I was having a look at this company on screener can anyone help me understand why is the inventory day shown so high in screener whereas it is roughly only 250 days ! turnover of approx 1050 cr and inventory of 745 cr avg , how can the inventory days be 517 days ! if anyone can help it will be great

Posts in category Value Pickr

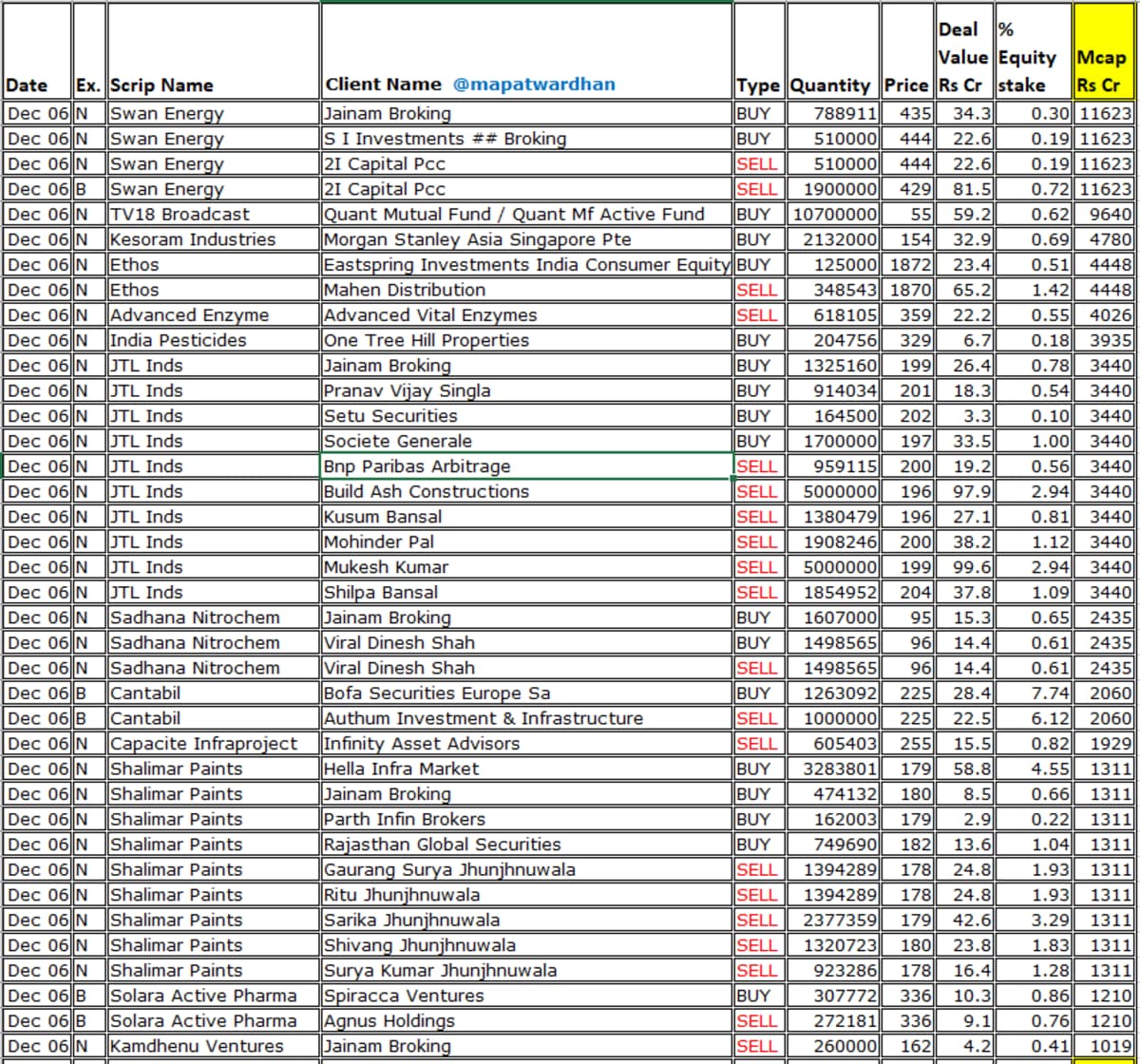

Sadhana nitro :a Dog or a Horse? (07-12-2023)

Jainam broking has bought at 95

Rural Elect Corp (07-12-2023)

other probable reasons why IREDA could continue to command a premium over REC/ PFC and REC / PFC could continue to catch up :

(1) REC PFC till date were financing thermal power projects which were having long gestation period of 4-5;years even more . The PPA normally for five years , lowered from 10 years earlier.

in comparison, renewable projects gestation period is 1- 2 years and normally PPA signed for long term 10-40 years. i can see PSP projects signed recently for 40 years.

so it goes in favour of Renewable energy financing.

