(post deleted by author)

Posts in category Value Pickr

Mrs Bectors Food Specialities: Can it beat the industry? (06-12-2023)

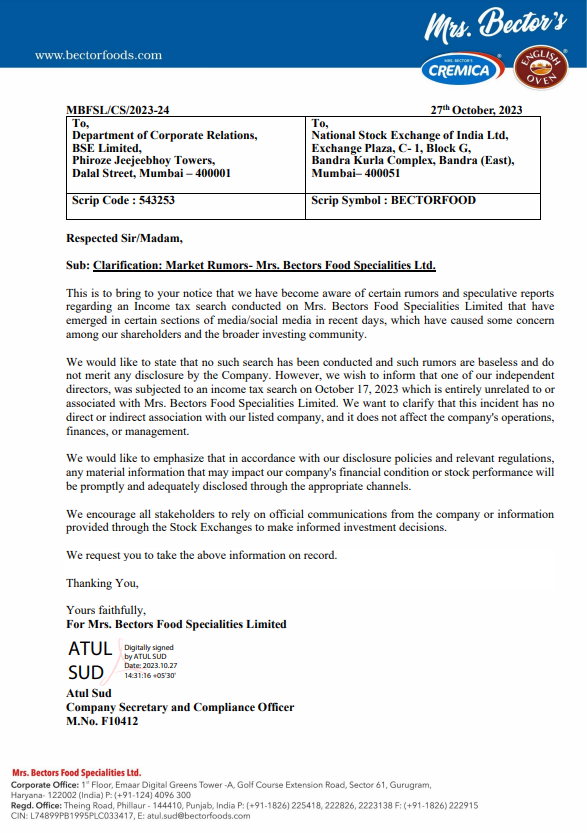

Clarification: Market Rumors- Mrs. Bectors Food Specialities Ltd.

Everest Kanto Cylinders Ltd. – A long runway ahead! (06-12-2023)

International LNG prices are coming down again… by next year it should be at pre-COVID levels… that is going to benefit EKC and all players in the CNG business.

For long term EKC is good as Hydrogen is also going to require Jumbo cylinders which EKC makes.

