what is the logic of doing capex of 550 cr having asset turnover of 0.7

Posts in category Value Pickr

Rategain – Fast Growing SaaS Leader (23-11-2023)

any potential names for acquisition?

TARSONS products ltd (23-11-2023)

RESULT Q2FY24 Concall

- EBITDA margin for Q2FY24 stood at 38.3%. This was impacted on account of lower revenue growth and GP margin leading to a negative operating leverage rate, increase in the cost on account of manpower and marketing expenses, which we believe are investments to fuel future growth opportunities

- Commercial production of cell culture and other products is anticipated to start in Q1FY25.

- Radiation & Isotope Technology for this purpose. This strategic move aims to reduce our dependence on a single source in West Bengal.

- Revenue breakup- export sales contributed around 35% and domestic sales contributed around 65%.

- BIS certification issue- raw material supply is getting a lot of problems because of the implementation of one of the concepts called BIS. And the government, obviously, is not allowing all kinds of imports without having that kind of certification.

- Ramp up of new capex- we expect to scale up in 4 to 5 years, completely ramp up to 100% of available capacities.

- Asset turn- 0.7x on 550 cr capex = 350-400cr revenue potential.

- Revenue potential- the existing capacity and the upcoming capacity, we can touch a revenue of about INR700 crores to INR800 crores.

- There would still be a lot of space for future capex.

- 500cr guidance- INR500 crores in FY ’25 looks highly unlikely at this point of time. no new guidance now.

- ESG issue- in some countries, the government banned or limited the usage of plastic because it’s not ESG friendly.

- GST notice- 66lakh

- Inorganic acquisition, which we are looking for in Europe and U.S. kind of countries.

- I dont see anything good happening in the next few quarters, operating deleverage is going to play, so I am exiting with 14% loss.

Rategain – Fast Growing SaaS Leader (23-11-2023)

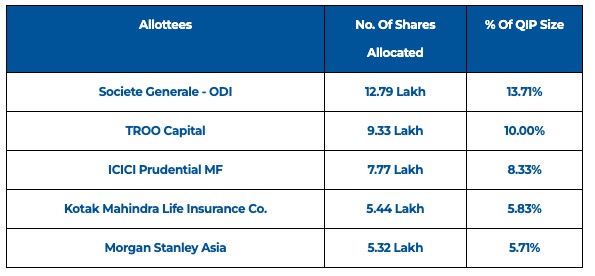

Looks like Societe Generale was allocated ~13% shares from the recently concluded QIP and have offloaded nearly half of their allocation on the first day of QIP listing (As shown in the image below).

Bulk Selling Deal

In my view decoding these actions from the firm might be an act of overthinking, hence we can wait and learn.

Disc. – Invested

Praveg Ltd: Play on Indian Tourism Industry! (23-11-2023)

Timeline of convertion of warrants

Timeline of promoter selling

Promoter is booking profits from warrants.

