The bird flu season in Japan typically begins in October each year.

Since mid-October, three HPAI outbreaks have occurred across Bulgaria.

The bird flu season in Japan typically begins in October each year.

Since mid-October, three HPAI outbreaks have occurred across Bulgaria.

Thanks for sharing!

As they say about IPO – “it’s probably overpriced” ![]() .

.

This time I also applied for the first time for an ipo for tata technologies but didn’t get the allotment, but I guess whatever happens, happens for the best ![]()

Interesting boardroom drama.

Forbes covered the story so far on 24-Nov-23.

Briefly, the company has had no promoters since the Singh brothers were convicted.

A board of independent directors has been in charge.

The Burmans want to take control and have made an open offer to get their holding above 26%. But the board is resisting. They think the offer price of Rs 235 per share is too low. Timing is ‘fishy’ says Religare board member Hamid Ahmed. The board appears to allege collusion between the Burmans and the Singh brothers.

There are countercharges of failure of corporate governance and excessive remuneration at the company. See deepuji2008’s post above.

Kedara Capital, the PE fund, holds 16% of Care Healthcare which is the flagship subsidiary of Religare Enterprises. Kedara came out with a statement supporting the Care management.

But the regulator is asking questions about the ESOPs.

Interesting interview with Mohit Burman on CNBC.

Once the regulators approve the open offer, this could resolve quite quickly with the Burmans in control and the current board out. Or could this end up in the courts and get dragged out?

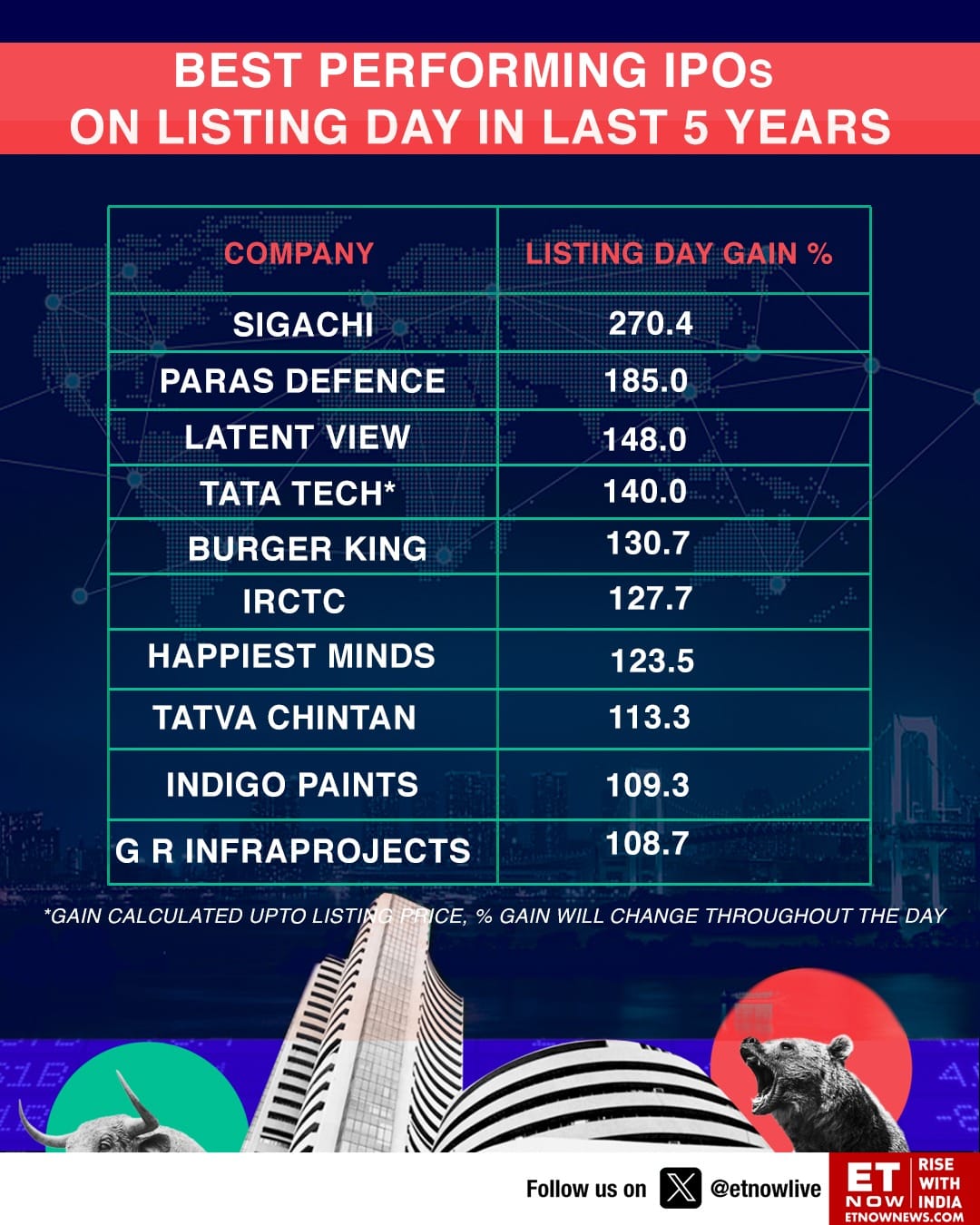

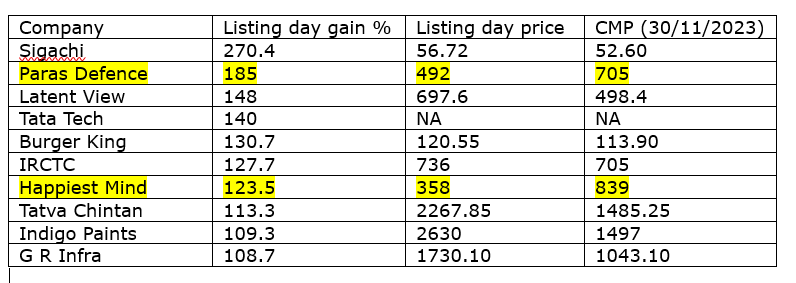

ETNow post on top best performaing IPOs in last 5 Years

Out of 10 – eight (8) are underperforming the day they listed.

There is high level of euphoria of Tata Tech with retail investor. My way to check data. i wish this reach to individual investor.

No I got it, I was corresponding to that only. They can be concentrated because they have all these other sources of earning income. Something which they control and transfer from Net Income which belongs to all shareholders.

My point was more towards concentration of networth of promoters, not much related with related party transactions or commission or salary of promoters.

In my Aug’22 post I was expecting the price to double in 4 years, price then was around 325. From that time there has been over 50% price appreciation to cmp of 500+.

Considering H1 results, and expecting the company to post similar performance in H2, there could be a 20%+ growth in profit from FY23 level. And assuming the PE level to be similar as now, that doubling of price from Aug’22 levels could be achieved by May’24 itself. But if there are negative surprises, like higher receivables, or write offs, or any technical issues wrt to WTE plant hampering its ramp up, or any other unpleasant development, the price will correct, and will follow the earnings trajectory.

Disc: invested, biased.

Growth is still better than other FMCG companies. IF you look at their high growth business e.g. nourishco, soulful,pulses etc. you will realise that business has high growth potential. No doubt it is over valued and it is tough to get exponential returns but long term story is still intact.