There was no substance in the ED raids. They were just perpetrated by some vested interest to tarnish the name of the company. Some local guy from the same village who had a grudge or maybe plain black mail. More than the regulatory actions what is worrying is if the company is run professionally. looks the the recent issue where an employee siphoned off more than 20Cr. Are systems in place to take care of these kinds of issues? As I see it the whole company is being run on Nandakumar, who is an honest man who built the company from scratch but who not young anymore. Though his daughter is brought on board, she needs to prove herself

Posts in category Value Pickr

Hyundai Motor India Limited – HMIL (16-10-2024)

Why are Hyundai’s promoters launching the largest IPO in Indian history?

The primary reason is to take home more than $3 billion. This is a 100% offer-for-sale issue, meaning no funds are being raised for business expansion or working capital. The promoters are merely reducing their stake.

They plan to raise nearly $1 billion from anchor investors, who will have a lock-in period of 30 days for 50% of their holdings and 90 days for the remaining 50%.

That’s one aspect of the story.

The second part is that the IPO is priced at a reasonable P/E ratio of 26, which is moderate and not overly expensive.

Given this scenario, where the IPO comes at a fair valuation but is purely an offer-for-sale with no funds allocated for growth, there’s a good chance that anchor investors might exit once their lock-in period ends.

These are just key points to consider, not a recommendation to apply or skip the IPO.

I personally will wait for its listing and see couple of quarterly results. Wont be bate of FOMO.

XIRR Calculator for your stock portfolio (16-10-2024)

Hi @Abhijith_P ,

Many thanks for posting this ![]() . I was actually looking for for an XIRR and portfolio tracking tool. Kudos for the great work .

. I was actually looking for for an XIRR and portfolio tracking tool. Kudos for the great work .

Had couple of queries :

-

How do you find the Tickr symbol for BSE only stocks and some SME stocks. I was not able to use the get the google finance function to work in some of the portfolio stocks like (Advait Infratech, Annapurna Swadist, Frontier Springs etc.).

-

Is there an option to pull Sectors also from Google Finance. Was not able to find the query for the same.

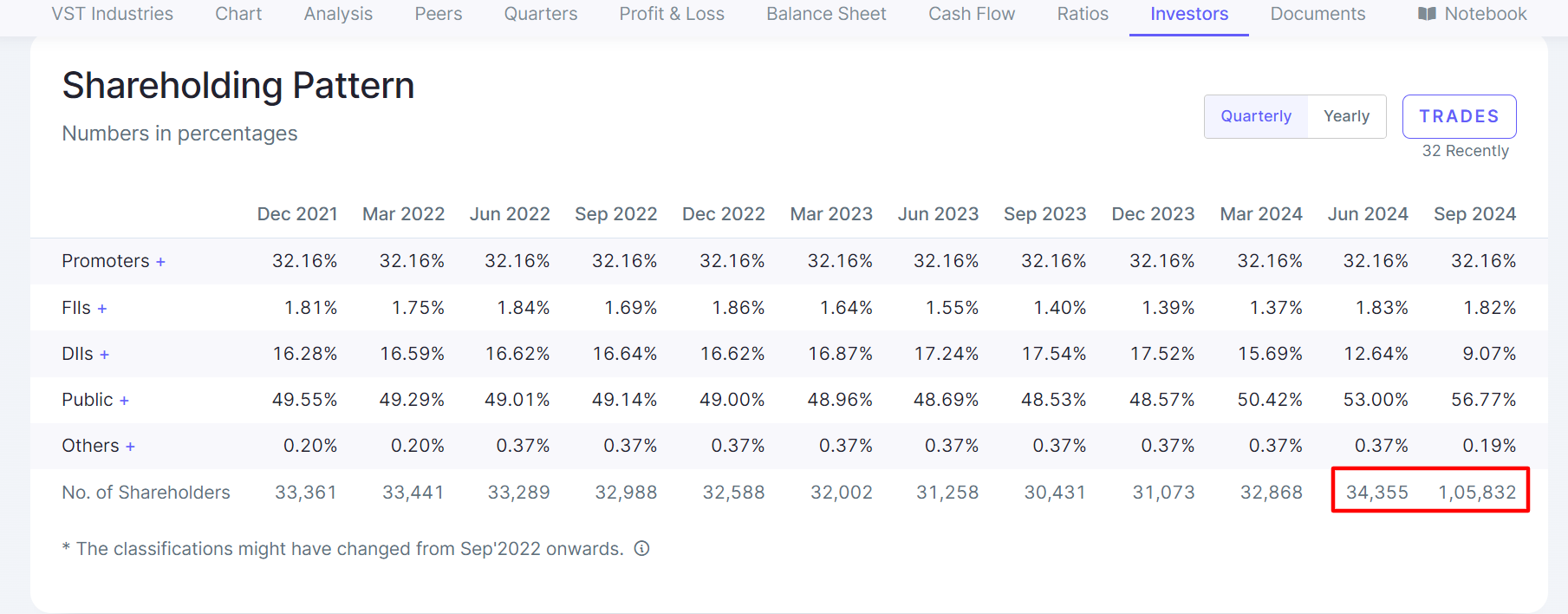

VST Industries: Puff full of power? (16-10-2024)

The total number of shareholders has increased significantly in the last quarter. What could this possibly mean.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (16-10-2024)

Compared to other Private banks, KMB has more potential to do value-unlocking, and given the fact, the increase in the affluent class, KMB poised to do well, although compounding at 25% for a decade is day-dream, 5-7 times in a decade should be their trajectory, yes I would agree no large company can grow beyond country GDP(unless export), India itself will grow 6-8%, and KMB themselves are not in top 3 or even top 5 for that matter, so I would say they are not systematically important bank yet.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (16-10-2024)

My comment was “Stock wont’ double every 3-4 years” which incidentally is what I said in 2021 about it. ![]()

So yes it may double from here in 3-4 years (and this time I’m fairly confident) given its long underperformance. But then whether it will keep doubling every 3-4 years is anyone’s guess as it will translate into 18-24% average return every year in stock prices. And for large banks it’s very difficult to grow stock prices at double the rate of gdp unless there is significant rerating of valuations.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (16-10-2024)

i partially disagree, although long term compunding should be somewhere around 18%, given the underperformance for almost half a decade, we should easily see it double in next the 3-4 years

Screener.in: The destination for Intelligent Screening & Reporting in India (16-10-2024)

Hey, Can somebody pls explain the reliability of the both formula for the Forward PE calculation , because sometimes using the EPS latest quarter can can produce misleading Forward PE because of exceptional income (or any spike in income bcz of exceptional items). And also using the latest quarter EPS may not depict the true picture in case of cyclical industries. So can we use the average EPS growth rate instaed ?

Formula 1 :

Forward PE = Current price / (EPS latest quarter * 4)

Formula 2 :

Forward PE = Current price / (EPS((100+EPS growth 3Years )/100))

Thanks

Manappuram Finance (16-10-2024)

oke lots of pessimism back in the company… Enough for me to reenter this… Had exited on ED raids… they have come clean…

Disc: Invested 180