In my opinion Growth will come from the uptick in the conversion rate of passengers, which is around 7.3% in Q2 and It was 6.2% in Q4FY23. They supposed to close some international deals, which will boost the growth at an exponential rate as it will add pax.

Over all on bearish case i am confident about their 20-30% growth, margins may improve slowly on QoQ basis as volumes increase.

Posts in category Value Pickr

Dreamfolks services limited( DFS) (06-12-2023)

Carysil (earlier Acrysil) – Kitchen sinks (06-12-2023)

Its my Question…see the reply from the Chirag about the upcoming deals, this itself explains that 200k volume could be possible in Q4FY24/Q1FY25.

Calcom Vision – Say yes to LED (06-12-2023)

Good observations.

Even with these few -ve things, i feel that there is a good opportunity for the company to have decent growth in coming few years from BLDC fan & EV chargers.

They might be late entrants in the Smart meters category to gain market share but this wil l also push the revenue slightly in addition to the above fast growing products.

Himadri Specialty Chemicals (06-12-2023)

Isn’t it a risky spell for himadri entering into this segment?

Cathode materials industry is predominantly led by Chinese players, with a total requirement of 1.4 million tonnes. Himadri emphasises its intention to sell these materials to original equipment manufacturers (OEMs). Contemporary Amperex Technology Co.Limited (CATL) a chinese battery manufacturer which holds majority share in LFP (lithium phosphate battery).

Major opportunity is there for this company but if any renown Indian brand comes into picture from the same serving segment as well it can be a major threat as well.

Omkar’s Portfolio Analysis and Discussion (06-12-2023)

Some initial thoughts on new fund houses – Whiteoak and Helios

To start with, I believe its very difficult for a direct equity investor to be a good mutual fund investor because direct equity investor has strong prejudices. Any analysis on mutual fund portfolio/ strategy is almost always done through that prejudiced lens which many times do not appreciate the fact that equity market rewards multiple strategies/frameworks if executed well

With that disclaimer, following are my initial thoughts on both of these fund houses after going through factsheets and other material available on the website

Whiteoak

The key tenets of their strategy is not too much focus on particular style, sector and market cap because they believe constructing balanced portfolio with blend of these factors which can help improving consistency in the performance. if I look at their portfolio, following points stand out

- Large diversified portfolio. There are 108 stocks currently in flexi cap fund

- Having higher allocation to small mid cap as they believe it gives them allocation lot of sector which are not represented in NIFTY. Small mid cap allocation is around 40% which is way higher than category in flexi cap

- Entire portfolio construction, sectoral weights and small mid cap tilt is based on bottom up research. That means they view portfolio construction as a function of stock selection and not based on economy/market/sectoral cycle we are in

- Stock selection is biased towards buying high ROCE businesses with discount to intrinsic value which is defined by cash flows. I see less representation of PSU, defence and railway sectors etc. sectors which has low cash flow conversion

Initial judgment –

I really liked the portfolio construction approach, i also find communication about portfolio strategy very clear and something I can measure over cycle. I havent compared their strategy with other fund houses yet. I will keep this thread updated as and when I do that analysis

