Just curious, since u r invested from 10 years in NMDC, why your handle has the name newbie? You seem to be a seasoned investor.

Posts in category Value Pickr

Mrs Bectors Food Specialities: Can it beat the industry? (25-11-2023)

Thanks a lot for this insight really feels like company management walks the talk.

Mrs Bectors Food Specialities: Can it beat the industry? (25-11-2023)

Thanks a lot for this insight really feels like company management walks the talk.

Edelweiss Financial Services (25-11-2023)

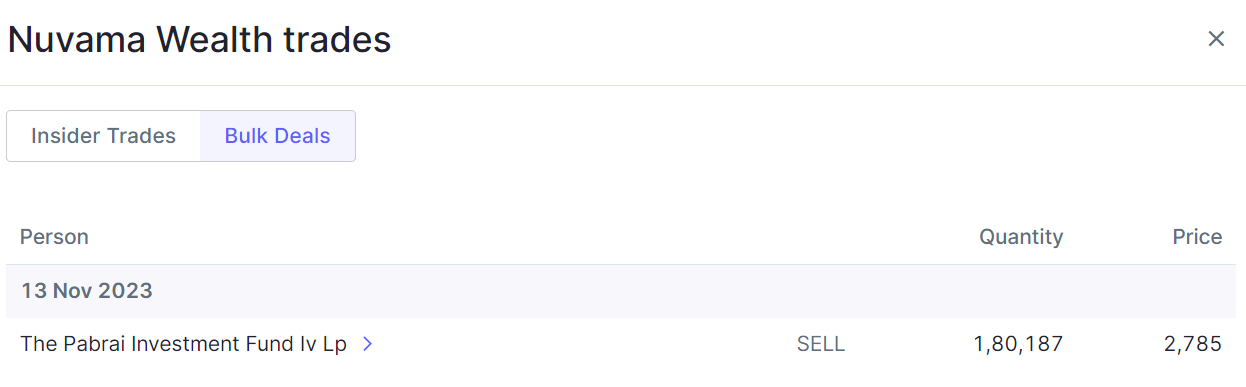

Pabrai funds sold Nuvama shares on 13th Nov

All were saying he was interested in wealth management business- but I think as valuation were high and as a value investor he exited.

Investing Basics – Feel free to ask the most basic questions (25-11-2023)

One thing i realised while calculating XIRR of total portfolio using weighted average method of individual stocks XIRR given by zerodha…is they obviously dont give XIRR of those stocks which we have completely sold and currently not part of the portfolio. So an investor have sold many stocks in past, which doesnot form the part of his portfolio currently, then his XIRR of portfolio will be wrong.

Investing Basics – Feel free to ask the most basic questions (25-11-2023)

From console, you can put exact date and get account value on that particular date.

Praveen’s Information Attic (Obervations, Lessons, Thoughts) (25-11-2023)

I am not sure how much sense that list makes. Is the list comparing apples to oranges? Different investors have different times of entry into a particular stock. A company that gives zero or negative returns to one investor could be a multi bagger for a different investor based on when they bought the stock of the company.

Also, I find that investing in a “good” company that hasn’t gone anywhere for a long period of time has yielded good returns as long as the company’s fundamentals hadn’t changed. A good example is Wonderla Holidays. I remember it was at 350 levels then it went nowhere for sometime and then went to 100 levels during covid and now is trading at 900 levels. Same goes for a company like NMDC although I have been in it for 10 years now for a little better than FD level returns. ![]() I think eventually it will pay just to stick to a good company for a long time.

I think eventually it will pay just to stick to a good company for a long time.

One psychological mistake I have to constantly fight back, in my case, is that I want the stocks I invest in to go up sooner. However, in the markets, some stocks take 1 year and some take 10. Some stocks go up in 1 year by 1000% and then goes nowhere for 10 years following that and then might go up again by another 500%. If we don’t stick to a company long enough, we will never find a 100 bagger!

