Interesting, it makes sense now. High margins, high ROCE.

But why go public? They could have done this without going public.

Interesting, it makes sense now. High margins, high ROCE.

But why go public? They could have done this without going public.

Can you share the data where you read this?

I have personally talked with management and one of my friend visited the plant. No company is perfect. If everything is rosy, I never invest. I like some negative points and some negative sentiments about the company.

Stock_XIRR_Calc.xlsx (10.7 KB)

i use attached excel based XIRR calculation. each day buy(positive value) and sale(negative value) is added along with date, Current Total value (negative) is used in the end,

to computed XIRR.

Paul Merchants Limited is an conglomerate providing various services such as Forex, International Money Transfer, Tour & Travels, and Business Payment Solutions. Paul Merchants through its 100+ branches serves thousands of customers PAN India, on daily basis.

Paul Merchants Finance Pvt. Ltd. Wholly Owned Subsidiary of Paul Merchants Ltd offers easy loan against your gold helping you live your dreams and fulfil your needs. The Paul Merchants gold loan service is not only easy and quick but also benefiting as the loan is served to the customers against the market value of gold at attractive and low-interest rates.

FOR GOLD LOAN BUSINESS

https://paulmerchantsfin.com/branches.html

PAUL MERCHAT LTD IS A UNDER VALUE + GROWTH STOCK

STANDALON QTRLY REVENUE RS.1799 CR

STANDALON QTRY PROFIT RS 7.56 CR

STANDALON QTRLY EPS RS.73

LOOKS VETY THIN MARGIN BUSINESS BUT THIS MARGIN IS CASH PROFIT

HOWEVER LOOKS CONSOLIDATED NUMBER WHICH INCLUDE GOLD LOAN BUSINESS

CONS. QTR REVENUE RS 1839. CR JUST 40 CR MORE THEN STANDALON

CONS. QTR PROFIT RS 15 CR DOUBLED

CONS QTR EPS RS 141

VERY TINY EQUITY JUST RS. 1CR 74.66 % PRAMOTOR HOLDING LOW FLOAT SHARE

INTERESTING PART IS

TOTAL GOLD LOAN BOOK AS ON 30TH SEPT 23 RS.873 CR

TOTAL LOAN TAKEB CY PML RS.442 CR

GOLD LOAN GIVEN BY OWN FUND RS. 431 CR WHILE MCAP RS.343 CR AS ON

5.12.23

COMPANY INCREASE AUTHORISED CAPITAL ALMOST 5 FOLD AND ANNOUNCE 2:1 BONUS ISSUE MEANS 1 CR CAPITAL INCREASE TO 3 CR SO IN FUTURE COMPANY MAY BE RISE MONEY THROU PREFRENCIAL OR ANY OTHER WAY

SUBSIDIEARY COMPANY PAUL MERCHANT FINANCE PVT LTD ANNOUNCE TO RISE 30 CR BY SECURED NON CONVERTIBLE DEBENTURE COMPANY DONE BRNACH EXPANTION IN LAST TWO YEAR MEANS OPEX DONE NOW RESULT WILL BE COME

FOR DETAILS OF BRANCH EXPANSSION PLEASE VISIT COMPNY’S TWITTER PAGE OR FACE BOOK PAGE

THIS ALL DETAILS ARE JUS EDUCATION PURPOSE DON’T DESIDE TO INVEST ON THIS DETAILS DO OUR OWN STUDY

Promoters infusing money at a higher price compared to QIBs. Good Corporate Governance

4e1d0483-e38d-4575-946f-07fcbf4ddd5c.pdf (251.3 KB)

Well I think …the most important negative point missed is the employee costs and revenue multiple…

I read somewhere that this was huge and doesn’t seem to fit as per the corporate standards…

Whether semiconductor uses any magic to create products then it’s a different take …happy investing:-)

Stock increased more than 6% today with high volumes. Seen other stocks from paper industry too increasing 3-4%. Any specific news on stock/sector?