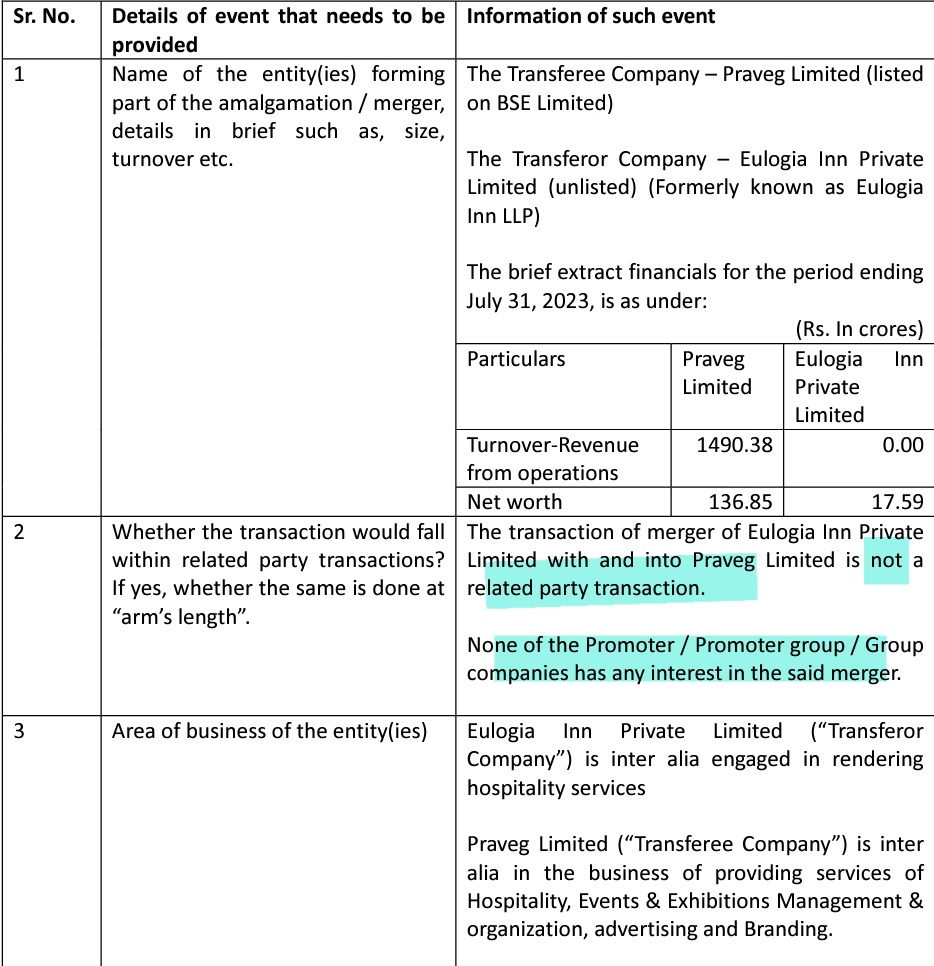

This deal should be called a related party transaction if what you suggest is true.

Ami Organics – Pharma Intermediates & Specialty Chemicals (23-11-2023)

Ami Organics Q2/H1 results highlights –

Q2 results –

Sales – 172 vs 147 cr, up 17 pc

Gross Margins @ 41 vs 48 pc due – steep price erosions in finished products due oversupply from Chinese manufacturers, higher sale of lower margin products. Also, high cost inventory of RM was a head wind

Expecting much better performance in H2 due healthy order book that the company has

EBITDA – 25 vs 28 cr ( margins @ 14 vs 19 pc )

Lower EBITDA margins due – lower Gross margins, higher employee cost due annual increments, hiring for Ankleshwar Unit and ESOPs

Adjusted PAT – 15 vs 19 cr ( without factoring the impairment of JV – Ami Oncotheranostics )

Have signed another contract with Fermion taking the total number of products to be supplied to 3, enhancing revenue visibility for coming years. Commercial production to start from Q4 FY 24 from Ankleshwar facility (validation batches). Have a few more products in pipeline for which manufacturing contracts may materialise for Ami Organics with Fermion and other innovators

One UV Observer – speciality chemical product for paint Industry ( for metallic paints used in Auto Industry ) is scheduled for launch in Q3. The product uses Swiss technology. Validation batches have already been approved

Electrolyte Additives (for energy storage) update – in advanced stages of negotiation of contract with a couple of customers ( first Indian and global company outside China to develop the product ) – product already approved by 6 buyers

Ankleshwar plant to commence commercial production in Q4 ( basically the new 190 cr brownfield capex for advanced intermediates to go live )

Completed acquisition of majority stake in Baba Fine chemicals ( 55 pc stake ) in Q4

Q2 Sales breakup –

Advanced Pharma Intermediates – 134 vs 125 cr

Speciality Chemicals – 38 vs 22 cr (rapid growth due smaller base)

Current manufacturing facilities for advanced Pharma intermediates and speciality chemicals – 03 + 01 R&D facility

59 pc – exports

41 pc – domestic sales

Revenues from top 10 customers @ 58 pc

Cash and cash equivalents @ 104 cr as on 31 Sep

Chinese over supply is not a direct threat to the company. Its just that company’s competitors got cheaper RMs from China and hence the downward pressure on finished products

Company should be back to 48 pc gross margins in next 2 Qtrs

Capex in H1 @ 100 cr. Another 105 cr lined up for H2

Electrolyte manufacturing supply to begin in Q3. Commercial supplies to begin in Q4

Full capacity ramp up of molecules being supplied to Fermion expected to happen in FY 25 – Q3 onwards

Baba Finechem – long term revenue target of 200 cr. Expect exponential ramp up at Baba Finechem from next FY onwards

Aiming to ramp up speciality chemical sales to 2.5 times of current sales in about 2-3 years

Company’s domestic business is mostly spot business. Most of the export business is contract business

Ankleshwar plant has 3 blocks. One of them is Dedicated to Fermion Ltd ( 33 pc of capacity ). This block is fully booked. Other two will be used by the company for business expansion till FY 27

Increase in inventory due build up in anticipation of execution of Fermion contract

Baba Finechem’s H1 sales are 21 cr, PAT is 14 cr !!!

