I use the Artos app and it provides overall as well as individual XIRR.

Posts in category Value Pickr

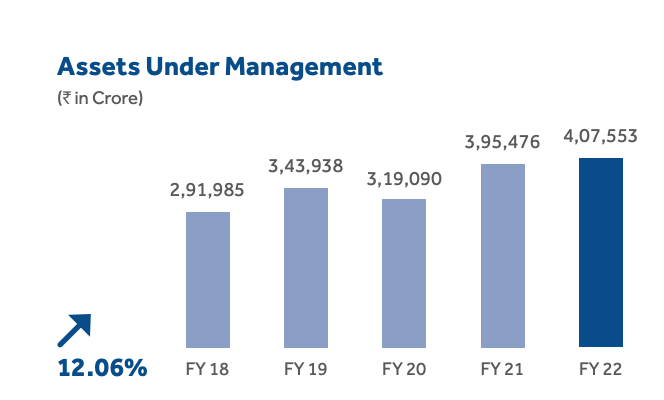

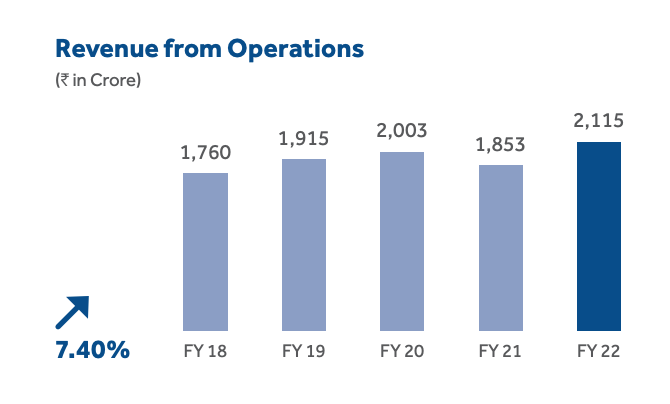

HDFC Asset Management Company (06-12-2023)

Rising Equity AUM might not benefit AMC players if there is relentless pressure on margin via competition from new entrant, passive equity investments and regulatory cap on fees.

With fintech startups, investing in overseas market is becoming easier. So rising allocation of Indian investor’s equity portfolio will also go to overseas asset manager offering cheaper passive investment options.

HDFCAMC AUM hasn’t done that great over last 5 years and revenue growth is even more disappointing. When starting valuation has sky high, stock returns might be very different than performance of the underlying business.

There is a limit for improving profits when business is not generating good revenue growth.

Hazoor Multi Projects Limited (06-12-2023)

There are too many red flags in this company. Be cautious.

Wonderla Holidays (06-12-2023)

Thank you for the crisp summary @shyamdsundar. I have a couple of doubts:

- Do you think the increasing capacity in existing parks can increase the footfall in the park?

- I am not sure how margins would improve if new parks are added as they are totally independent of each other. Each park will have its own staff, equipment, maintenance, etc.

Wonderla Holidays (06-12-2023)

Thank you for the crisp summary @shyamdsundar. I have a couple of doubts:

- Do you think the increasing capacity in existing parks can increase the footfall in the park?

- I am not sure how margins would improve if new parks are added as they are totally independent of each other. Each park will have its own staff, equipment, maintenance, etc.

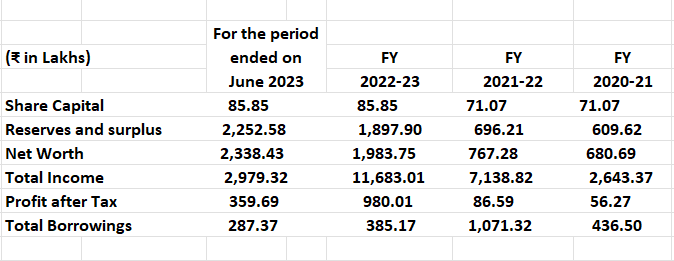

Amic forging limited – sme (06-12-2023)

Thanks for the write-up here, Do you think they will be able to sustain the growth that they have shown to date?