Companies build value by reinvesting internally or in other businesses. Markets take their own time to give a correct valuation (or inflated valuation). As the accomplished value investors have shown us, we just have to keep searching for dollars available for cents. Our entry price matters a lot but so does averaging. Many times, we buy into a stock and stop buying when the same stock becomes a better deal.

Coming back to the list, most of the companies in the above list are multi baggers and market leaders. Looks like a good list for stock picking. Sometimes it seems like we can find value exactly in these type of stocks because they seem to be going nowhere.

Pitti Engineering Limited: Is it on an inflection point? (24-11-2023)

Pitti Engineering Conall Notes Q2 FY24

Highlights:

- Sales Volume:

- Up 17.38% YoY to 10,340 tonnes.

- Revenue from Operations:

- Quarter revenue: 290 Crores.

- 4.56% decrease due to material price reduction passed on to clients.

- Record EBITDA:

- Highest-ever at 42.56 Crores, up 16.44% YoY.

- Government Incentive Impact:

- Maharashtra government incentive: 10.9 Crores.

- Boosts net profit to 22.55 Crores.

- Capacity Utilization:

- Lamination: 72.27%.

- Machining: 91%.

- Order Book Strength:

- Robust at 716 Crores as of September 30, 2023.

Incentives and Revenue

- FY2023 Recognition:

- 10 Crores realized this quarter.

- Categorized under “other income.”

- FY2024 Projections:

- Anticipated 30 Crores in Q4.

- FY2024 incentive: 34 Crores.

- Recognition annually in two tranches.

- Crediting typically takes 6 to 8 months from sanctioning.

Capacity and Business

- Capacity Increase:

- QoQ increase from 50,200 to 56,000 MT.

- Next increase planned in March 2024 to reach 72,000 MT.

- Volume Targets:

- Q3 target: 10,500 tonnes.

- Q4 target: 11,000 tonnes.

- On track with annual target of 42,000 tonnes.

- Overseas Business – Europe:

- Recent breakthroughs in Europe.

- Expecting Rs. 100 Crores revenue in FY2024-2025.

- Growth from wind turbine and marine businesses.

- Outlook:

- Positive three-year outlook for Europe.

Raw Material, Contracts, Railway Business, and Guidance

- Raw Material Prices:

- Current quarter: Rs. 90,000 per MT.

- Year-ago: Rs. 1,15,000 per MT.

- Next two quarters expected to be stable.

- Price Correction and Contracts:

- Prices stable; no need for reduction.

- Contracts have quarterly Price Variable Clause.

- Railway Opportunity:

- 8,000 MT lamination sold annually to railways.

- Machine components: 70% of overall business.

- Annualized revenue: Rs. 400-500 Crores.

- Potential increase: Rs. 200-250 Crores in the next years.

- Capex and Revenue Guidance:

- Capex: Additional Rs. 120 Crores for the year.

- Revenue guidance: Around Rs. 1,100 Crores, extrapolating from Q2.

Capacity

- Capacity Utilization:

- Current: 56,000 MT, scaling to 72,000 MT.

- Current utilization: 71%.

- FY2025 sales target: 48,000 MT (66% utilization).

- FY2026 sales target: 56,000 MT (80% utilization).

- Future Capacity Plans:

- No plans beyond 72,000 MT.

- Further plans based on market progress.

Order Book, Demand, and Subsidiary Merger

- Order Book and Demand:

- Short-term order book flat, marginal Q4 increase.

- Longer-term impacted by depleting 10-year Indian loco business contracts.

- Stable demand; cautious outlook due to elections.

- Strong order books in North American and European markets.

- Direct Exports and Margins:

- Strong growth in direct exports.

- Margins similar, depending on value add.

- Subsidiary Merger:

- Approval received from stock exchanges and SEBI.

- NCLT application in progress.

- Merger expected by March 31st, 2024.

European Business, Green Energy, and EVs

- European Business:

-

Lamination Business:

- Competitors from Europe and China.

- European manufacturers shifting orders to Asia.

- Companies prioritizing supply chain diversification.