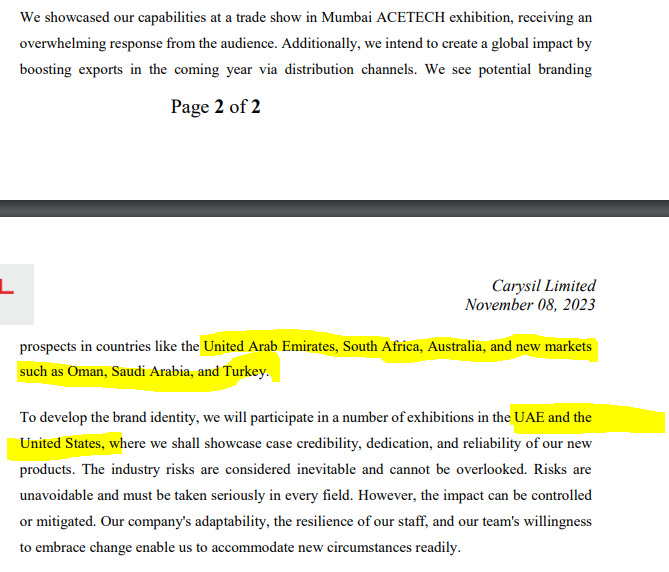

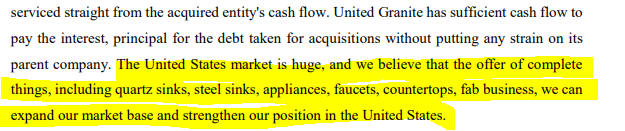

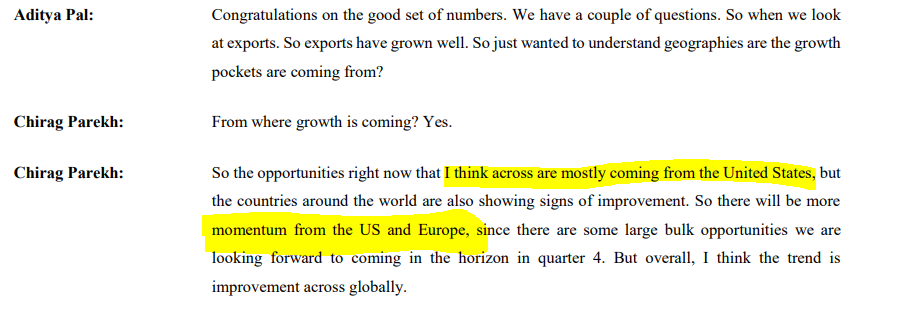

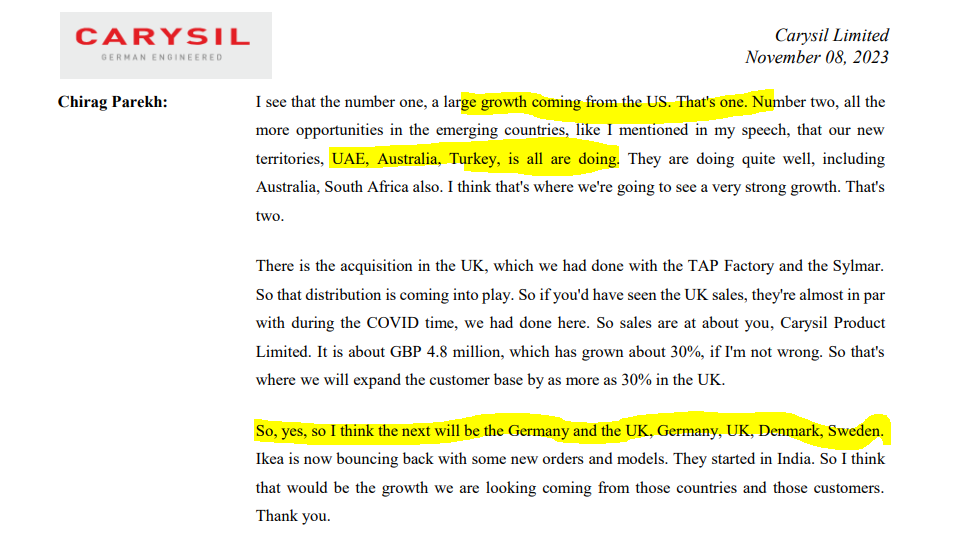

For H1-24 revenue from exports is around 78.4%. There is no individual country specific breakup but based on management commentary it was mostly from Europe and they are focusing on other countries USA, UAE, Turkey, South Africa, Australia going forward. USA is going to be a bigger market for them. We can probably ask management about the region level distribution.

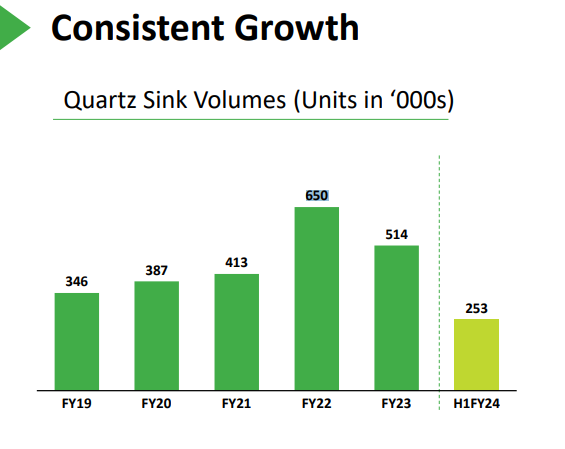

>>Close to 50% of revenues are generated from the sale of Quartz kitchen sinks although revenues from this product are down from 650K in FY22 to 514k in FY23

I think this is volumes and not revenue.

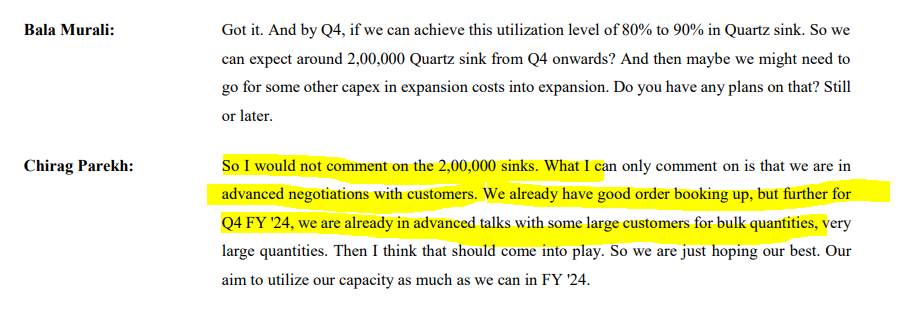

There is a slowdown in demand in FY23 due to the Russia-Ukraine war and slow down in US due to recession caused the volumes to go down. Management talked about this and expecting this number to go up in coming quarters. H124 volumes are 2.53L and this what management says for doing 2L per quarter from now on, they are in advanced stages for getting orders for large volume in q4 fy24.

sir,ur view in agi greenpac can this company give 20% gr next 2 yr.and the current valuation is good to go.

Since i have similar number of names…

1.Large numbers does become difficult to track & take a convinced bets…however i found it okay so far in my short journey…u may like to study more on ideal numbers ?

2.I did invest consistently for about an year on monthly weeekly basis without selling…but i realized it blured my visibility for individual names in PF…and i found i was like sprinkling for gardening purpose without a logic and qithout much to gain…so i found limited number of names can help us stop investing surplus without return visibility.

3.I would consider taking a loss is very very necessary ![]() …you shall notice on this forum “taking a loss is part of investing journey…do not get married to a particular name”

…you shall notice on this forum “taking a loss is part of investing journey…do not get married to a particular name”