Also, could you identify the reason behind the sudden growth in the margins just before the IPO?

Amic forging limited – sme (06-12-2023)

Thanks for the write-up here, Do you think they will be able to sustain the growth that they have shown to date?

Also, could you identify the reason behind the sudden growth in the margins just before the IPO?

Amic forging limited – sme (06-12-2023)

AMIC FORGING LIMITED

Listed @ 251.35/- on 06.12.2023

IPO Size – 34.80 crs

Fresh Issue – 27,62,000 shares

Cap Price(IPO) – 126/-

3M Profit – 3.5 cr

(June Quarter)

2024 Profit = 3.5cr *4 = 14 cr

(Assumption)

EPS = 13.34

Post IPO P/E = 9.5

(Based on 2024

Profit Assumption)

The company is a manufacturer in forging industry and is engaged in manufacturing of forged Components catering to various industries. They manufacture precision machined components as per customer specifications and International Standard catering to the requirements of various industry such as Heavy Engineering, Steel Industry, Oil & Gas,Petrochemicals, Chemicals, Refineries, Thermal Power, Nuclear Power, Hydro Power, Cement Industry, Sugar and other related industries.

The company is planning to expand via backward integration with starting the manufacturing of Steel Melting & Ingot Casting. This backward integration would increase our product base and also increase our output due to easily availability of raw material.

The company is also planning to pursue forward integration to change the grain size, refine its magnetic and electrical properties to increase the resistance against corrosion as well as against wear and tear. For that, they propose to set up state of art heat treatment plant which is capable of normalizing, annealing volume hardening and flame hardening, etc

FINANCIALS

Promoters –

- Mr. Girdhari Lal Chamaria

- Mr. Anshul Chamaria

- Ms. Manju Chamaria

- Ms. Rashmi Chamaria

Product Range-

Rounds, Shafts, Blanks and engineering spare parts like Gear Coupling Hub, Round and Flange.

Definitely go through website of the company for further information on products-

https://amicforgings.com/

Clientele-

JSPL, TATA Steel, L&T, Phooltas and many more

Strengths –

- Experienced Promoters

- Integrated Manufacturing Facility

- Brand Positioning

- Quality Assurance

Risks –

- High working capital requirements

- Highly Competitive industry

- Invested in shares of HFCL Ltd worth Rs 3.24 cr.

Market value as on June 2023 is Rs 2.45 cr

Hitesh portfolio (06-12-2023)

You might want to go through the following write up…

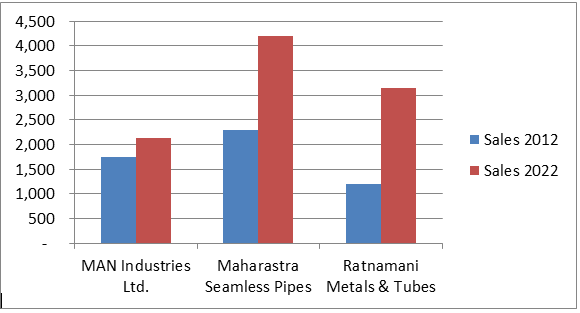

Man Industries a revival in progress (06-12-2023)

Brief Introduction:

The Man Group was promoted by the Mansukhani family in the 1970. It is a diversified group with its flagship company Man Industries (India) Ltd incorporated in 1988. The Company is engaged into manufacturing of Line pipes, Core Carbon Steel LSAW & HSAW Pipes, API grade ERW Pipes, Seamless Stainless Pipes & Steel Bends & Connectors.

The Company has two facilities at Anjar, Gujarat & Pithampura, Madhya Pradesh totaling 10 MTPA per annum equally distributed between LSAW & HSAW Pipes and recently company has commissioned 1.25 Lakh Tons API grade ERW pipe manufacturing facility. The company has recently declared its foray into Seamless Stainless Steel Pipes manufacturing with capacity of 20,000 tons per annum.