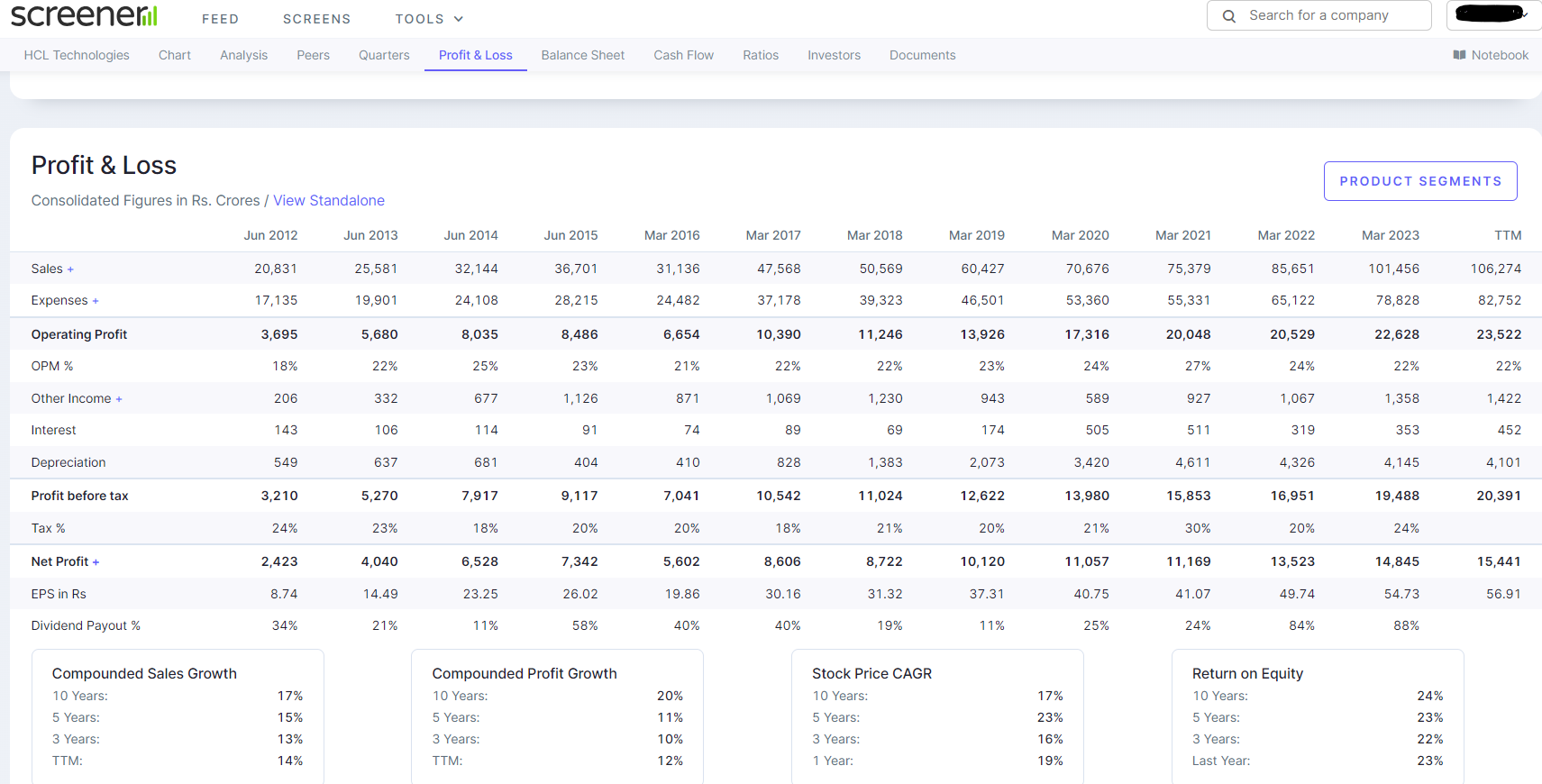

Screener.in formula for ROE? (06-12-2023)

The growth rates for Profit and Sales are also not adding up:

In this example, unless I am missing something, the TTM Sales growth (106,274 – 101,456)/101,456 = 4.75%, but, is shown as 14%.

JK tyres – Catching the speed (06-12-2023)

Hi …

Any one from tyre Industry can share how are things for Jk tyre

Thank you

Simple Investing (06-12-2023)

I did a long pending exercise…seems had been very casual and avoiding the hard work but words of @hitesh2710 made me dig deeper into this. I always wanted to check stock level CAGR for my portfolio, especially over different major time frames that I purchased them. This was primarily because I purchased same set of stocks at various levels over last few years and averaged up most of the time.

I must say I was positively surprised by the result. Pls note that the CAGR is in no way an indication that these stocks are good and would give similar CAGR in future. Also, these numbers are no indication of my portfolio CAGR as that is dependent on numerous factors like losses booked in stocks that were weeded out, allocation levels in existing and sold stocks, CAGR of sold stocks, current losses in some 1% holdings which I have excluded etc. (I have reasons to believe that overall, at Portfolio level, my CAGR would be around 15% only)

This is just an exercise for purpose of self-learning, deepening understanding of simple investing technique that I try to follow, understanding how individual stocks in my portfolio have performed, how staggered investing in same stock has performed, which stocks have not performed for me and reflect upon the why!

This is in no way a recommendation or endorsement of any stocks as any high CAGR can plunge anytime in short span and a low CAGR can increase anytime as well. Any CAGR over any timeframe can be misleading and not indicative of true returns that stock can give us as true returns depends on numerous factors and not just one. I am not eligible for any advice.

| Company | Percentage | CMP | Buy Price(s) | Holding period in Years (Approx, Average) | CAGR (Approx) | CAGR (Approx) | CAGR (Approx) |

|---|---|---|---|---|---|---|---|

| Tata Consumer | 15 | 950 | 150, 250, 600 | 10, 3, 1 | 20.27 | 56.05 | 16.55 |

| ITC | 11 | 455 | 170, 200 | 3,2 | 38.84 | 50.83 | NA |

| Trent | 9 | 2870 | 500, 750, 1000 | 3,3,2 | 79.05 | 56.41 | 69.41 |

| Pidilite | 8 | 2570 | 500,600, 2000 | 8,8,1 | 22.71 | 19.94 | 28.5 |

| Marico | 7 | 535 | 100, 270 | 10, 3 | 18.26 | 25.6 | NA |

| Midcap IT | 6.5 | NA | NA | 3, 1 | NA | NA | NA |

| Godrej Consumer | 6 | 1045 | 350, 550 | 8, 3 | 14.65 | 23.86 | NA |

| HDFC Life | 6 | 675 | 350, 450 | 6,3 | 11.57 | 14.47 | NA |

| United Spirits | 4 | 1070 | 550, 600 | 3 | 24.84 | 21.27 | NA |

| Nestle | 3 | 24600 | 15000 | 3 | 17.93 | NA | NA |

| Dabur | 2.5 | 550 | 250, 400 | 8, 3 | 10.36 | 11.2 | NA |

| Avenue Supermarts | 2.5 | 2050 | 4050 | 3 | 25.48 | NA | NA |

| Asian paints | 2.5 | 3220 | 1100, 1500, 2000 | 5, 3, 2 | 23.96 | 29 | 26.89 |

| Britannia | 2.5 | 4960 | 1000 | 8 | 22.16 | NA | NA |

| HDFC AMC | 2.5 | 3030 | 2000, 1700 | 3, 0.6 | 14.85 | 216 | NA |

| SBI Life | 2 | 1460 | 700, 750 | 6, 3 | 13.03 | 24.86 | NA |

| United Breweries | 2 | 1700 | 900 | 3 | 23.61 | NA | NA |

| Agro Tech Foods | 2 | 850 | 550, 500 | 8, 3 | 5.59 | 19.35 | NA |

| Hitachi Energy | 2 | 4790 | 1200 | 3 | 58.63 | NA | NA |

| 3M India | 2 | 31500 | 18000 | 3 | 20.51 | NA | NA |

All above figures are approximate, many out of my memory and I can be wrong in any or all of these numbers.