Helios

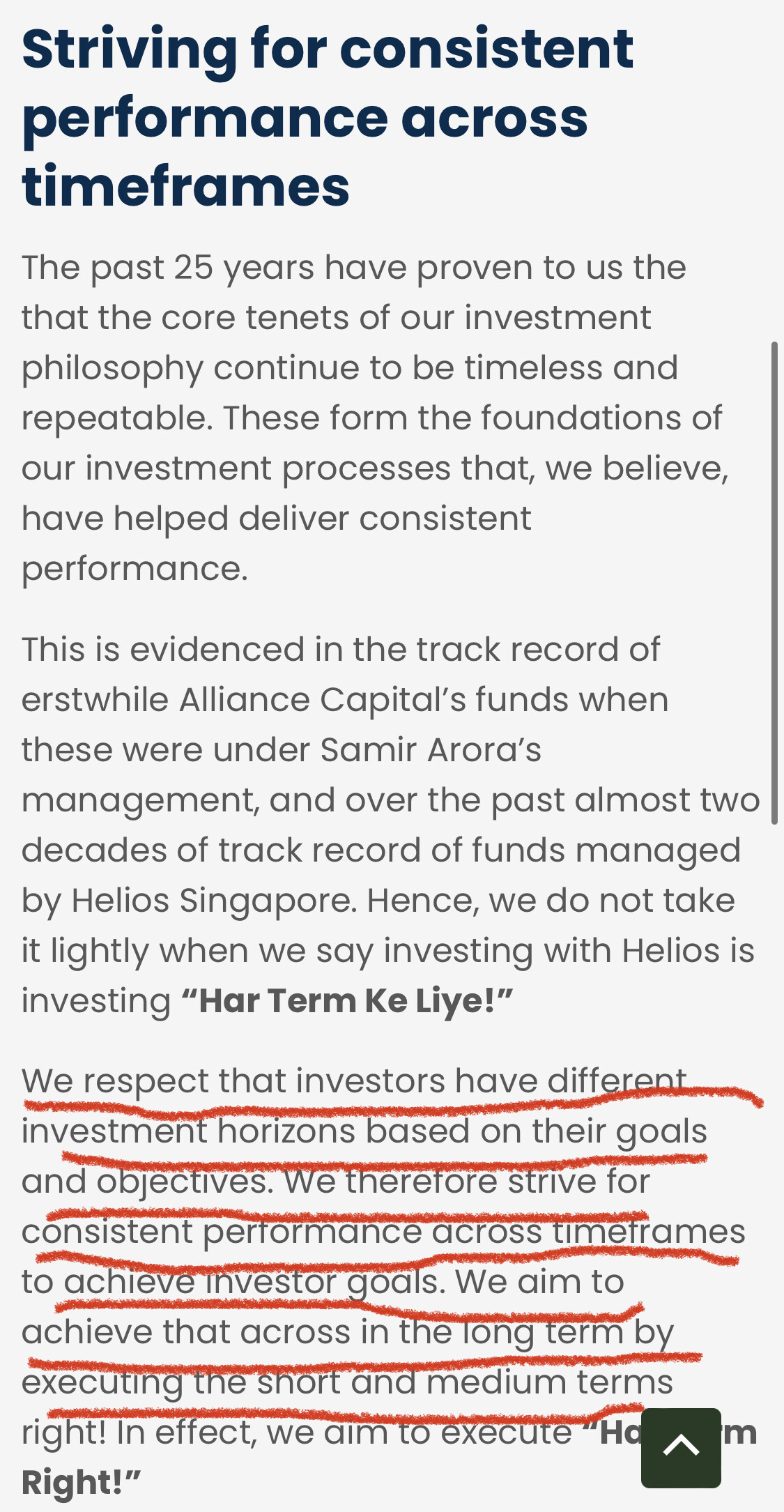

I personally did not understand what exactly is their portfolio strategy which they have termed as a “Bar-bell” strategy. To me, their is no unique attribute which stands out from their investment framework. Above all, I can not relate with their campaign ‘Har term ke liye’ which I am attaching below. I dont want fund manager to focus on near term returns because thats a job of financial advisor according to me ( my prejudice is already speaking ![]() )

)

Everest Kanto Cylinders Ltd. – A long runway ahead! (06-12-2023)

Not now but in long run it will.

but there are many competitors waiting for this opportunity like supreme and time technoplast.

Bulk Deals Daily Log (06-12-2023)

Hi Valuepickr, back with the analysis

5th Bulk Deals Log

Date: 06th December, 2023

Links:

NSE: https://www.nseindia.com/report-detail/display-bulk-and-block-deals

The bulk deals on NSE were from 5th of December and the ones on BSE weren’t as interesting again. So focusing on the NSE deals only that weren’t covered last time here.

- Emkay Global Financial Services

Unlike the common perception, I think investment banks have their own cycle linked with low interest rates and not directly with market performance. This company has seen renowned investors like Ajay Upadhyay enter, so it is definitely something interesting. Clover Infotech has bought 1,50,000 shares of the company at 121.65.

- Inox Green Energy

Citadel securities India markets private limited entered this stock. They bought 14L shares at Rs.77.95 This has seen good performance in the past. But I wouldn’t be so interested at these valuations.

- Reliance Power

Hriti Private Limited, which mostly acts like a scalper has invested in this company. They bought more than 3 Crore shares at Rs. 21.52. Mathew Cyriac invested in this company earlier so it does seem like something interesting is happening, but I personally think it is a high beta stock, which would be badly affected if the markets fall. Again however, valuations are definitely in favour for this company.

I promised to study Narmada Agrobase and Akash Dhiman’s buying and selling last time. However, there are some issues I’m facing with accessing this week’s data, but I’ll be sure to share that in the next post.

