Thanks for notes.

Only one correction here – On initial notes of concall – company said that L1 is 3550 Cr. However, later MD, Mr. Gupta rectified it by saying that L1 of 3550 Cr. includes received order of 850 Cr. So actual L1 is 2700 Cr

Thanks for notes.

Only one correction here – On initial notes of concall – company said that L1 is 3550 Cr. However, later MD, Mr. Gupta rectified it by saying that L1 of 3550 Cr. includes received order of 850 Cr. So actual L1 is 2700 Cr

(post deleted by author)

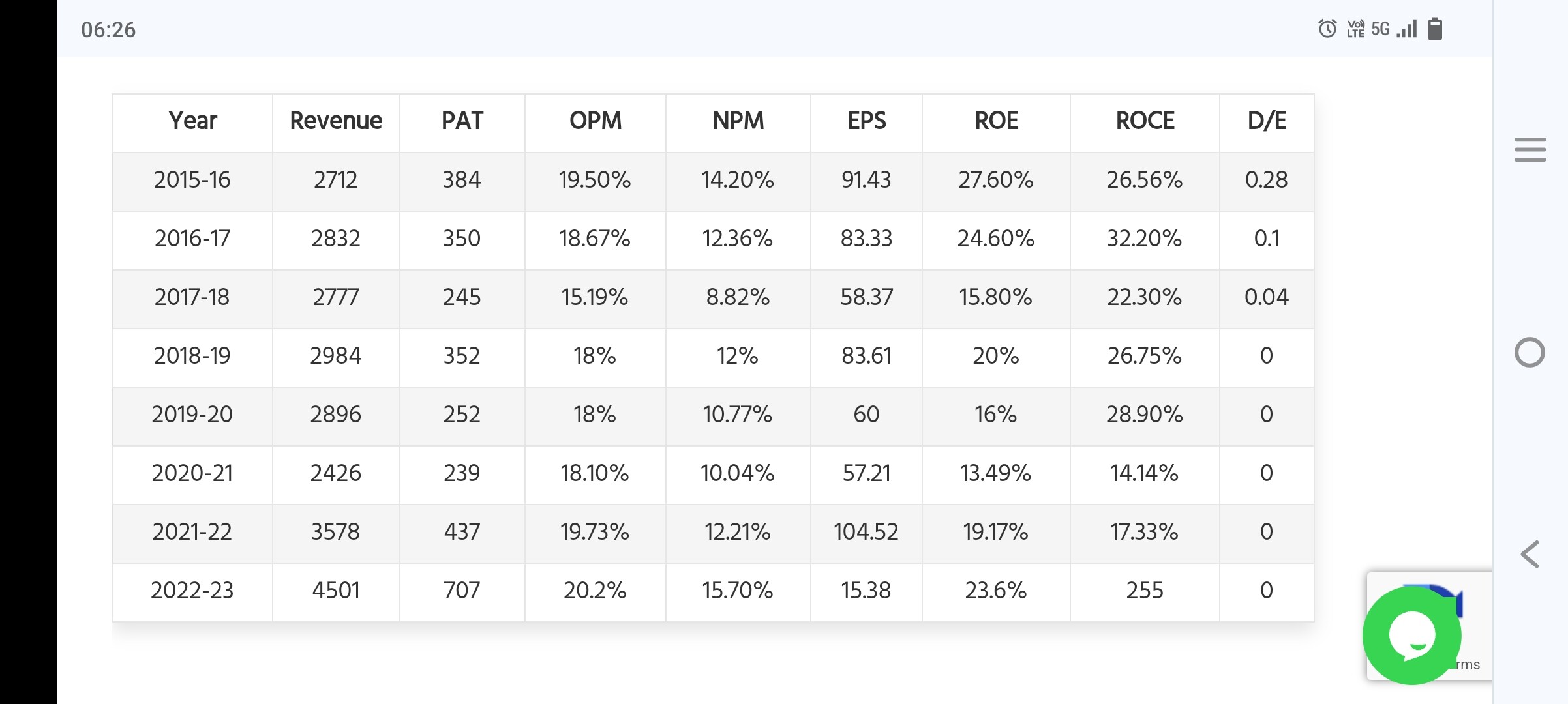

Flat topline for several years 2015-21, then suddenly shown big jump in last 2 years. Now it is coming with IPO right at the peak. An opportunity OR a Trap ?

No holding company will opt this way and however discount will get less due to one more possibility available for shareholders of holding company along with dividend pass on

I wouldn’t invest personally at these valuations. But great companies keep throwing positive surprises.

Also, I think relative valuations are in play. When many cable making and electrical goods making companies are trading at north of 50 PE and larger ones have mcap of close to 1 lakh crore, Titan doesn’t appear very expensive.

@KUMOD_KUMAR_GUPTA @Shubham_Dilawari

Many investors try to connect to their employees on call or LinkedIn to get to know real situation what’s happening in the Company

There might be some internal issues due to sales or growth or salary or handling responsibilities

Which creates a negative impact on directors and firm

But When a person leaves and another one is joining , vice versa Same work will be performed

( I m accepting experiences from old employees was not good but past is history and end of day , Company keeps growing and work keeps happening ) (logical side)

If I think about future

If Major Red Flag will be there , it will be seen in coming quarters( u look 8 quarter results before selling any stocks , warren buffet one quote said look for 5 year avg number or something )

, it will good for management to learn from red flag if some big mistakes happen and rise up again

Paint industry is growing double digit in percentage for next decade

Mr Sanjay Agarwal and Apoorv Agarwal will not destroy their hard work from so many years they have took to built these business

I think they are Only struggling to gain market share and sales from my view rest no issues in company

From previous survey , shopowner told me they are bunch of Finance Guys

New Person is also CA , this shows similarities and lack of Marketing boost from management as finance guys cannot do good Marketing,

I have worked in Nobroker Startup company , I know how speeches are given when u struggle to sales and that’s what I found in two /sec video in video in YouTube that Sanjay Agarwal Boosting employees to push this product like typical Sales company ( no negative reviews )

My views are totally Biased One can ignore

Sirca has shown good Results this quarter

It is good debt free company , buy and hold forever type , less risky small cap other than others and easy to understand business

My theory is mutual funds are not buying due to overall Indian market share has less captured by them

Pls happy to ignore if you find something offensive

Discl : invested ,

when this report came , i parted 20% of my holding and felt cheated ![]() the stock bounced in 2 days

the stock bounced in 2 days ![]()

Yes I agree on all the points, Valuation is what i was not comfortable with, I asked myself would i be buying KPIT at this price and the answer was NO so left it, i rode the wave and i am out , it was a difficult decision, the day after i sold it i was cursing myself now that i have to pay 10% LTCG tax, so basically i sold for 10% below the market price ![]()

Chart of Natco had been discussed on 52 weeks high technical thread at following link.