That could be the reason both REC PFC are increasing their renewable portfolio. so market has re-rated these stocks.

In addition REC PFC have decided to add infra projects in to their portfolio which may be bit risky though. However the opportunities is huge in infra too.

(2) IREDA is 100% renewable and hence may continue to trade at a premium, though PE re-rating or de-rating or could take place depending upon financial performance

Discl: invested in all the 3 stocks. may be biased. not a buy sell recommendation. please do your own assessment before investment

Himadri Specialty Chemicals (07-12-2023)

HBL power is one of them which already manufactures LFP as well as NMC batteries.

read this to understand other Indian companies capex.

KDDL (Ethos Watches) – Scalable business model at an inflection point? (07-12-2023)

Sorry my mistake! I will remove it

Ritco Logistics-Microcap opportunity (07-12-2023)

Company has recently issued warrant to promoter at price of 247.

TAAL Enterprise – cheap valueations (07-12-2023)

A lot of positives have been captured already in this thread, so I do not want to repeat them here.

But I am skeptical of the promoter quality. Performance of both Taneja Aerospace and ISMT has been poor. There was this aircraft accident in 2020 after which they shut down the business, and there was a bird hit earlier in FY17. This reflects poorly on the management. Accounting quality also needs to be scrutinized closely. When the aircraft accident took place in FY20, the losses were shown as Exceptional Item in the P & L, but when insurance claim was received, it was accounted as Other Income:

This inflates the PBT for FY21. More importantly this amount has not been deducted from PBT while calculating the CFO and so the CFO also stands inflated to that extent. Meanwhile, the aircraft continues to appear in the Gross Block under Right of Use Asset even today. I am not fully sure how this accounting works; but something doesn’t seem right here.

Salil Taneja has maxed out his remuneration at 10 % of PAT already which seems too high too early. I am also curious why a software company (Taal Tech) with a Gross Block of Rs.8 crores has Rs.1.42 crore of vehicles in it.

(Disc: Tracking, no positions)