Navneet Publications – a good com in education sector (06-12-2023)

Could you please tell why you have discounted risky cash flows with risk free rate of return, which is obviously lower? Effect of this is that your calculated intrinsic value will be higher

Titan Company Ltd : a three decade old company (06-12-2023)

Sales growth can be at 25% CAGR instead of 15% as has been in last 3 to 5 years and median PE has been at 85 in last 5 years. So these factors should be your neutral workings and Bull workings will be much above that. Also you are ignoring some new verticals in apparels and current exclusive 10 lakhs ticket size shops might pick up, which can go beyond these calculations.

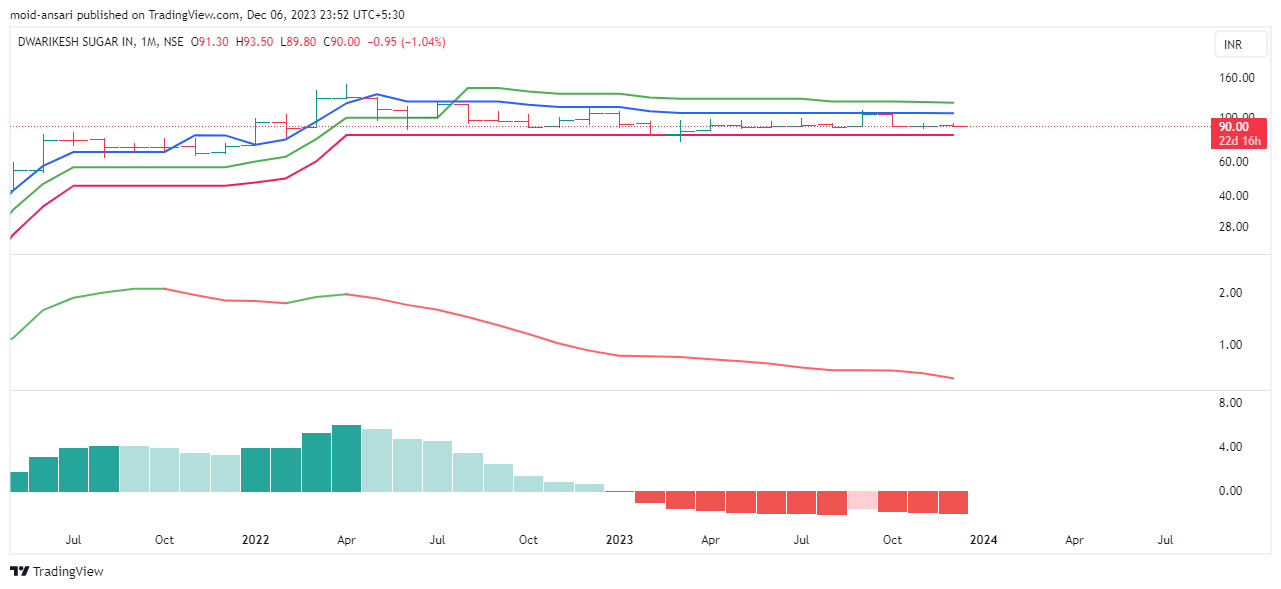

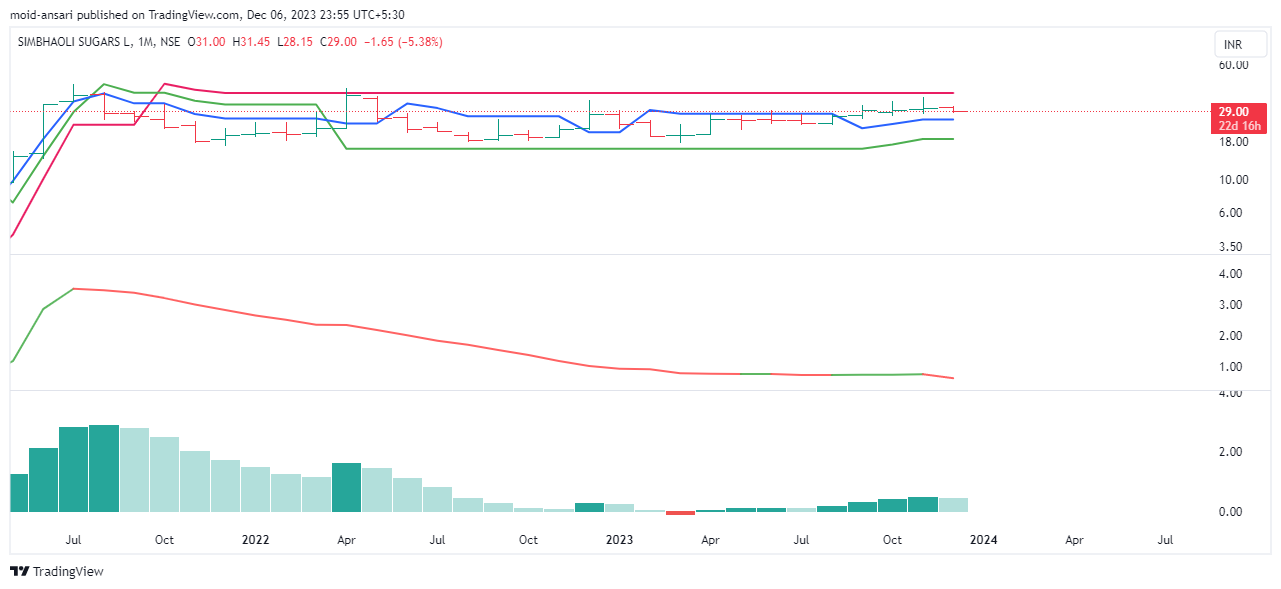

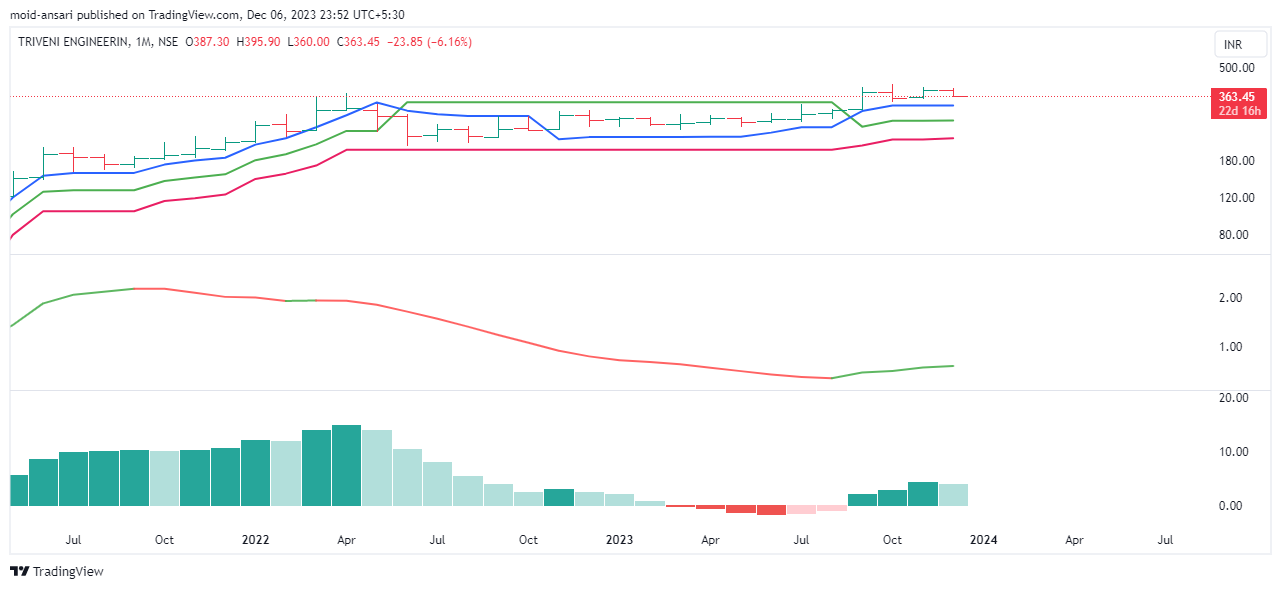

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (06-12-2023)

In case of doubt, it better to look at the long term charts of the leading companies in the sector to find out if there is sectoral turnaround.

Stock prices of many companies turning bullish from a very similar technical set up …all at the same time is the surest indication of a sectoral uptrend.

In sugar sector such a thing happened in early 2021…after that many frontline sugar stocks became 3-4 baggers.

As of now, among sugar stocks only Triveni Engineering is worth making fresh investment.

Sorry to say this, but i do not find indications of sectoral uptrend in sugar stocks as of now. …long term price charts are an important component of my investment strategy for cyclical stocks.

Have a look at the monthly charts of the UP based sugar mills…as per my system only Triveni and Uttam are looking good