Disc: Invested & Biased. Not a buy/sell recommendation. Not eligible to give any advice. Post only for academic purposes and learning. I can be wrong in all my assessments.

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (06-12-2023)

In ESY 2023-24, no ethanol from sugarcane juice and B-Heavy will be procured by OMCs with immediate effect. Ethanol from C Heavy will be encouraged.

This decision by Govt takes care of sugar shortage, in the sugar season 2023-24.

No wonder, sugar stocks fell today.

Everest Kanto Cylinders Ltd. – A long runway ahead! (06-12-2023)

If GOI offers a MSRP and guarantees offtake, then all roadside trees, paddy straw etc will be used more effectively. Even wet garbage in cities would have a market

Himadri Specialty Chemicals (06-12-2023)

Himadri plans to set up Rs 4,800 crore LFP cathode manufacturing plant in Odisha (moneycontrol.com)

looks like a good plan, with EV going mainstream and sourcing it locally instead of China. Might even get some PLI subsidy too down the road.

Navneet Publications – a good com in education sector (06-12-2023)

A short research report with updated developments.

This report was originally written in FY21 as part of personal investment record. Updates have been made wherever necessary.

Business Overview:

- In the business of publication of books for Maharashtra and Gujarat State board schools and CBSE books under the brand name Indiannica (erstwhile Britannica).

- Cyclical nature of business with bulk of revenues coming in Q1 and Q4.

- Stationary products(paper/non paper), exports of which contribute majorly to revenues.

- E-Learning solutions under the brand name E-sense Learning.

- Managing schools under the brand name Orchid International Schools. (K12-Techno).

- Majority of the revenues is through publishing and stationary business.

Probable reasons for current valuation: - Loss making business verticals

- Significance of publishing business in a digital age (probably a newspaper moment for the business).

- Love and excitement among the people for edtech platforms.

- Has failed to capture CBSE publishing market share(yet).

Reasons why current valuation is wrong (mispricing exists):

-

The drop in revenue for FY21 was caused by the lock down which was announced by the Central Govt. in the last week of March. Most of the revenues are generated by the company in the months of April-May as students buy books for the Academic Year which starts from June. This should normalize by FY22.

-

Revenues have normalized by FY23.

-

There is a virtual monopoly of the company in the publishing business in Maharashtra and Gujarat state board schools.

-

There are approx. 24,000 CBSE schools pan India. But there are more than 24,000 state board schools in Maharashtra itself and new schools keep opening every year to pick up on the schools that have shut down.

-

And the students of Maharashtra and Gujarat schools are captive customers as they are dependent on the books and guides published by the company for exams.

-

Plus, there is high competition in the CBSE space among publishers and to add to that schools have themselves started publishing their own books.

-

On the ed-tech front, the company is venturing into the field and leveraging the long old relationships it has established with the schools to get the product rolling.

-

But the argument against the significance of the company’s core business (publishing and stationary) does not hold up. The reason being, the amount of fees charged by the darling ed-techs (Byjus, Unacademy) is more than the fees of the state board schools (where the company has a monopoly). The parents cannot afford these exorbitant fees charged by the ed-techs.

-

Update FY24- Massive correction in valuation of Byju’s.

-

Plus, the ed-techs are not officially affiliated to any Education Board, while Navneet’s books and guides strictly follow the prescribed curriculum. And the experience and expertise of all these years in the business is an intangible asset which translates into the brand name.

-

The company witnesses a more than normal revenue and profit growth once in every 4-5 years when the syllabus is changed and students buy new books. This will be the case in the next two years on account of the New Education Policy.

-

The company is also trying a pilot project where it will also sell books through its website in a digital medium which if successful will reduce the capex as no physical copies have to be printed. Update – Seems unlikely.

-

Update – Company has 20% stake in K12 Techno valued at 800 Cr as of Q2FY24.

Some Numbers…

Key takeaways from my crunching of the Annual Reports (not from Screener)

-

Current valuation (as of 04/02/2021) is almost equal to the revenue.

-

Current Ratio>2

-

Negligible Debt

-

ROE & ROCE>20% (presence of moat/competitive advantage as suggested above as a monopoly in Maharashtra and Gujarat).

-

Intrinsic Value based on DCF of Owner Earnings,

Where Owner Earnings = (Net Profit+ Depreciation&Ammortization – Capex)

Note: did not take working capital changes into account while calculating owner earnings.

Discount rate – 10 Yr G-Sec yield.

Intrinsic Value= 4500-5500 Cr

Update- Could be significantly higher if company unlocks value by selling 800Cr stake in K-12 Techno. Management would think about it in coming 2 years.

- Margin of Safety >50%

- Probable correction of mispricing Q4FY22-Q2FY23 with opening up of schools and syllabus changes which will also give a boost to the ROE and ROCE. Update- Current market cap (September 2023) around 3100 Cr.

- Recommendation – Buy at 3100 Cr levels as well despite run-up in price as Board is highly vigilant as they cracked down on loss making ventures and Management (Gnanesh Gala,MD) is honest about headwinds and tailwinds alike and wants to create minority shareholder value.