I completely agreed with u…each word is true

I feel the largest down cycle of MFI industry is begin. There will be blood bath in rural sector…

Disc. Not invested , but I had interest in unlisted MFI.

I completely agreed with u…each word is true

I feel the largest down cycle of MFI industry is begin. There will be blood bath in rural sector…

Disc. Not invested , but I had interest in unlisted MFI.

Centre intends to sell 5% stake in Cochin Shipyard through the OFS route, at a floor price of Rs 1,540 per share, an exchange filing said on October 15.

The Offer For Sale, which opens on October 16, will include a base offer of 2.5% stake or 66 lakh shares, as well as a green shoe option of another 2.5%.

The OFS will open on October 16 for non-retail investors and for retail investors, the issue will open on on October 17. The indicative price for the non-retail category will be released separately.

My previous attempts were somewhat unsuccessful in fpo for retail. When they declare the floor price for retail and is it necessary to place the order above that price? Request your inputs pls.

Hi! I have added you to the WhatsApp group. A sincere request to all the members who wants to be part of this WhatsApp group is to kindly dm me their number only if they are interested in offline meets. We will be conducting offline meets at every last Sunday of the month. Next meeting will be held on 27th October. We conducted our maiden meeting last month and it was a great knowledge sharing session with many ideas presented.

Request everyone to not share their contact number on this thread. They can dm their contact number to me or @SHAIL_APTE

84cr profit before tax, after 26% tax net profit should come down to 62.16cr

Any connection between the RILs launch of solar panels in Q4 2024 and trigger of its mega solar plant? At present they are going slow using the pilot plant as a excuse.? Can it be RIL solar panels with SW EPC?

If you are going as per Mgmt. forecast, then bake in ~10% of tax from their forecast as explained in the call. So FY27 bake in 450 cr. topline.

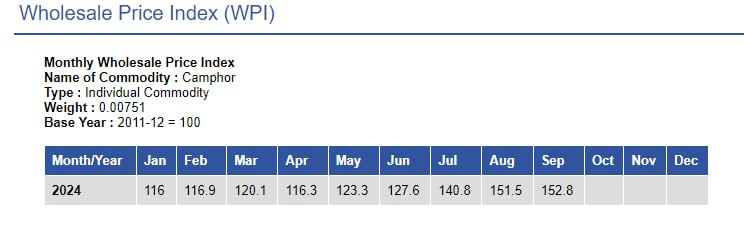

Q2 should be good … camphor prices have sustained through out the quarter…