is overvalued esp in context of higher interest rate , I kept shifting my asset allocation from equity ( 90% to 80%) to debt …

But Crazy market movement meant I had sell lot more equity than I had planned in absolute term . Overall PF return was 50%+ inspite of huge shift to debt and movement from midcap to large cap. That indicates level of craziness that markets is in .

Last 4 year CAGR of 40% even on my conservative PF which is high on large caps / passive ETF and debt scares me esp when geopolitics risk are high and interest rate are higher in decade . Global liquidity index and domestic investor SIP is driving market valuation beyond my comprehension .

So what happened …

Oil / Gas Magic

Contrary to expectation of OPEC inspite of oil production cuts … Oil prices reduced … America increase in oil production that compensated Saudi reduction was big surprise of 2023…

Add to that … now on LNG

Low energy prices meant lot of Risk related to Indian market reduced and also gave flip to equity earnings .

US and India GDP Gr continue to surpass expectation

US at 5% and India at 7% are excellent Gr nos and will increase overall optimism esp to invest in capacity expansion .

Global Liquidity continues to grow

Against view of FED balance sheet tightening has been countered by US and other Government fiscal loosening esp inn areas of infra spends and war has lead to global liquidity remain favourable .

So what is my action plan 2024 …

I think we have pulled in lot of future returns and GOVT investment spending will reduce as we come closer to near and post election

So I have decided to

-

Reduce asset allocation of equity to 70% in case market continues to rally like it has done in 2023 and increased allocation to long term debt or arbitrage funds

-

If market remains stagnant and declines not more than 10% . No change in asset allocation

-

If market declines > 20% < 40% increase equity allocation to 85%

-

If market declines > 40% increase equity allocation to 90%

Techno electric engg ltd (10-12-2023)

Agree. Congratz to all stakeholders who stayed put in the stock.

My second top holding (9% of my portfolio). Invested from last 3.5 years… lot of patience required considering everything was going up but not this stock whereas fundamentally thiz was top class

Best P2P lending platform advice (10-12-2023)

I recommend not to go for P2P platforms since almost all platforms are experts in lending other’s money with very inadequate and lethargic efforts towards recovery ultimately leading to an overall loss in the portfolio. Even RBI is unable to render much support although they have tall claims of investor education and protection. In my experience i2ifunding was the only one to have done a better job.

Phillips Carbon Black (10-12-2023)

Do we have any clarification from the management if they are going to retain the old management or bring new management into ACPL?

Companies with 20%+ growth guidance for next few years (10-12-2023)

Radiant guiding for 20+ CAGR growth in the coming years. Their DBJ (Diamond, Bullion & Jewelry) vertical expected to show results from this qtr3 while the recent acquisition of Acemoney puts it in a different league and expected to contribute from FY25.

Investing Basics – Feel free to ask the most basic questions (10-12-2023)

hi,

How to generate and use a regression equation for investing.

Please elaborate or share some link.

Regards

Indian Hotels–for long term portfolio stability (10-12-2023)

EV / EBIDTA is indeed currently the most fashionable valuation metric – not just for hotels but I think across majority of the sectors.

I tried to look up how brokerage houses are valuing IHCL. Geojit Paribas has used a valuation of 22 X FY25E EV / EBIDTA. HDFC Sec assigns a multiple of 22 X EV / EBIDTA. Axis Securities gives a value of 38 X FY26E PAT. I-Sec does slightly better, as it gives 23 X FY25E EV / EBIDTA and also does some adjustments for cash, minority interest etc. and then adds values of Taj GVK & Oriental Hotels (but not others), doing a SOTP valuation. Motilal Oswal gives a value of 25 X EV / EBIDTA and does the same SOTP as I-Sec but also includes Taj Sats. Ventura Securities assigns a flat P/E of 46 X to FY25 PAT.

Traditionally, hotel stocks used to be valued on asset value basis. You could count how many rooms it has, assign a value of X per room, calculate the value of the hotel and then adjust it for other factors like debt on the balance sheet. Or based on benchmarks set during comparable buyout / M & A deals. But given that a significant share of revenues now a days come from management contracts, this too doesn’t seem appropriate now.

I am not a fan of EV / EBIDTA, but I don’t have an alternative either, especially for a complicated business like IHCL. Perhaps a better (and lazier) option is to ride the uptrend so long as it lasts, and exit based on technical analysis.