Brief History:

The Company has a history of poor corporate governance due to promoter disputes regarding ownership/Title rights to shares & Acquisition of shares during closer of trading window. The company has two promoter groups mainly JCM group & RCM group. The Bombay High Court has given the statement in favor of the company and currently RCM Group heads the company.

Rationale Behind:

- The Company is doing a Capex of around Rs. 170 Crores in setting up API Grade ERW pipe manufacturing facility, Rs. 800 Crore Capex for Seamless Stainless Pipes & DFT technology Pipes & Rs. 75 Crores Capex for Steel Benders & Connectors totaling to Rs. 1045 Crores. Whereas the entire capex in the last decade from FY12 to FY22 was Rs. 403 crores hence, the current capex program is 3x the capex done historically.

- Our Take on the company earlier had internal family & promoter disputes but that doesn’t translates into lack of integrity secondly the company faced governance issues primarily related to procedural violation of security laws but, no money was siphoned out of the company.

- The current promoter group is making serious efforts to rebuild the image of the company by engaging in quarterly concalls giving raw explanations regarding the historical disputes and timeline by which it will be solved

- The Company’s has forayed into value added products that are high margin products which will help company to improve its EBITDA margins (%).

- The Company’s traditional business of SAW pipe manufacturing is not a very attractive business & the industry suffers from over capacity plus the ROE for last 10 years has been 10% & MAN industries is also not a industry leader in it. They are however, expanding into high value growth products.

- The company is available at a relatively cheap price (P/E ratio: 19.5, 6x PAT of FY24e) which offers good safety of margins to us.

- The Natural gas pipeline sector in India is going through structural transformation and is facing strong industry tailwinds as India intends to increase the share of natural gas in energy mix to 20% from current 6% by year 2030.

- The government also Target to increase the pipeline coverage by ~54% to 34,500 km by 2024-25 and to connect all the states with the trunk natural gas pipeline network by 2027.

- Capex under City Gas Distribution Scheme, Nal se Jal Mission, Jal Jeevan Mission & National River Linking Scheme are further providing strong tailwinds to the sector & LSAW & HSAW pipes are widely used for water transportation.

- The SBI lead consortium has supported Company’s expansion plans by granting them working capital & long term debts for their ERW plant they also conducted special audit on the company, they wouldn’t have granted the loan if they would have found siphoning of the fund it is to be noted that the current loan has been sanctioned to the company after the Forensic audit conducted by SEBI & transaction audit conducted by SBI led consortium.

MAN Historical Growth has been Poor:

- MAN lost almost a decade due to internal promoter & family disputes

- Over the last decade from FY12 to FY22 total cash generated from operations is Rs. 1562 Crores only Rs. 403 Crores were invested back into business.

- The company lost the market share and order book to the competitor leading to lack of growth & expansion.

Expectations of the Management: - The Company aims to have sales of Rs. 5000 crores or more by FY 2025-26 & growth of 20% CAGR in revenue from now.

- The company targets EBITDA margins in the range of 11-15%

- The company has an order book of 13,000 crores as on this date and expects conversion rate of 20-25%

- The company aims to expand revenue from ERW pipe, Seamless Steel Pipe Sale to Rs. 1700 Crores

- Expects sale of Rs. 200 Crore from ERW pipe sale in the current year

- The Stainless steel pipe plant will become operational from Q1FY24 & start full fledges production from Q2FY24.

Concerns for the company: - ERW pipes & Seamless Stainless Steel Pipes is a new sector for the company & does not have existing relationships with clients in this sector

- The Company derives majority of its revenue from Oil & Gas industry and even today the capex of this industry is linked to oil prices and the sector goes through cyclical in nature.

- The Company has contingent liabilities worth Rs. 406.33 Crores & Disputed Debtors worth Rs. 95.20 Crores however; the company has given guidance that the company will be able to recover the amount.

- The promoter groups have dispute regarding right to receive dividends of Rs. 4.45 Crores however; the Bombay high court gave decision in favor of the company and the JCM group has further challenged it in Supreme Court of India.