Disc: holding, biased, not SEBI registered

Ranvir’s Portfolio (23-11-2023)

Ami Organics Q2/H1 results highlights –

Q2 results –

Sales – 172 vs 147 cr, up 17 pc

Gross Margins @ 41 vs 48 pc due – steep price erosions in finished products due oversupply from Chinese manufacturers, higher sale of lower margin products. Also, high cost inventory of RM was a head wind

Expecting much better performance in H2 due healthy order book that the company has

EBITDA – 25 vs 28 cr ( margins @ 14 vs 19 pc )

Lower EBITDA margins due – lower Gross margins, higher employee cost due annual increments, hiring for Ankleshwar Unit and ESOPs

Adjusted PAT – 15 vs 19 cr ( without factoring the impairment of JV – Ami Oncotheranostics )

Have signed another contract with Fermion taking the total number of products to be supplied to 3, enhancing revenue visibility for coming years. Commercial production to start from Q4 FY 24 from Ankleshwar facility (validation batches). Have a few more products in pipeline for which manufacturing contracts may materialise for Ami Organics with Fermion and other innovators

One UV Observer – speciality chemical product for paint Industry ( for metallic paints used in Auto Industry ) is scheduled for launch in Q3. The product uses Swiss technology. Validation batches have already been approved

Electrolyte Additives (for energy storage) update – in advanced stages of negotiation of contract with a couple of customers ( first Indian and global company outside China to develop the product ) – product already approved by 6 buyers

Ankleshwar plant to commence commercial production in Q4 ( basically the new 190 cr brownfield capex for advanced intermediates to go live )

Completed acquisition of majority stake in Baba Fine chemicals ( 55 pc stake ) in Q4

Q2 Sales breakup –

Advanced Pharma Intermediates – 134 vs 125 cr

Speciality Chemicals – 38 vs 22 cr (rapid growth due smaller base)

Current manufacturing facilities for advanced Pharma intermediates and speciality chemicals – 03 + 01 R&D facility

59 pc – exports

41 pc – domestic sales

Revenues from top 10 customers @ 58 pc

Cash and cash equivalents @ 104 cr as on 31 Sep

Chinese over supply is not a direct threat to the company. Its just that company’s competitors got cheaper RMs from China and hence the downward pressure on finished products

Company should be back to 48 pc gross margins in next 2 Qtrs

Capex in H1 @ 100 cr. Another 105 cr lined up for H2

Electrolyte manufacturing supply to begin in Q3. Commercial supplies to begin in Q4

Full capacity ramp up of molecules being supplied to Fermion expected to happen in FY 25 – Q3 onwards

Baba Finechem – long term revenue target of 200 cr. Expect exponential ramp up at Baba Finechem from next FY onwards

Aiming to ramp up speciality chemical sales to 2.5 times of current sales in about 2-3 years

Company’s domestic business is mostly spot business. Most of the export business is contract business

Ankleshwar plant has 3 blocks. One of them is Dedicated to Fermion Ltd ( 33 pc of capacity ). This block is fully booked. Other two will be used by the company for business expansion till FY 27

Increase in inventory due build up in anticipation of execution of Fermion contract

Baba Finechem’s H1 sales are 21 cr, PAT is 14 cr !!!

Disc: holding, biased, not SEBI registered

Yash Pakka – (Previously Yash Paper) – Rising from ash (23-11-2023)

Eduardo Estrada joins Pakka USA as CEO

Manappuram Finance (23-11-2023)

Why is the opex cost high compared to muthoot finance ?

APL Apollo Tubes (23-11-2023)

You need to look at seasonality – this is a business where you need to compare YoY and not QoQ.