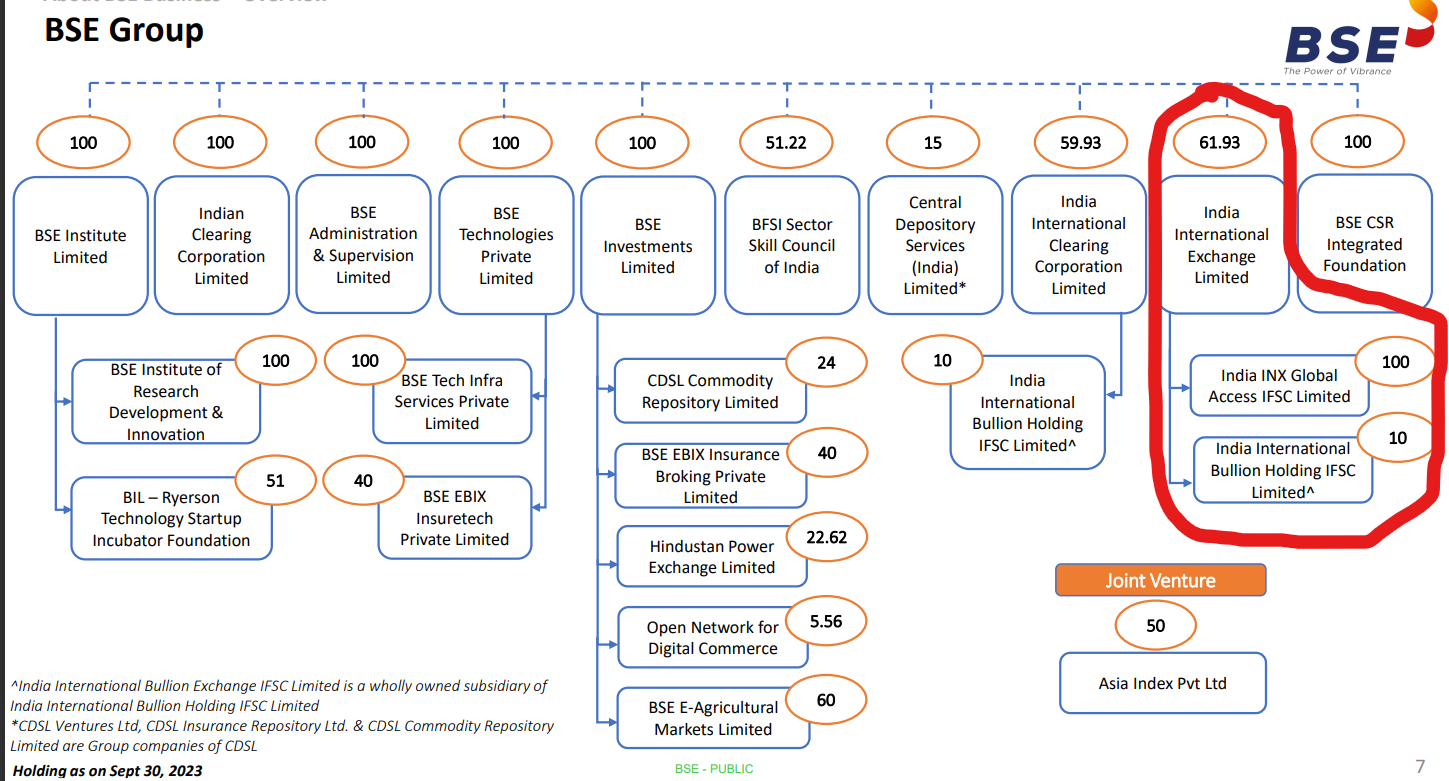

BSE (Bombay Stock Exchange)- Bet on Financialization? (07-12-2023)

BSE, NSE GIFT City units to be merged by Jan 2024; direct listing by April (msn.com)

How is this going to work? Who will control the GIFT city exchange? NSE or BSE? The unified exchange will be competing with SG/HK/LSE/NYSE bourses, and will be the GIFT City IFSC gateway for Dollar Inflows to Indian listed stocks/bonds etc.

BSE holds 61.93% indirectly in this. Any thoughts from boarders on this development?

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (07-12-2023)

Let’s try to understand the practicality of this news. Currently 50% (approx) of the ethanol demand is met by sugar industry. If they stop procuring all of this (Ethanol made from B molasses, C molasses and sugarcane juice) they won’t be able to meet targets of even 15% blending forget 20% blending of 2025 which anyways will 1000 crore litres (approx) from sugarcane. Lets think of the feedstocks demand in this case. All the feedstocks apart maize is already in short supply. Price rise of wheat and rice which already has happened will happen more and create inflation.

Let’s come to the news government will procure only ethanol made from C molasses. It will result in 20% less ethanol production to the sugar mill compared to B molasses and sugarcane juice. Anyway, given the current sugar price scenario sugar mills were anyway going to use the C molasses way. Even if they stop in the long run the fundamental impact of the sugarmills will be optionality of their 20% revenues of the % of the ethanol produced will be lost. So net net not a major impact in the long run. Currently there is no impact at all.

Currently given the feed stock shortage and price rise in other commodities achieving this target of blending is already ambitious (without changing the dynamics of supply of all rice, sugar and wheat) If they want to keep a balance they wont practically stop sourcing of B molasses and Sugarcane Juice. I think its just to create a hype and this will help in keeping sugar prices in control and even hoarders will be cautious in hoarding sugar.

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (07-12-2023)

Let’s try to understand the practicality of this news. Currently 50% (approx) of the ethanol demand is met by sugar industry. If they stop procuring all of this (Ethanol made from B molasses, C molasses and sugarcane juice) they won’t be able to meet targets of even 15% blending forget 20% blending of 2025 which anyways will 1000 crore litres (approx) from sugarcane. Lets think of the feedstocks demand in this case. All the feedstocks apart maize is already in short supply. Price rise of wheat and rice which already has happened will happen more and create inflation.

Let’s come to the news government will procure only ethanol made from C molasses. It will result in 20% less ethanol production to the sugar mill compared to B molasses and sugarcane juice. Anyway, given the current sugar price scenario sugar mills were anyway going to use the C molasses way. Even if they stop in the long run the fundamental impact of the sugarmills will be optionality of their 20% revenues of the % of the ethanol produced will be lost. So net net not a major impact in the long run. Currently there is no impact at all.

Currently given the feed stock shortage and price rise in other commodities achieving this target of blending is already ambitious (without changing the dynamics of supply of all rice, sugar and wheat) If they want to keep a balance they wont practically stop sourcing of B molasses and Sugarcane Juice. I think its just to create a hype and this will help in keeping sugar prices in control and even hoarders will be cautious in hoarding sugar.