-

Machine Components:

- India slightly more expensive than China, but customers derisking from China.

- Green Energy in Europe:

- Demand from green energy sectors: hydro, wind, green hydrogen.

- New business in marine generators due to emission regulations.

- Electric Vehicles (EVs):

-

Current Status:

- Two customers in two-wheelers.

- Seven clients in three-wheelers, buses, and off-highway vehicles combined.

- Slow start in EV component demand; imports from China.

- Unorganized market retrofitting EVs gaining traction.

-

Future Outlook:

- Major OEMs expected to enter manufacturing in 3-4 years.

- EV component market potential around 1,00,000 tonnes.

- Company poised for growth in this sector

Margin Outlook and EBITDA Projections

- Current Margin Profile:

- EBITDA per tonne at 42,000 for the current half-year.

- Anticipate an increase to 43,000-43,500 by Q4.

- Future Margin Trends:

- Continued rise in machine components contribution.

- Blended EBITDA per tonne expected to reach 45,000 for FY2025.

- Factors for Change:

- Increased machining capacity deployment.

- Positive impact from the proposed merger.

Turnover, EBITDA, Acquisitions, and Private Capex

- Turnover and EBITDA:

- Plain components: 100 Crores revenue annually.

- Machining-related components: ~200 Crores.

- Anticipate doubling in 2-3 years with increased machine capacity.

- Private Capex:

- Healthy demand observed among clientele.

- Government capex ahead but strong private demand.

- Private capex remains robust compared to the previous year.

- Future Expectations:

- Continued growth in private capex anticipated.

MNC Customers, Supply Chain, Joint Ventures

- Joint Ventures Opportunities:

- Existing MNC relationships.

- Supply chain realignment opens joint venture possibilities.

- Initial focus on specific railway bill of materials.

- Expansion Constraints:

- Current focus on execution and steep targets.

- Constraints due to capital and managerial bandwidth.

- Prioritizing current commitments, merger, and machine components opportunity.

- Strategic Approach:

- Concentrating on present commitments before new ventures.

- Excitement about machine components opportunity.

- Delay in targeting certain locomotive interior components for potential joint ventures.

- Revenue from European Opportunity:

- Anticipated 100 Crores revenue.

- Mix of machine components and high-level assembly.

- High margin business, applicable even in the Indian market.

Strategic Focus and Market Expansion:

- Major Contributors:

- Railways, power, and industrial segments key to top-end growth.

- Power includes data centers, DG sets, hydro, thermal projects, wind turbines, and generators.

- Industrial spans diverse sectors other than Railways.

- Target Industries (Two-Year Perspective):

- Focus on renewable energy, mining equipment, automotive, and appliances.

- Aiming to increase market share in appliances and automotive.

- Client Relationships:

- Major supplier for Cummins in India.

- Open to global opportunities but not the sole supplier.

- Uncertainty on future India-Europe supply chain dynamics.

Portfolio of a novice investor (24-11-2023)

Added one more criteria in my checklist (reverse DCF):

Portfolio of a novice investor (24-11-2023)

I tried using ValueResearchOnline platform to calculate XIRR of my holdings. As I mentioned, since I have 3 demat accounts, it was a pain to calculate the XIRR of my portfolio especially for my Sharekhan demat accounts (I have 2 of them).

One word of caution if someone is trying to upload his / her portfolio in VRO platform, please take care of the bonus / split shares as sometimes it gets messed up. I manually adjusted those bonus and split shares that I got in last 10 years before I uploaded entire portfolio on the platform.

Here are the results:

- Zerodha account (3 years) – I have started investing in Zerodha account since 2020 and these days I am using only Zerodha to purchase any new stock. Sharekhan is only for selling or applying for IPOs in case of shareholder category. Here is the XIRR for Zerodha account.

- For all demat accounts (> 10 years) – I have started investing journey since late 2012 / early 2013. So, it has been almost 10 years now. Below is the XIRR details of my entire portfolio across all 3 demat accounts (2 Sharekhan and 1 Zerodha):